Learning From Brad DeLong and Paul Krugman

[UPDATE below.]

Rather than have a long series of posts discussing the fallout from my (price) inflation bet with David R. Henderson, I decided to do one comprehensive reply to Brad DeLong and Paul Krugman. I had toyed with not even responding, but two things ruled that out: (1) This isn’t a case of two guys challenging me on some academic point; they are publicly impugning my character. (2) My supporters have pledged (as of this writing) more than $81,000 that will go to a food bank in NYC if Krugman ever debates me on business cycle theory.

If I just walk away from this incident, they might worry that Krugman is holding a trump card against me, and their enthusiasm for promoting the debate will wither. So to be clear, I would still love for Dr. Krugman to publicly debate me on Keynesian vs. Austrian business cycle theory, and if he ever did try to bring up this inflation bet, I have lots I can say in reply, as I discuss below. Because this post will be long, I am organizing it into sections.

I. The Pot Calling the Kettle a Pot

It is simply astounding to me that I am being accused of ideological dogmatism and a refusal to see the merits of my opponent’s position by these particular gentlemen. Brad DeLong is notorious for deleting people’s comments on his blog who say things that disagree with him. This is not an urban legend. It’s happened to me, to Mario Rizzo (you know, that bomb-thrower Mario Rizzo), and other people who are being completely courteous and on-topic. DeLong also has a running series where he nominates the “Stupidest Man Alive” (here’s an example), and he routinely mischaracterizes his opponents’ positions in arguments ranging from economics to politics to philosophy–for example, implying someone was a creationist (who in reality was an atheist) but not actually saying so explicitly, proving that DeLong knew exactly what he was doing. (If you really want a fun anecdote, here I explain DeLong’s outrageously selective reading from Herbert Hoover’s memoirs.)

Paul Krugman, for his part, tells us, “Some have asked if there aren’t conservative sites I read regularly. Well, no. I will read anything I’ve been informed about that’s either interesting or revealing; but I don’t know of any economics or politics sites on that side that regularly provide analysis or information I need to take seriously. I know we’re supposed to pretend that both sides always have a point; but the truth is that most of the time they don’t.” Beyond that, Krugman routinely dismisses his critics as idiots or liars who literally don’t understand intro macro, even if they are expressing a stance he himself held within the previous 15 years.

Let us not forget what the former New York Times Ombudsman Dan Okrent had to say about his professional dealings with Dr. Krugman. He said that after some serious haggling, he once got Krugman to “reluctantly” issue a correction on something in one of his columns, and then Okrent comments on that word, “I can’t come up with an adverb sufficient to encompass his general attitude toward substantive criticism.” (I can find people quoting Okrent, but the links to the original seem broken.) But don’t take Okrent’s word for it; just go read Krugman’s blog for a week, and then you tell me if he’s the kind of guy who freely admits when his critics had a good point on something.

So in summary, I am being hauled in front of a tribunal, being accused of dogmatism and an unwillingness to see when my opponents have the better of me…by Brad DeLong and Paul Krugman?! Can this really be happening? I’m hoping Rod Serling can make an appearance and shed some light on these events.

II. Austerian #1 vs. Austerian #2: No Matter Who Loses, Krugman Wins

I made a bet on official CPI and lost. Brad DeLong wants me to announce on my blog, “I have been totally wrong, about everything. I am closing down this weblog for five years to avoid misleading readers while I intellectually retool. You will find me sitting at the feet of Paul Krguman, chanting ‘om mani padme hum’ until I achieve enlightenment.”

But wait a second. I didn’t bet against Paul Krugman, I bet against David R. Henderson. So why wouldn’t I have to sit at David’s feet?

Well, the answer is that David is an “austerian” (in Krugman’s terminology) too. And I don’t just mean if you grabbed him on the street and asked him. I mean, he wrote a study for a DC think tank on how Canada solved its fiscal crisis mostly by actual cuts in federal spending, and he went on John Stossel’s show to preach this message of austerity. That’s the guy who won the bet.

Since David just won a bet, that’s a feather in the cap of his model, and now Brad DeLong has updated his Bayesian priors on David’s worldview, right?

So to summarize, two economists who both have written studies urging fiscal austerity based on the Canadian example (mine here) had a bet. When one of the austerians lost–which had to happen, since ties were impossible–DeLong and Krugman thought this proved austerity doesn’t work.

(In related news, I am trading public trash talking with Chris “Ron Paul’s Freaking Giant” Lawless on Facebook for a game of P-I-G in basketball at a conference in the summer. When one of us loses, will Rudy Giuliani say, “Aha! I was right about 9/11 after all!” ? If so, Chris and I will cancel.)

III. Price Inflation Has Virtually Nothing to Do With Austrian Economics in General, and Truly Has Nothing to Do With Austrian Business Cycle Theory

When explaining why Christina Romer’s notorious unemployment forecasts have no bearing on Keynesian models, but my price inflation forecast blows up Austrian economics, Krugman writes:

[I]t’s really important to distinguish between fundamental predictions of a model and predictions that an economist happens to make that don’t really come from the model….[T]he unfortunate Romer-Bernstein prediction of a fairly rapid bounceback from recession reflected judgements about future private spending that had nothing much to do with Keynesian fundamentals, and therefore sheds no light on whether those fundamentals are correct.

In short, some predictions matter more than others.

Beyond that is the question of how you react if your prediction goes badly wrong.

The fact is that while Keynesians predicting a fast recovery weren’t really relying on their models…

As Alex Padilla quipped on Facebook, if Romer wasn’t using her model to generate the unemployment forecast, then whose model was she using?

But joking aside, we all get the point Krugman is making here, and it’s a valid one. That’s why I’m going to say it applies to my price inflation bet, a lot more than it applies to someone who was saying we needed the Obama stimulus package because it was going to raise employment.

Simply put, my price inflation wager has nothing to do with Austrian business cycle theory. Mario Rizzo spells it out here, and to his credit Daniel Kuehn (who is a huge fan of Krugman and DeLong) also gives this claim a fair hearing on his blog. Yes, I screwed up in my bet with David–and possibly with Bryan, we’ll see–but it’s not because Mises and Hayek doomed me.

Really. For example, I just wrapped up on online course on ABCT and the Great Depression. The only point I recall making about price inflation that was directly tied to ABCT, was that Mises had explained before the Crash why Irving Fisher’s policy of stabilizing consumer prices could still allow an unsustainable boom.

Krugman thinks that worries over price inflation are essential to the Austrian position, because:

The prediction that huge increases in the monetary base will cause large increases in the price level, and that big government deficits will cause big increases in interest rates, are more or less inescapable if your model of the economy is one in which recessions are supply-side problems, not the result of inadequate demand.

Yes, that would be true, if other things were equal. But you could have a big reduction in supply (due to a discoordinated capital structure bequeathed by the preceding boom) accompanied with a big reduction in demand, because the financial world is collapsing and everyone rushes to dollars and Treasuries. This wouldn’t mean that throwing trillions of dollars in new money at the problem would solve the underlying real problem, nor would it mean that modest consumer price hikes would prove that some more $100 bills was the solution.

The fundamental problem here is that Krugman is using a very simple macro model, with a few aggregate variables, and he’s trying to spin out implications of the Austrian view in such a world. Well, that isn’t going to work because the Austrian theory relies on heterogeneous capital goods and the role that artificially low interest rates play in distorting the sectors into which investment flows. You can’t really test to see if that theory is right, by using a model that has AD and AS moving around and causing “the price level” to go up or down.

In any event, Krugman is hardly qualified to be telling us the empirical implications of Austrian theory. In his last written response to me, Krugman asked, “Why is there overwhelming evidence that when central banks decide to slow the economy, the economy does indeed slow?” To be clear, Krugman thought this would embarrass the Austrians, who must not have been aware of the peer-reviewed, cutting edge research showing that when central banks raise interest rates, the boom turns into a bust. This would be like asking a Christian, “Well if God loves us so much, why did He send His son?”

