Potpourri

* My brother sends me this YouTube of Hitler reacting to the Buffalo Bills’ signing of Terrell Owens. (We grew up in Rochester and so are Bills fans–they lost the Superbowl every year I was in high school. I am still bitter.) This is now the 3rd or 4th spoof of this scene; can someone tell me the actual movie?! It looks awesome.

* A reader (sorry I forget which thread this was in so I can’t look up who it was!) recommended this rather ominous story about the Bank of England promising to inflate until the economy is fixed. *Gulp*

* LRC hosts this AWESOME Jim Rogers interview. It’s 26 minutes, so what I did was start it and then do other stuff. But note how the young interviewer keeps bringing up the same fallacies over and over, and the wisened old Rogers–like Yoda correcting Luke’s aggression–keeps bringing him back to reality. It’s especially funny around 12:00 when Rogers reminds the guy that the British government couldn’t borrow money in the 1970s, and the guy says, “But that can’t happen again.” Rogers says (paraphrasing), “Well why don’t you write that one down and we’ll see.”

* Tyler Cowen links to a Greg Ransom post. The guy below is Hayek, the animal is named “Inflation,” and you’ll have to click here to see the full story (including double entendre).

The Housing Bubble Has Nothing to Do With the Recession?

In a recent debate (which I discuss here), Brad DeLong referred to an apparently decisive argument from Paul Krugman regarding the “hangover theory.” Here’s Krugman:

[T]he hangover theory, which I wrote about a decade ago, is still out there.

The basic idea is that a recession, even a depression, is somehow a necessary thing, part of the process of “adapting the structure of production.” We have to get those people who were pounding nails in Nevada into other places and occupation, which is why unemployment has to be high in the housing bubble states for a while.

The trouble with this theory, as I pointed out way back when, is twofold:

1. It doesn’t explain why there isn’t mass unemployment when bubbles are growing as well as shrinking — why didn’t we need high unemployment elsewhere to get those people into the nail-pounding-in-Nevada business?

2. It doesn’t explain why recessions reduce unemployment across the board, not just in industries that were bloated by a bubble.

One striking fact, which I’ve already written about, is that the current slump is affecting some non-housing-bubble states as or more severely as the epicenters of the bubble. Here’s a convenient table from the BLS, ranking states by the rise in unemployment over the past year. Unemployment is up everywhere. And while the centers of the bubble, Florida and California, are high in the rankings, so are Georgia, Alabama, and the Carolinas.

I’m going to deal with objection (1) in a forthcoming Mises Daily article. But for here, I want to discuss objection (2).

First, note that the BLS table looks at the yr/yr change in unemployment (by state) from Dec 07 to Dec 08. Now is that really a good measure of whether the bursting of the housing bubble has anything to do with the recession? After all, the bubble had well burst by Dec 07. So if the Austrians–or in fact, any economist who thinks the current recession “started” in housing–are right, you would expect the connection between unemployment jumps, and housing price collapses, to be weaker, the farther along you get from the bursting of the bubble.

Nudged on by an email from the mysterious von Pepe, I decided to check on the relation during a time frame that more tightly captures the bursting of the housing bubble. The OFHEO data is quarterly, and I picked the top of the bubble as 2q 2006. We can quibble with that, but that’s what I picked.

Then I picked the other variable to be the change in unemployment (in terms of absolute point changes, not percentages of percentages) from Jun 2006 to Dec 2008.

Then I ranked the states according to these two criteria, and looked at the worst 10 in both rankings. The 7th through 10th slots don’t match up, but check out the top/worst 6 slots in both lists:

Ranking of States By Point Increase in Unemployment Rate, Jun 06 – Dec 08

1……Rhode Island (+4.9)

2……Florida (+4.8)

2……Nevada (+4.8)

4……California (+4.4)

5……North Carolina (+3.9)

6……Michigan (+3.8)

Ranking of States By Percentage Drop in OFHEO Housing Price Index, 2q06 – 4q08

1……California, -27%

2……Nevada, -26%

3……Florida, -22%

4……Arizona, -16%

5……Rhode Island, -11%

6……Michigan, -11%

Note that North Carolina and Arizona are the only ones that don’t match.

I confess I haven’t yet run Monte Carlo simulations to see how likely this result is, out of 50 states, if there were no causal relation. But I’m feeling pretty good about my hangover theory.