The problem here is that Krugman actually hasn’t read much of Austrian business cycle theory. I’m guessing–can’t prove it–that he read somebody else summarizing it. This is why Krugman apparently classified it as a “real” theory, relying on underlying technological considerations, as opposed to Krugman’s demand-based theory. Since the central bank raising interest rates doesn’t burn crops or kill workers, Krugman thinks the Austrians must not be able to explain how changes in money can affect the business cycle.

Anyway, if you want to see me give a point-by-point response to Krugman’s erroneous understanding of Austrian business cycle theory, read this essay.

IV. “Then Why Did You Bet Bob?!”

Because I thought I would win $500, duh.

Here’s the bigger context: Back in late 2008 and early 2009, many analysts–including me–were freaking out about the unprecedented actions that the Fed and other major central banks were taking. (For example, in June 2009 I explained why I thought the real economy would be “in the toilet for a decade” and that I expected “20+ percent price inflation.”) Bryan Caplan thought we were overreacting, and wanted to bet on something specific, so that the inflation-mongers couldn’t just issue vague warnings that might someday come true. Understanding that he had a point about non-falsifiable hysterics, I bet Bryan $100 in 2009 that by January 2016, official CPI would rise 10% year/year.

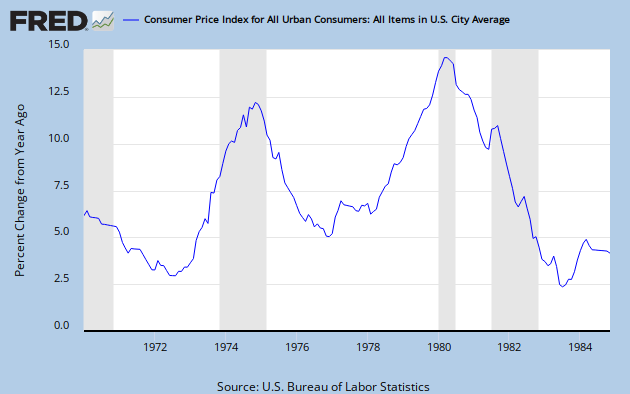

Just to be clear–since these two points come up in every comment section on the issue–I was aware at the time that there are serious problems with the way the government calculates CPI, and I knew that if I won the bet, I would be getting paid in weaker dollars than if Bryan won. (I understand that rising prices means a weaker dollar, yes, I do understand that.) Official CPI inflation rose at almost 15% yr/yr at one point in the early 1980s, and since I think what Bernanke has done will ultimately be worse, I am thinking the government won’t be able to get away with reporting less than a double-digit rise.

Seeing my bet with Bryan, David wanted a piece of the action, but he wasn’t comfortable giving such a big window. So he wanted to shorten the horizon from January 2016 down to January 2013, and bump up the amount from $100 to $500. Obviously I was less confident about this bet than the one with Bryan, but I still thought I would win it so I said sure.

V. What Went Wrong?

I’m not sure yet, which is why I haven’t performed seppuku as DeLong insists. I realized that there were a lot of excess reserves when I made the bet with David, but it was also true that M1 had risen strongly since the onset of the crisis (presumably as people fled to very liquid assets). The big thing is that I did not, and do not, trust Bernanke when he tells us there will be a gentle unwinding of the Fed’s balance sheet, and that if things ever started getting out of hand he has all sorts of “exit strategies.” I thought other investors would eventually agree with me that the Fed was simply printing money to buy time and temporarily stave off disaster, and they’d head for the exits. Back in late 2009, I was sure enough that this would happen within two years that I bet $500 on it.

Well, it hasn’t happened yet, so what does that mean? Are we stuck in a dollar and Treasury bubble that is taking longer to pop than I thought? Or have I been “completely, comprehensively, unmistakably, fundamentally, fatally, totally wrong,” as Gentle Brad puts it?

I don’t know, of course, and none of us can, until the bubble bursts or the Fed unwinds its balance sheet with no major hiccups. So I haven’t been writing much on price inflation in a while, and when people ask me in radio interviews etc., I have been prefacing my remarks with, “Let me just admit, I thought this was going to happen already and it hasn’t, so take my analysis with that caveat…”

VI. Learning From My Mistakes, DeLong and Krugman Style

It’s true, Krugman and DeLong have changed their minds on plenty of issues over the years. For example:

(A) Krugman’s notorious 2002 call for Greenspan to replace the bursting tech bubble with a housing bubble. Then, just to be sure there was no misunderstanding, read the 2006 exchange with a reader to see Krugman’s nuanced view of the matter. Having had to explain this extremely unfortunate statement many many times, Krugman has learned to no longer make flippant remarks about the Fed creating an asset bubble to prop up aggregate demand.

(B) In the late 1990s Krugman thought that there was only dubious theoretical justification, and perhaps not a single historical example, for the view that a large fiscal stimulus could rescue an economy from the liquidity trap. Krugman actually used the term “Krugman solution” to refer to a purely monetary approach. Early in the 2008/09 crisis, Krugman championed fiscal policy. Then later, he came back to monetary. In a similar vein, DeLong in early 2009 said monetary policy had “shot its bolt” and was championing fiscal policy. Eventually though he acted like he’d been bosom buddies with Scott Sumner all along.

(C) When it comes to understanding/forecasting the bond markets, Krugman and DeLong have both admitted mistakes. Read what is now a laugh-out-loud funny article from Krugman freaking out about the US government’s debt and the imminent attack from bond vigilantes back in 2003, and in this piece DeLong explains that he has “gotten significant components of the last four years wrong…federal funds rates at zero I expected, but 30-Year US Treasury bonds at a nominal rate of 2.7% I did not.” (HT2 EPJ)

And there are plenty more I could give you. So yes, it’s true: Reading DeLong and Krugman is like watching a ballet, with one dancer named Fiscal and the other Monetary, and at any moment you’re not sure who will be leading the other. But the title of the ballet is, “The Free Market Needs a Genius Like Me to Fix It.”

Krugman and DeLong have tweaked their views over the years, but they are still interventionists. There is literally no empirical outcome that would ever make either of these guys say, “Oh my gosh, I have been totally wrong about the need to prop up Aggregate Demand. I am going to send Peter Schiff an apology.”

So when Krugman says that his Keynesian colleagues have engaged in “soul searching,” this is the kind of thing he means. They’re not questioning the core premises at stake here. Look at how he handled my question about Christina Romer: He didn’t even entertain the possibility that it was the Obama stimulus package that made the economy suddenly “get worse than we realized” in early 2009. No, we all just know that a big deficit creates more jobs than would otherwise be the case, and so if Romer’s forecast was off, well it was because she plugged in the wrong baseline.

In the spirit then of being as flexible and data-driven as DeLong and Krugman, let me report on how much I’ve changed my own views in just the last few years:

(D) I used to think that unemployment benefits and refundable tax credits weren’t that big a deal in explaining the sluggish recovery, but the empirical work of Casey “Poverty Should Have Risen” Mulligan has made me change my mind.

(E) I used to think that if we were going to have a Fed that did something, it might as well lock in a fixed price of gold. But now I’ve been convinced by other Austrians that this would probably be a bad idea, because the Fed officials would just go off the new gold standard the next time it became really onerous, thus discrediting the reform. If we’re going to push for a massive change, might as well go for complete abolition of the Fed.

(F) I used to think–and even wrote it up in my textbook for young readers–that the only way a government debt could impose a burden on future generations, was through the crowding out of physical investment in private capital goods. But then Don Boudreaux and Nick Rowe showed me that government debt can allow the present generation to effectively transfer wealth from their descendants in a much more direct way. Thanks guys, you made the scales fall from my eyes.

(G) Relevant to my inflation bet, I’ve learned something important: The urgent task isn’t to abolish the Fed, but rather to abolish the IRS. Price inflation wasn’t the clear and present danger I thought it was back in 2009. My priorities have altered. First the IRS, then the Fed.

Now that I’ve exhibited the analogous flexibility in my policy views that DeLong and Krugman possess, I’m sure they’ll let me join their League of Distinguished Scientists, don’t you think?

Ha ha, of course not. They get to “change their minds” by tweaking how they want the government to redistribute income and create new money. But when I get something wrong, they want me to drop my drawers, bend over, and ask, “May I have another stimulus, sir?”

VII. Krugman Wins Price Inflation, But Loses a Bunch of Others

Finally, let me remind people of some issues directly related to diagnosing the cause of the recession–“sectoral imbalance” versus “general shortfall in demand”–where Krugman was simply wrong:

(A) In late 2008 Krugman argued that the housing bust had little to do with the recession, because the latest BLS figures showed that unemployment at the state level bore little relationship to the declines in home prices across the states.

However, I pointed out that looking at year-over-year changes in unemployment at the end of 2008 was hardly the right test. If we looked at changes from the moment the housing bubble burst, then five of the six states with the biggest housing declines were also in the list of the six states with the biggest increases in unemployment.

(B) Later, Krugman once again thought he had dealt the readjustment story a crushing blow when he pointed out that manufacturing had lost more jobs than construction. I pointed out that this too wasn’t a valid test, because manufacturing had more workers to begin with. When we looked at percentage declines, then construction did indeed crash more heavily than manufacturing. Furthermore — and just as Austrian theory predicts — the employment decline in durable-goods manufacturing was worse than in nondurable-goods manufacturing, while the decline in the retail sector was lighter than in the other three.

There are other examples–how about Krugman telling people gold went up (as the “inflationistas” would have predicted) not because of Bernanke, but because of Glenn Beck?–but the above two suffice to make my point. I didn’t pick out the above two tests of our theories; Krugman did, and (I argue) he botched the tests. When you run the tests in what is surely a more appropriate way, Krugman’s theory no longer comes out on top, and moreover, his theory can’t really explain the results the way the Austrian explanation easily can.

So feel free to send those links to Dr. Krugman, and let’s see how much soul-searching they provoke.

UPDATE 1/3/2013:

After reading an excellent post by Nick Rowe explaining why there are no controlled experiments in macroeconomics, I realized there was one crucial point I forgot to make in my original post, above. So let me append one more section, and then hopefully we can all move on with our lives.

VIII. If I Happen to Win the Bet With Caplan, Krugman Will Still Be “Vindicated”

Suppose that by January 2014 (well ahead of schedule for what I need), the dollar has fallen strongly against other currencies, short-term Treasury yields have risen to 7%, headline CPI has risen year/year by 11%, and the national unemployment rate has moved up to 9.3%. So Bryan cuts me a check for $100, my fans have multiple orgasms, and then what does Krugman write on his blog? Does he say, “You may have won this time Murphy, but I’ll be back, I’ll be back!!”

No, that’s not at all what he would write. Rather, it would go something like this:

Oh my. It seems the childish blogger at ZeroHedge–who likens himself to a paranoid schizophrenic movie character, which is actually quite appropriate–is chortling with glee because an austerian won a bet about inflation, and it so happens that it’s the same guy who earlier lost a bet (upon whom Brad DeLong and I heaped justifiable scorn). Even though the austerians and ZeroHedge folks have been totally, utterly wrong for five years straight–see here, here, and here–they now want to argue that I should quit blogging and just play golf, or something.

Um, no. As anyone who has actually, you know, read my blog would understand, I never said the US would forever have modest inflation. Indeed, literally the same week I took this austerian down for losing his first (and bigger!) bet, I explained that inflation would one day become a real threat.

I know the austerians don’t understand the liquidity trap, but the rest of us serious analysts do. I have always said that inflation would remain subdued so long as we were in the liquidity trap. Since the Fed has been steadily raising rates since August, we are clearly no longer in the liquidity trap, and now we return to the normal framework where the austerians won’t make utter fools of themselves.

But here’s the thing: It’s not merely that the IS/LM framework once again comes through with flying colors. In terms of policy prescriptions, the Fed and government have been doing exactly what the austerians have been screaming for, all along. The Fed has been raising interest rates–just like the Hayekian groupies want, to avoid those dastardly “artificially low interest rates”–and as part of the budget deal from late February, discretionary spending has been trimmed by a whopping $850 billion. And yet, unemployment went up. Imagine that–contractionary policy is contractionary. Who knew?

If you doubt that Krugman would write something like the above, then you need to become more empirical. And just to reiterate my main theme here in this final section, Krugman would be justified in so arguing. Economics is not about unconditional forecasts, rather, its core propositions or “laws” are couched in ceteris paribus terms. Economic theory gives us a framework for interpreting the world. So it’s not that Krugman the Keynesian is wrong for being able to explain his way out of any predicament, rather it’s that he is fooling himself for thinking he is a “scientist” as opposed to those medieval Austrians who talk about a priorism.

Last thing, somewhat related: I got burned because I went out on a limb and locked myself into a specific CPI range by a specific date. Obviously, that was a dumb thing to do, both in terms of my bank account and reputation. But Krugman is able to run victory laps partly because he himself has a humongous “error bar” in his stated views. For example, over the last few years Bob Wenzel has comedically pointed out every time Krugman warns of deflation. So: I warned of serious price inflation and was wrong, and mocked accordingly. Krugman for years has been saying price deflation was the threat, that hasn’t come to fruition, and he is hailed as Nostradamus.

Yes yes, of course Krugman and his fans can explain away why his warnings of deflation didn’t pan out. Bernanke saved the day, blah blah blah. But they should then not get so upset when I and my fans explain away my botched price inflation warnings. That’s really the issue here: Guys like Nick Rowe, Russ Roberts, and me understand full well just how hard it is to remove ideology from the estimates of “multipliers” and such, whereas Krugman, DeLong, et al. don’t realize how much they are infused with confirmation bias every time they pick up a keyboard.

{kind=link}

Bro, I love you so much right now.

Not to oversimplify it, but isn’t the debate about inflation/deflation more of a debate of which is the stronger force: Americans deleveraging vs the Fed’s QE?

The Baby Boomers alone could explain why inflation has not happened yet. 100 million have peaked in their consuming. They lost a bunch of wealth in 1999 with stocks, then their home prices took a plunge. Our wealthiest demographic took a big hit. So they are paying down the debts (those lines of equity from their homes) and saving for retirment. Boomers have been the main engine behind our economy and arguably for money’s velocity. The Fed may or may not get the inflation they want. But that’s how I see the issue, layman that I am.

This is great.

This is a great response. I think the last stretch, in particular, sealed it: if the tables were turned, those two examples you point out would easily provoke us into mocking economists like DeLong and Krugman for not giving up New Keynesianism. Also, it’s too bad that with Krugman, for the most part, it’s either you love him or you hate him, in the sense that there’s nobody in the middle that might say, “I think Krugman is right on most things, but his characterizations of Austrian theory aren’t credible” (i.e. they acknowledge that economists and writers like you [and me] have successfully rebuked his criticisms by showing that he set up a straw man) — then he’d be much less damaging, and much less influential in general. Finally, you’ve persuaded me to give Mulligan’s new book a chance.

My only criticism, and I think this hardly really qualified as criticism, is that a lot of people think DeLong’s personal attacks are an expression of sarcasm, and that his intentions are more benign than this post suggests. It’s true that he has a tendency to delete comments (he’s deleted mine, unless I respond to his WWII posts). Krugman, on the other, I think is purposely writing more seriously, and aggressively, than he otherwise would. He wants to transmit a feeling of confidence to his readers, and I think he’s becoming notoriously known for his bad temper when his image is on the line.