On Miracles

Wintery Knight has an interesting post on how to argue with non-believers regarding the resurrection of Jesus. However, more than the post itself, what interested me was the issue he and a commenter touch on underneath it, regarding “front loading”:

Actually, in Christianity, there is a faction of scholars who prefer to “front-load” all of the biological design and miracles. I think this is done in order to keep God outside of time, subsequent to the big bang.

I have tons to say on this, but let me right now give a very succinct argument that I find irresistible. Maybe Wintery Knight or someone else can show me it’s not so open-and-shut. But here goes:

(1) The “laws of physics” are regularities that humans think they have discovered; they are apparent patterns that exist in the observations of physical phenomena.

(2) If one really understands the character of physical law–as explained by the master, Richard Feynman–then nature can never violate the laws of physics. If scientists repeatedly observe a violation of, say, the conservation of energy, then the “law” wasn’t really a law.

(3) Therefore it is impossible for God to “intervene” in nature and “perform a miracle,” if “miracle” means “matter behaving not in accordance with the true laws of physics.”

Like I said, I have a heck of a lot more to say on this issue. I am not disputing that Jesus did “miraculous” things, like walk on water. But my point is, by definition He did not thereby violate the laws of nature or physics. Such talk is nonsensical.

Potpourri

Three great pieces for ya…

* The definitive free marketeer blog post on how to think about the mark-to-market controversy.

* Bob Higgs rolls up his sleeves and blows up (what he calls) vulgar Keynesianism. I warn you that there are a few equations in here, but this is top-flight stuff. Higgs really nails the conceptual problems in the standard policy prescriptions coming from today’s gurus.

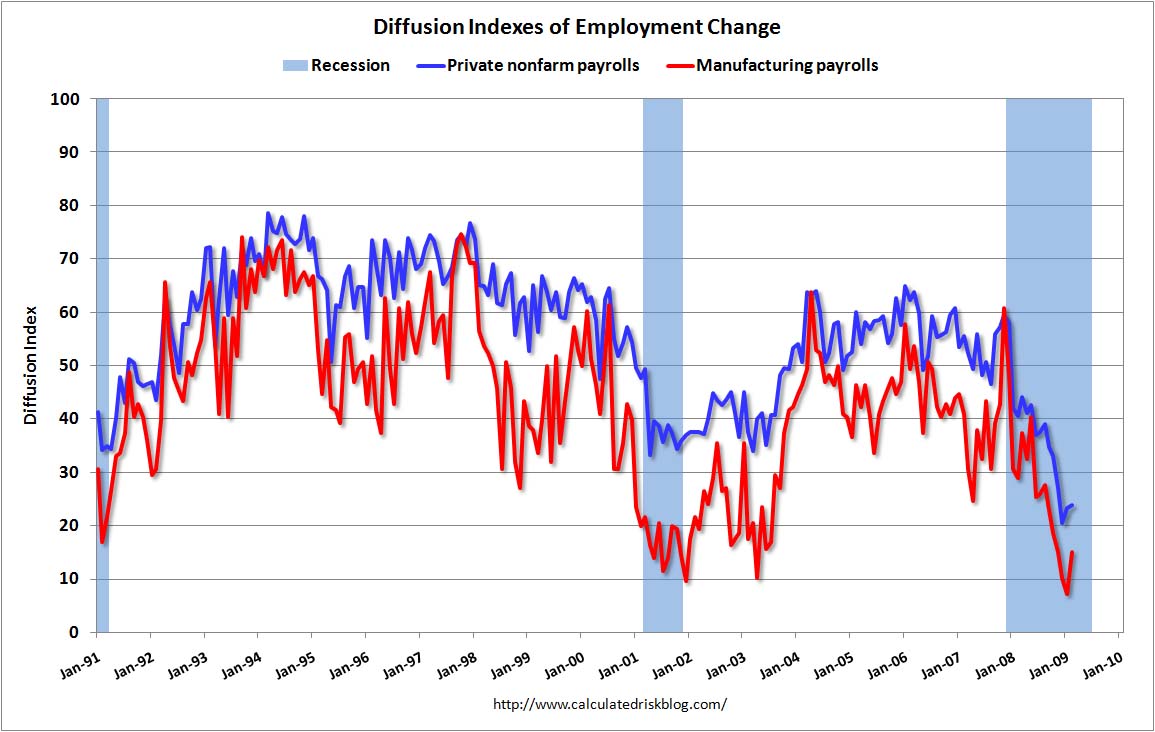

* Mario Rizzo adds yet another post on the problems with Keynesian “stimulus.” He links to this graph:

Now I’m not 100% sure, but I think what this image shows us is that the job losses during this recession are fairly concentrated in a few specific industries, particularly those in the manufacturing sector. (Note that I think the chart is not saying, “The job losses are mostly concentrated in manufacturing.” Rather, I think the chart is saying that within manufacturing, job losses are focused in very specific areas. But I could be wrong about that interpretation.)