Tangentially, to win your bet with Caplan, I think what you need is a change in Fed policy, rather than the gradual release of bank reserves into circulation. First, there’s a lot of merit to the argument that since the marginal loan is decided by a bank’s capital current excess reserves, which really represent asset swaps with a neutral effect on capital, aren’t likely to be circulated (I don’t think it’s entirely correct, because liquidity matters, but it’s correct enough). Second, Bernanke’s main intention seems to have been to provide liquidity to the financial sector, and then sterilizing these injections by either selling treasuries (earlier during the crisis) or paying interest on reserves. It’s true that more recently Bernanke has hinted that the Fed will no longer strictly target inflation, but I think that this particular change isn’t big enough. In turn, major policy changes, I think, will depend almost entirely on changes in GDP growth — a more obvious recovery will probably help Bernanke keep more-or-less that status quo, but another contraction in output might push him to adopt something like nominal income targeting (and not 5-percent, but 5-percent plus whatever the current nominal income gap is, to get nominal income growth back on its long-run trend line).

A serious question, though: why CPI? Why not something like the price of intermediate goods? In other words, what makes you think that a radical growth in the money supply will mostly manifest in consumer purchases, rather than producers’ goods purchases? (By the way, intermediate goods prices were the hardest hit at the beginning of the recession — as Austrian theory predicts —, and have spiked, I think surpassing the previous peak.)

Thank you,

Jonathan

Very well written response. To paraphrase Tom Woods, regarding the points of Brad Delong’s and Paul Krugmans Krugman Kontradictions and Romneyesque flip-flops I predict we’ll hear crickets.

I doubt they’ll get the Cristian reference.

Regarding what went wrong with the inflation bet, I’ve heard a good case from Steve Hanke that the reason we haven’t seen massive inflation is due to the Basel III framework. While it is true the Fed has been monetizing the debt and pumping trillions of new dollars into the economy, Basel III has imposed capital requirements on banks that has essentially changed the reserve ratio from 1:10 to 1:6. This has reduced the ability of banks to lend, forcing a contraction in bank money that has made up for the new Fed money in the overall money supply.

Here is the EconTalk podcast I heard that lays out the case:

http://www.econtalk.org/archives/2012/10/hanke_on_hyperi.html

Hope it is useful to you.

As you have said elsewhere, the overall publicity is worth more than the $500 and anyhow, if David R. Henderson gets a massive upsurge in kudos then that ain’t exactly the end of the world.

Well I’m ready for a lot of people to bash me over this, but I think that the basic theory is that if government tips large quantities of additional fiat money into the system, it has to devalue the existing money, and thus have some upward effect on prices. What other conclusion could be compatible with the basic idea of supply and demand?

The problem with Austrian theory is that it doesn’t have a model to figure out where exactly those injected dollars are going to finally end up. Worse, the Austrian theory implies that you can’t have a model to figure out where those injected dollars finally end up because you never have as much information available as the rest of the world has available, so ultimately only a real world market can make the necessary decisions. Consumer Price Inflation measures a small subset of the total prices available in a marketplace, so maybe the injected fiat dollars will turn up in the CPI, or maybe they will turn up in house prices, stock prices, metal prices, oil prices, or somewhere else.

Also, the Austrian theory doesn’t have a model to say how quickly the new money flows through the system. It can sit as excess reserves in banks for an arbitrarily long time… and then what? I don’t think Keynesian theory has the answer either by the way, because Keynesian theory tries to claim that total quantity of money is more significant than the place at which the new money is injected… an affront to common sense. If we want a model of a modern economy we need to model the banks, and then there’s the problem that modern banks do not function independently of government, nor does modern government function independently of the banks.

Is there a rational theory of banking, that accounts for the corporatist cartel that banking and central banking has become?

I haven’t read about it in depth but there is Rothbard’s

The Case Against the Fed

where he explains how the Fed is a cartelizing devices for the banks.

Tel:

Well I’m ready for a lot of people to bash me over this, but I think that the basic theory is that if government tips large quantities of additional fiat money into the system, it has to devalue the existing money, and thus have some upward effect on prices. What other conclusion could be compatible with the basic idea of supply and demand?

Credit deflation.

These are good:

The Founding of the Federal Reserve | Murray N. Rothbard

http://www.youtube.com/watch?v=Ta7q1amDAN4

War and the Fed | Lew Rockwell

http://www.youtube.com/watch?v=Tl9lS5k7H5M

so maybe the injected fiat dollars will turn up in the CPI, or maybe they will turn up in house prices, stock prices, metal prices, oil prices, or somewhere else.

“My supporters have pledged (as of this writing) more than $81,000 that will go to a food bank in NYC if Krugman ever debates me on business cycle theory.”

Why does Krugman even need to debate you on the ABCT?

You may well deny it, but your own work – endorsing a monetary theory of interest rates, your PHD, and the paper “Multiple Interest Rates and Austrian Business Cycle Theory” – already severely undermine the classic Hayekian ABCT with the unique Wicksellian natural rate of interest:

“In his brief remarks, Hayek certainly did not fully reconcile his analysis of the trade cycle with the possibility of multiple own-rates of interest. Moreover, Hayek never did so later in his career. His Pure Theory of Capital (1975 [1941]) explicitly avoided monetary complications, and he never returned to the matter. Unfortunately, Hayek’s successors have made no progress on this issue, and in fact, have muddled the discussion. As I will show in the case of Ludwig Lachmann—the most prolific Austrian writer on the Sraffa-Hayek dispute over own-rates of interest—modern Austrians not only have failed to resolve the problem raised by Sraffa, but in fact no longer even recognize it.

Austrian expositions of their trade cycle theory never incorporated the points raised during the Sraffa-Hayek debate. Despite several editions, Mises’ magnum opus (1998 [1949]) continued to talk of “the” originary rate of interest, corresponding to the uniform premium placed on present versus future goods. The other definitive Austrian treatise, Murray Rothbard’s (2004 [1962]) Man, Economy, and State, also treats the possibility of different commodity rates of interest as a disequilibrium phenomenon that would be eliminated through entrepreneurship.”.

Robert P. Murphy, “Multiple Interest Rates and Austrian Business Cycle Theory”, pp. 11–12.

http://consultingbyrpm.com/uploads/Multiple%20Interest%20Rates%20and%20ABCT.pdf

That pretty much destroys the foundations of modern ABCT.

You are always good for a laugh. The existence of multiple interest rates would not seriously affect the ABCT at all. Those interest rates would still function as market signals, allowing for the directing of investment to meet consumer demand, and would still cause the same issues if distorted.

That said, I would also contend that the originary rate of interest is not generally, in the Austrian paradigm, treated “as a disequilibrium phenomenon that would be eliminated through entrepreneurship.” Instead, this rate is that of time preference, which is modified by risk premiums and a few other factors to create multiple interest rates in the actual market. On this, and on much of my interpretation of time preference in general, I differ from Bob.

But even if we assume multiple originary interest rates for various commodities, this in no way “destroys the foundations of modern ABCT”.

“The existence of multiple interest rates would not seriously affect the ABCT at all.”

Ah, the straw man argument … last refuge of the idiot.

What was asserted above is that the non-existence of the unique natural rate invalidates the classic Hayekian ABCT (which uses this concept) – and you have not demonstrated the falsity of that statement.

” Those interest rates would still function as market signals, ….”

You are saying that the banks/central bank reduce the interest rate below one of possibly hundreds of “natural rates”, are you?

“What was asserted above is that the non-existence of the unique natural rate invalidates the classic Hayekian ABCT (which uses this concept) – and you have not demonstrated the falsity of that statement. ”

Argument by assertion. Now THAT is the last refuge of the idiot.

Unless we are not examining the point Saffra actually made in the debate reference – the multiple own-rates for various commodities – then I have done exactly this.

“You are saying that the banks/central bank reduce the interest rate below one of possibly hundreds of “natural rates”, are you?”

If we accept Saffra’s criticisms as valid, and thus assume differing interest own-rates for commodities as being evidence against a single underlying rate, it still doesn’t affect things as you believe. A stratified rate of return exists for reasons that, while in my opinion having actually nothing to do with interest per se, do not affect the theory here. If there is, for instance, a 5% return on corn and a 10% return on wheat, a drop of 1% in the loan rates would distort these relative return rates when investment is done via financing through banks (even indirectly through financing of stock purchases with loans). A 2:1 return ratio – the one determined by the market – is now adjusted to a 1.83:1 ratio, leading to investment distortion in favor of corn.

“Argument by assertion”

Given that all arguments are conducted by using assertions/propositions, you’re effectively saying all arguments are invalid merely because assertions are asserted!

Impressive.

http://en.wikipedia.org/wiki/Proof_by_assertion

How hard do you work to come off as such a pedantic ignoramus?

Is this a trick question?

I feel funny siding with someone who likes to call himself Lord Keynes, but you don’t seem to understand what the problem with proof by assertion is all about.

“you don’t seem to understand what the problem with proof by assertion is all about”

How do I not? LK has repeatedly asserted that multiple interest rates invalidates the ABCT. He does not explain how this does, or where in the logic it matters whether there is one or many interest rates. Simply repeats the assertion, as if this proves it to be true.

To top this off, I actually wrote a post countering his assertion, and instead of responding with his logic, he goes off on a tangent about how I didn’t get the name of the fallacy I was accusing him of just right.

” LK has repeatedly asserted that multiple interest rates invalidates the ABCT.”

No, I have not, but that it invalidates the classic Hayekian version of the ABCT. Any version that dispenses completely with the single natural rate obviously is not invalidated in this way (though there are ample other reasons why even these theories are unsound).

Add the straw man argument to Tanous’s list of fallacies.

Also, Mises clearly used the unique Wicksellian natural rate in his original version of the ABCT, so that original theory is just as flawed:

“In his Theory of Money and Credit, Mises had based his analysis on the Wicksellian distinction between the natural rate of interest and the money rate. But this distinction was untenable in light of Mises’s work on economic calculation and on the non-neutrality of money. There is no such thing as a natural rate of interest, defined as the rate of interest that would prevail in a barter economy. And even if there were such a ‘natural’ rate of interest, it would still be irrelevant for the analysis of a monetary economy. Money is not just a veil over a barter economy. “

Hülsmann, J. G. 2007. Mises: The Last Knight of Liberalism, Ludwig von Mises Institute, Auburn, Ala. p. 779ff.

It would be a fallacy if LK had claimed that he was right because he said so. But he didn’t do that. Only to assert something is hardly a fallacy in itself.

“It would be a fallacy if LK had claimed that he was right because he said so.”

That would be a different fallacy – ipse dixit, aka the bare assertion fallacy, to be exact. LK has engaged in a proof by repeated assertion fallacy.

“No, I have not, but that it invalidates the classic Hayekian version of the ABCT. ”

Again, assertion without logical reasoning. Also, pedantic – focusing on a sole version, to the exclusion of all others, to avoid any sort of rational debate. Strange that you focus so much on Hayek when commenting on a blog that holds far closer to Mises.

As for Hulsmann, I cannot claim to be an expert with Mises’ Theory of Money and Credit, but my reading was that he had modified the Wicksellian “natural rate” to be the rate of equilibrium in a monetary economy. Again, no expert on it, but that was my reading – I’m sure Murphy is more aware of the particulars than I am.

But if all we need to disprove a theory or regard it as inconsequential and heavily flawed is a theoretical mistake that is not essential to the theory in the first place, how can you hold to any of the Keynesian nonsense? You shouldn’t be a New Keynesian or “post-Keynesian” or whatever, but something entirely different, because Keynes said a lot of stuff that was not right, and it was far more consequential in his theories than the number of interest rates is to ABCT.

As Hayek makes clear in his reply to Sraffa, no it doesn’t.

“As Hayek makes clear in his reply to Sraffa, no it doesn’t.

And he was wrong – and his modifications of the theory later in the 30s show in the end he understood this.

“And he was wrong – and his modifications of the theory later in the 30s show in the end he understood this.”

What modifications are you talking about?

Sraffa showed in his last comment to Hayek that his point against single natural interest rates is superficial:

Hayek’s response shows Sraffa’s criticism doesn’t REFUTE the ABCT:

“I think it would be truer to say that, in this situation, there would be no single rate which, applied to all commodities, would satisfy the conditions of equilibrium rates, but there might, at any moment, be as many “natural” rates of interest as there are commodities, all of which would be equilibrium rates; and which would all be the combined result of the factors affecting the present and future supply of the individual commodities, and of the factors usually regarded as determining the rate of interest.”

All the interest rates would be equilibrium rates. How in the world does this, as you claim, “destroy the foundations of modern ABCT.”?

Sraffa’s last comment was this:

“Dr. Hayek now acknowledges the multiplicity of the “natural” rates, but he has nothing more to say on this specific point than they “all would be equilibrium rates”. The only meaning (if it be a meaning) I can attach to this is that his maxim of policy now requires that the money rate should be equal to all these divergent natural rates.”

Exactly. The optimal CB policy is one where it can set all interest rates to be their natural equilibrium rates. Of course that is impossible, which is why we need ABCT to explain what happens when nominal rates diverge from their unhampered market (i.e. “natural”) rates!

You’ve exploded his ENTIRE post. Nice one, Lord.

Oh, wait…

From my brief reading of Murphy’s paper the existence of multiple interest rates complicates but in no way undermines ABCT.

At a simplistic level one only needs to substitute the concept of dynamic equilibrium for the concept of natural rate of of interest and and the theory still works, Murphy just didn’t have time in that paper to provide an example.

“From my brief reading of Murphy’s paper the existence of multiple interest rates complicates but in no way undermines ABCT.”

In no way??

And why, pray, does Murphy tell us explicitly that “Austrian expositions of their trade cycle theory never incorporated the points raised during the Sraffa-Hayek debate. Despite several editions, Mises’ magnum opus (1998 [1949]) continued to talk of “the” originary rate of interest, corresponding to the uniform premium placed on present versus future goods. ”

Also, notice Murphy’s embarrassed silence over this whole issue.

Perhaps Murphy’s too timid to assert on his actual blog – on front of his mindless fanboys – what he asserted quite clearly and unashamedly in his paper.

“on front of his mindless fanboys”

Does anybody else crack up when they see a guy with the moniker “Lord Keynes” make a comment like this?

My favorite is when he uses the word “cult” and its derivatives.

I haven’t noticed too much embarrassment from the Murphy camp in terms of defending unpopular positions – I assume he is just focused on other topics.

From an Austrian perspective I think this is just a rather subtle issue that would leave ABCT needing some fine-tuning but really would not change too much fundamentally.

From a big picture Austrian view then even with multiple own-rates of interest the market, left to its own devises, would “discover” the structure of interest rates that would lead to a stable structure of production (one that that accurately reflected societies time-preferences). . Any interventions into the market that caused a deviation from this interest rate structure would cause a corresponding deviation from this optimal structure of production.

The derivation of the equilibrating structure of interest rates becomes more complex as a result of the Straffa discussion – but I think it would still be reasonably easy to accommodate it within Austrian theory. Market forces could still be identified. that tend towards the “dynamic equilibrium” being established.

Probably because he wanted to trick you into not reading the following passage in the same paper:

“I argue that the original Misesian insights still hold valid, and that the economist armed with ABCT has much to contribute to contemporary debates.”

Multiple interest rates does not undermine the original ABCT. It just means it should be updated.

Easiest way to do that is to just add an “s” at the end of the term “natural interest rate” every time it is mentioned.

That was hard.

Hayek did not originate ABCT. He got it from Mises, his mentor.

The same way you have not abandoned the core of Keynesianism despite some of Keynes’ arguments being rebuted and abandoned by his own followers, so too does the core of ABCT stand in the face of multiple interest rates as opposed to one interest rate.

I am not saying that you are arguing the introduction of multiple interest rates invalidates the entire ABCT. Yes, Hayek used a single natural interest rate in his discussions. However Mises, the originator of the ABCT that Hayek adopted, treated “the” natural interest rate as the rate that is TENDED towards in an ERE. Mises knew full well that interest rates in the real world market will be different:

“The final state of the market rate of interest is the same for all loans of the same character. Differences in the rate of interest are caused either by differences in the soundness and trustworthiness of the debtor or by differences in the terms of the contract.

“Differences in interest rates which are not brought about by these differences in conditions tend to disappear. The applicants for credits approach the lenders who ask a lower rate of interest. The lenders are eager to cater to people who are ready to pay higher interest rates. Things on the money market are the same as on all other markets.” – Human Action, pgs 458-9.

“Under the conditions of a market economy the rate of originary interest is, provided the assumptions involved in the imaginary construction of the evenly rotating economy are present, equal to the ratio of a definite amount of money available today and the amount available at a later date which is considered as its equivalent.” – ibid, pg 532.

“Originary interest can therefore in the changing economy never appear in a pure unalloyed form. It is only in the imaginary construction of the evenly rotating economy that the mere passing of time matures originary interest; in the passage of time and with the progress of the process of production more and more value accrues, as it were, to the complementary factors of production; with the termination of the process of production the lapse of time has generated in the price of the product the full quota of originary interest. In the changing economy during the period of production there also arise synchronously other changes in valuations. Some goods are valued higher than previously, some lower. These alterations are the source from which entrepreneurial profits and losses stem.” – ibid, pg 534.

“Originary interest is the outgrowth of valuations unceasingly fluctuating and changing. It fluctuates and changes with them. The custom of computing interest pro anno is merely commercial usage and a convenient rule of reckoning. It does not affect the height of the interest rates as determined by the market. The activities of the entrepreneurs tend toward the establishment of a uniform rate of originary interest in the whole market economy. If there turns up in one sector of the market a margin between the prices of present goods and those of future goods which deviates from the margin prevailing in other sectors, a trend toward equalization is brought about by the striving of businessmen to enter those sectors in which this margin is higher and to avoid those in which it is lower. The final rate of originary interest is the same in all parts of the market of the evenly rotating economy.” – ibid, pg 536.

“In the changing economy, the rate of interest can never be neutral. In the changing economy, there is no uniform rate of originary interest; there only prevails a tendency toward the establishment of such uniformity. Before the final state of originary interest is attained, new changes in the data emerge which divert anew the movement of interest rates toward a new final state. Where everything is unceasingly in flux, no neutral rate of interest can be established.” – pg 542.

“There prevails upon the loan market a tendency toward the equalization of gross interest rates for loans for which the factors. Without the aid of

this knowledge, the vast historical and statistical material available would

be merely an accumulation of meaningless figures. In arranging time series of the prices of certain primary commodities, empiricism has at least an apparent justification in the fact that the price data dealt with refer to the same physical object. It is a spurious excuse indeed as prices are not related to the unchanging physical properties of things, but to the changing value which acting men attach to them. But in the study of interest rates, even this lame excuse cannot be advanced. Gross interest rates as they appear in reality have nothing else in common than those characteristics which catallactic theory sees in them. They are complex phenomena and can never be used for the construction of an empirical or a posteriori theory of interest. They can neither verify nor falsify what economics teaches about the problems involved. They constitute, if carefully analyzed with all the knowledge economics conveys, invaluable documentation for economic history; they are of no avail for economic theory.” – ibid, pg 546

Finally,

“The connexity between all sectors of the loan market and the gross rates

of interest determined on them is brought about by the inherent tendency of the net rates of interest included in these gross rates toward the final state of originary interest. With regard to this tendency, catallactic theory is free to deal with the market rate of interest as if it were a uniform phenomenon, and to abstract from the entrepreneurial component which is necessarily always included in the gross rates and from the price premium which is occasionally included. – ibid, pg 546.

————————–

So here we have Mises explaining ad nauseum that “the” natural interest rate he referred to is an imaginary construction only, a mental tool used to understand the non-uniform interest rates that empirically prevail in the market.

Now, given that Mises, the originator of the ABCT that Hayek adopted, held that there will always prevail multiple interest rates in the market, the next question is: How can a theory that pedagogically utilizes a single natural interest rate, explain the real world? The answer should be straightforward, but for those who have an agenda of wanting to refute a theory, as you do, rather than approaching the theory from an unbiased rational foundation, which is what is required to understand it, Austrians have found themselves having to hold the hands of such agenda driven demagogues, and walk them through what they should be doing themselves:

The answer is that the market economy IS a complex, emergent process that tends towards an equilibrium that sees economic growth, rising standards of living, declining unemployment, and various other economic phenomena. Such tendencies follow from the nature of human actors as goal seeking entities. Goal seeking entities will make mistakes, but they will relentlessly move towards a final state that will forever be out of reach due to the fact that goal seeking itself affects the world and people and this introduces new valuations and a new final state tendency. And so on.

What “monetary manipulation” does according to ABCT is that it affects the economic calculation of individual market actors in a division of labor, in a non-market originated manner. Investors and consumers can see only one price structure and forecast only one price structure. But that relative price structure is affected by a non-division of labor, non-market activity. Thus, investors calculate using information that is generated by not just what consumers are communicating, but what the state is communicating as well.

In a market, relative prices tend towards relative marginal utility individuals place on goods. The relatively more valuable a good is, the relatively more pricey it will tend to be. Of course this tendency is itself brought about by entrepreneurs and speculators anticipating future consumer relative demands.

In a market with non-market state activity however, relative prices tend away from the marginal relative utility individuals place on those goods. Crucially, since those marginal utilities do not disappear just because there is a state, there arises a conflict between the marginal utilities of individuals in society. Instead of marginal utilities individuals place on goods being communicated by way of relative prices tending towards those utilities, the relative prices deviate away from that tendency because those prices include non-market state activity.

Investors cannot discern from a single price how much of it is due to state activity, and how much is due to market activity. This is the source of the business cycle on the market side of the economy. It is due to the relative prices conveying information that does not reflect only the relative marginal utilities of individuals, which thwarts what investors would actually be able to do in a free market, which is allocate resources and labor in a generally physically sustainable way.

In a division of labor, the tendency towards market based equilibrium is carried out by market actors through calculation. This tendency towards market based equilibrium is thwarted with non-market activity. Whether this distortion arises from petty criminals who counterfeit money in their basements, or grand official overlords who have a monopoly privilege, the effects are the same.

As the real Lord Keynes (as opposed to his cult followers who name themselves after him) once wrote:

“Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become ‘profiteers,’ who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

“Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” – The Economic Consequences of the Peace, Chapter VI, pgs 235-236.

Couldn’t have said it better myself. This is one of the few passages of Keynes I agree with. Too bad he contradicted himself and went sociopathic just a few years later.

(1) “Hayek did not originate ABCT. He got it from Mises, his mentor. “

No kidding! Not that anyone disputed this above, though it’s a nice red herring.

(2) And you are correct: given that ERE is a purely imaginary realm, whatever interest rate prevails there has no relevance to the real world.

(3) “In a division of labor, the tendency towards market based equilibrium is carried out by market actors through calculation. This tendency towards market based equilibrium is thwarted with non-market activity.”

It would be thwarted by purely market based activity too, given that consumer tastes and preferences are always shifting. Producers cannot predict what consumers want with perfect accuracy. Producers have subjective expectations. Producers’ investment decisions will not necessarily equal saving decisions or necessarily be sufficient to provide employment to all those willing to work.

The notion of a “tendency towards market based equilibrium” in any real economy is a fantasy – a fantasy Austrians share with any neoclassical.

1) You are the one repeatedly referring to the classical HAYEKIAN view. It would be like referring to Samuelson every time I reference Keynesian theories, and even calling them Samuelsonian theories.

2) Right. And if I throw a ball, the fact that the conditions of the world are not ideal and uniform means that the mechanical equations for projectile motion have no relevance to the real world. After all, such calculations are only imaginary, and the object likely will never reach the plotted destination exactly.

3) Changing preferences and imperfections in the process do not mean there is no tendency to equilibrium. That is an incredible non sequitur.

“Producers’ investment decisions will not necessarily equal saving decisions or necessarily be sufficient to provide employment to all those willing to work.”

Unless markets clear, and they do, so we have no problem. If you are not willing to accept a lower price or wage, then you are not preventing markets from clearing – you are voluntarily staying out of the market.

“Producers cannot predict what consumers want with perfect accuracy. ”

And those that are wrong are pruned out by the market itself, as part of the tendency towards equilibrium.

1) “Hayek did not originate ABCT. He got it from Mises, his mentor. “

No kidding! Not that anyone disputed this above, though it’s a nice red herring.

Yet you keep referring to Hayek as if he is the go to person for ABCT. it would be like referencing Mises every time you talked about Mengerian economics, rather than referencing Menger.

(2) And you are correct: given that ERE is a purely imaginary realm, whatever interest rate prevails there has no relevance to the real world.

False. The real world, according to ABCT, is a place where there is a tendency towards equilibrium, because the tendency derives from human goal seeking, not “out there” behind some rock or tree or price or demand.

(3) “In a division of labor, the tendency towards market based equilibrium is carried out by market actors through calculation. This tendency towards market based equilibrium is thwarted with non-market activity.”

It would be thwarted by purely market based activity too, given that consumer tastes and preferences are always shifting. Producers cannot predict what consumers want with perfect accuracy.

False. Changes on the side of producers and consumers are reflected in the information that market prices convey. The changes on the side of market activity are not disrupting to market activity. They are the very changes that tend towards equilibrium that monetary policy thwarts!

Laissez faire market economics does not hold that non-disrupting markets contain no changes. Changes are a part of a healthy economy, but not all changes are healthy.

You can’t argue that because consumers and investors change their preferences, that the market is thwarted, when that IS the very market process!

Producers have subjective expectations. Producers’ investment decisions will not necessarily equal saving decisions or necessarily be sufficient to provide employment to all those willing to work.

That’s exactly why Mises argued there is a TENDENCY among investor decisions reflecting saving and consumer decisions. If an investor is wrong, he will incur losses. If an investor is right, he will make gains.

Since investors tend to want to avoid losses and acquire gains, losing activity will tend to be avoided and gaining activity will tend to be sought. If a loss is made, something else is tried. If losses are made again, then again something else is tried. And so on until something works.

The notion of a “tendency towards market based equilibrium” in any real economy is a fantasy – a fantasy Austrians share with any neoclassical.

It isn’t a fantasy. It derives from the irrefutable axiom of action.

Most importantly, you can’t claim there is no tendency towards equilibrium in one breath, and then in another breath claim that there exists a tendency towards disequilibrium. For that is just another equilibrium, namely, a sub-optimal or substandard or undesirable one.

Only Post Keynesian cultists seem to be willing to claim that tendency towards equilibrium doesn’t exist, but then argue in favor of a tendency towards an equilibrium.

What lunacy.

I agree Major Freedom, Rothbard updated the ABCT using the ERE, with time preference and individual value scales at its core, far better than Hayek ever could. He showed that there were various interest rates that create one uniform rate. This uniform rate is the marginal efficiency of capital that Keynes was blind to seeing. It is the price spread of the various factors of the production process.

http://archive.mises.org/11584/rothbard-and-hayek/

“Producers cannot predict what consumers want with perfect accuracy. Producers have subjective expectations. Producers’ investment decisions will not necessarily equal saving decisions or necessarily be sufficient to provide employment to all those willing to work.”

Ah, so you DO get why the Austrian model works! No one person can predict what markets want, and even if he did he couldn’t continue to do so in a timely manner forever, which is why the most efficient way to organize markets is for no particular decision maker (be he an entrepreneur or Ben Bernanke) to control entire markets. Wasted time and resources are most effectively minimized when resource allocation decisions are distributed, so that those who predict poorly don’t drag down the whole economy with them, while those who predict well can maintain efficiency. This is how equilibrium is maintained, by the give and take between those who predict well and poorly. And if some lenders find varying success by lending at different rates for different businesses, this merely extends the relevance of the equilibrating process to the banking sector as well, meaning that it is imperative that banking be decentralized as well.

I’m glad we finally won you over to the Austrian perspective.

HOLY SH-!

MARXISTS, ARE YOU SEEING THIS?!

They are pitting us against each other, ON PURPOSE!

Thank you, Major Freedom!

#winning

While I agree with how some people want to engage in divide and conquer, I don’t think that is the purpose of why the founders of central banking founded central banking, nor why the current crop of monopolists are maintaining it.

But I could be wrong, because I can’t accurately infer their real intentions, other than what is tied up with their actions (printing money, buying specific assets from specific people at specific time, etc)

Again LK returns to his desperate attempt to hide the fact that he does not understand the concept of economic calculation with the red herring of the so-called single natural rate of interest. Hayek used the term “equilibrium structure” to refer to the price structure that would have existed but for GOVERNMENT intervention, especially granting banks the right to create fiat funny money loans out of thin air, thereby distorting the price, investment and capital structure. Hayek stated:

These discrepancies of demand and supply in different industries, discrepancies between the distribution of demand and the allocation of the factors of production, are in the last analysis due to some distortion in the price system that has directed resources to false uses. It can be corrected only by making sure, first, that prices achieve what, somewhat misleadingly, we call an equilibrium structure, and second, that labor is reallocated according to these new prices. ****

The primary cause of the appearance of extensive unemployment, however, is a deviation of the actual structure of prices and wages from its equilibrium structure. Remember, please: that is the crucial concept. The point I want to make is that this equilibrium structure of prices is something which we cannot know beforehand because the only way to discover it is to give the market free play; by definition, therefore, the divergence of actual prices from the equilibrium structure is something that can never be statistically measured. ****

In contrast, the modern fashion demands that a theoretical assertion which cannot be statistically tested must not be taken seriously and has to be discarded. As a result of this belief, a theory which, in my opinion, is the true explanation has been discarded as not adequately confirmed, and a false theory has been generally accepted merely because it happens to be the only one for which statistical evidence, even though very inadequate evidence, is available.”

http://www.flickr.com/photos/bob_roddis/7534880182/in/set-72157630494776170

Therefore, how could Hayek or anyone else know in advance what unadulterated interest rates might exist or how many different unadulterated interest rates there might be in the absence of intervention because “this equilibrium structure of prices is something which we cannot know beforehand because the only way to discover it is to give the market free play”.?

Personally, I prefer calling these prices and interest rates “unadulterated” or “adulterated” as opposed to “natural” and “artificial” if only to prevent monstrous liars like LK from employing the ambiguities in the terms for further deception and misrepresentation.

“Hayek used the term “equilibrium structure” to refer to the price structure that would have existed but for GOVERNMENT intervention, “

And neoclassicals don’t think of an “equilibrium structure” in the absence of government or unions?

Really? So where is this vast army of non-Austrians constantly bemoaning the adulterated and distortionary price signals induced by Keynesian funny money dilution?

Hint: one major school is called the New Classicals.

Who cares?

That’s wrong. The New Classicals reject Keynesianism, but they do not hold that inflation distorts the price structure that leads to painful corrections.

New Classicals are by and large monetarists themselves, and monetarism IS the very “funny money dilution” being referred to here. Saying New Classicals are bemoaning inflationism is like Keynesians bemoaning government spending.

There’s nothing wrong with unions, corporations, oligopolies, or 100% market share, per se.

It’s only when violence is used to achieve such things that there’s a problem:

Anti-Trust and Monopoly (with Ron Paul)

http://www.youtube.com/watch?v=8C4gRRk2i-M

Dominick Armentano: The Case for Repealing Antitrust Laws

http://www.youtube.com/watch?v=xBT-fnJsfo0

Why does Krugman even need to debate you on the ABCT?

Because you don’t want him to.

My personal view is that if you look at [A] the deficit, and [B] the total debt, and [C] the social security situation, and [D] the overall employment situation, the US government does not look to be in a stronger position today than it did in 2009. The backstop of value for the US government can only be the US population.

We have an Australian government that swore black and blue that it would turn a surplus this year, but that hasn’t happened. Now they decided to blame it on the Tea Party in the US (for reasons that make no sense) but really we are in a worse situation than we think as well. Australia is at least in a better situation than we were in 2009, but overall we stacked on a lot of public debt at the same time (we could afford it, but not forever).

“Well, that isn’t going to work because the Austrian theory relies on heterogeneous capital goods and the role that artificially low interest rates play in distorting the sectors into which investment flows”

Artificial compared to what? You already admit that interest rates are not explained by pure time preference theory. Nor do you believe in the Wicksellian natural rate.

So what is this rate above or below which everything is artificial?

“The big thing is that I did not, and do not, trust Bernanke when he tells us there will be a gentle unwinding of the Fed’s balance sheet, and that if things ever started getting out of hand he has all sorts of “exit strategies.”

And why not? The Japanese did QE from 2001–2006 and rapidly and successfully removed the excess reserves from the system.

Artificial relative to the rates that would prevail on the unhampered market.

There is nothing special about the rate on the unhampered market. Indeed, given that, in any really *free* market, FR banking and credit instruments would be ubiquitous, and by the logic of the ABCT theory, that market would be hit by perpetual Austrian business cycles anyway.

There is everything “special” about the rate on the unhampered market. It is the result of peaceful, voluntary agreements as opposed to violence, the threat of violence and/or fraud. Unadulterated prices reflect the vast dispersed fountain of knowledge inside everyone’s head that is not and cannot be conveyed in any other manner and which is impaired by statist interventions.

” Unadulterated prices reflect the vast dispersed fountain of knowledge inside everyone’s head”

No, they do not.

You’re effectively saying that – even if you had no government – when a business sets its prices it could magically create an equilibrium price by means of knowing and having perfect information about what price could clear a market in terms of many other agents’ preferences and decisions – even assuming (which is unlikely anyway) that such “equilibrium prices” exist across all markets.

Of we’re not saying that. If a business “sets” its price and someone pays it, then each party apparently thought they were better off doing the deal. Among other information created and transmitted, others can guesstimate that they too might find willing buyers for such goods/services at such prices.

It’s just not that complicated.

TYPO: The first sentence should have read:

“OF COURSE we’re not saying that.”

Non-distorting prices that do not bring about the business cycle do not need to reflect “perfect” information. Only market-based information is necessary.

And by market based, it means only market based information, if it gets into prices that is, influences prices.

What we mean by “equilibrium price” is that the price “equates” to the desires of each individual, as expressed in their desire to engage in peaceful exchange.

So, a business has set the “equilibrium price” when he is able to exchange with others for his own desired ends without the intervention of violence (or threats of violence) or of privileges and protections that derive from state violence (redistribution of wealth, monopoly privilege, etc.).

The point is that there is no equilibrium price, that is why there is fluctuations in price levels. Stop focusing on equilibrium analysis and realize that reality paints a different picture. Too much statist dogma fed to you by your over priced education buddy.

by the logic of the ABCT theory, that market would be hit by perpetual Austrian business cycles anyway.

No, it wouldn’t. You are conflating the arguments of 100% reservists and free bankers.

http://www.freebanking.org/2011/06/27/the-problem-is-central-banking-not-fractional-reserve-banking/

There is nothing special about the rate on the unhampered market.

False. The rates that prevail on the market are most reflective of individual relative marginal utilities of goods over time. They are “special” because to economists, interest rates MEAN SOMETHING. They are not merely book-keeping entries, or middle age “usury” ethical dilemmas, or cumbersome barriers to healthy markets. Interest rates in a free market regulate the temporal allocation of capital, which tends to reflect the inter-temporal preferences of individuals.

Indeed, given that, in any really *free* market, FR banking and credit instruments would be ubiquitous, and by the logic of the ABCT theory, that market would be hit by perpetual Austrian business cycles anyway.

Red herring.

Basic Economics Lesson 4 – Time Preference, Interest Rates, and Production

http://www.youtube.com/watch?v=g2OK5D_3TzM

Inflation also does that.

In particular inflation is a mechanism to interfere with the normal individual economic calculation of inter-temporal preferences. Each individual is then forced to predict how inflation will upset his/her future preference, and how to adjust for that.

Someone who would have been happy to save cash at 5% interest, will not be happy to save cash at 5% interest in the expectation of 4% inflation, so they are more likely to either buy an asset, or just spend the cash and not save.

FR banking and credit instruments would be ubiquitous, and by the logic of the ABCT theory, that market would be hit by perpetual Austrian business cycles anyway.

We go around and around on this.

http://factsandotherstubbornthings.blogspot.com/2012/07/bob-roddis-makes-bad-argument.html?showComment=1342710030818#c2618524232434861358

I submit that in a free market that bank notes would/should be required (to avoid a claim of fraud) to state on their face whether or not they are a warehouse receipt and if not, state on their face the amount of specie reserves backing the notes. I think notes with low reserves would either be rejected by the market or greatly discounted ( but I don’t know that for sure). Further, each firm’s form of money would carry their brand name so there would be little chance for prices across the board to become adulterated and become misleading. Each sale could/would be stated in the brand of the money employed in the transaction.

I think it’s quite odd that the interventionist statists go slightly berserk when I insist upon full disclosure written upon the face of FRB banknotes which the statists think is absurd and unnecessary (see link below). Well, if average people are so smart, there wouldn’t be any “macro” moments that average people can’t understand and only the anointed Keynesians can discern, right?. Further, if average people are not misled by prices that result from FRB notes, there is no possibility of malinvestment resulting from those prices, right? If no one is misled, there is no problem. If people are in fact misled, then they need more information. I don’t think this is all that complicated.

http://factsandotherstubbornthings.blogspot.com/2012/07/bob-roddis-makes-bad-argument.html

It probably helps to say that ABCT involves the “Cluster of Errors”.

If individuals suffer from their own miscalculations in a free market, they feel the pain sooner than when their mistakes are propped up by socialized costs.

So, the corrections to their miscalculations happen long before a cluster of errors can occur. At least in the “system-wide” sense, which is part of what we all mean by “crash”.

Hi Mr. Lord Keynes.

On the quotations that Mr. Major_Freedom has put upstairs is demonstrated what Agnes Festre has said:

[For Mises] “1. there cannot be any conceivable uniform rate of originary interest in a changing economy; 2. there is no more permanence in the rate of originary interest than in prices and wage rates.”

http://ideas.repec.org/p/hal/journl/halshs-00272399.html

Mises in Human Action was not using a wicksellian-one-unique-barter equilibrium rate. For him neither the originary nor the gross market rate was uniform outside equilibrium.

“It has been pointed out already that in the imaginary construction of the

evenly rotating economy the rate of originary interest is uniform… In the changing economy, there is no uniform rate of originary interest; there only prevails a tendency toward the establishment of such uniformity… The gross rates of interest as determined on the loan market are not uniform… In the rate of originary interest there is no more permanence than in prices and wage rates.”