UPDATE: Mario Rizzo sent me this clarification from the original site; they are saying the graph above means the opposite of what I claimed. My smart-butt response was, “So they should rename this the anti-diffusion index?” I will have to go the BLS and figure out exactly what this thing measures.

Australian PM Blames Geithner for Directly Messing Up Indonesia, and Indirectly for Contributing to Housing Boom

Tokyo Tom passed along this very interesting piece describing the accusations. (EPJ has two follow ups here and here.)

I’ll boil down the essentials here:

In a speech…[former Australian PM] Paul Keating gave a starkly different account of Geithner’s record in handling the Asian crisis: “Tim Geithner was the Treasury line officer who wrote the IMF [International Monetary Fund] program for Indonesia in 1997-98, which was to apply current account solutions to a capital account crisis.”

In other words, Geithner fundamentally misdiagnosed the problem. And his misdiagnosis led to a dreadfully wrong prescription.

Geithner thought Asia’s problem was the same as the ones that had shattered Latin America in the 1980s and Mexico in 1994, a classic current account crisis. In this kind of crisis, the central cause is that the government has run impossibly big debts.

The solution? The IMF, the Washington-based emergency lender of last resort, will make loans to keep the country solvent, but on condition the government hacks back its spending. The cure addresses the ailment.

But the Asian crisis was completely different. The Asian governments that went to the IMF for emergency loans – Thailand, South Korea and Indonesia – all had sound public finances.

The problem was not government debt. It was great tsunamis of hot money in the private capital markets. When the wave rushed out, it left a credit drought behind.

But Geithner, through his influence on the IMF, imposed the same cure the IMF had imposed on Latin America and Mexico. It was the wrong cure. Indeed, it only aggravated the problem.

Keating continued: “Soeharto’s government delivered 21 years of 7 per cent compound growth. It takes a gigantic fool to mess that up. But the IMF messed it up. The end result was the biggest fall in GDP in the 20th century. That dubious distinction went to Indonesia. And, of course, Soeharto lost power.”

Exactly who was the “gigantic fool”? It was, obviously, the man who wrote the program, Geithner, although Keating is prepared to put the then managing director of the IMF, the Frenchman Michel Camdessus, in the same category.

Worse, Keating argued, Geithner’s misjudgment had done terminal damage to the credibility of the IMF, with seismic geoeconomic consequences: “The IMF is the gun that can’t shoot straight. They’ve been making a mess of things for the last 20-odd years, and the greatest mess they made was in east Asia in 1997-98, so much so that no east Asian state will put its head in the IMF noose.”

China, in particular, drew hard conclusions from the IMF’s mishandling of the Asian crisis. It decided that it would never allow itself to be dependent on the IMF, or the US, or the West generally, for its international solvency. Instead, it would build the biggest war chest the world had ever seen.

Keating continued: “This has all been noted inside the State Council of China and by the Politburo. And it’s one of the reasons, perhaps the principal reason, why convertibility of the renminbi remains off the agenda for China, and it’s why through a series of exchange-rate interventions each day that they’ve built these massive reserves….

Is this some flight of Keatingesque fancy? The former deputy governor of the Reserve Bank of Australia, Stephen Grenville, doesn’t think so: “After the Asian crisis, the countries of east Asia decided that they would never go to the IMF again. The IMF is taboo in east Asia. Look at the evidence. The revealed preference of the region is that no one has gone to the IMF since, even when they needed the money.”

…

Keating went on to argue that, by frightening the Chinese into building their vast $US2 trillion foreign reserves, Geithner was responsible for the build-up of tremendous imbalance in the world financial system. This imbalance, in turn, according to Keating, contributed to the global financial crisis which has since devastated the world economy….“That is the fundamental cause of the problem – the imbalance is the fundamental cause.”

Now I’m not necessarily endorsing Keating’s analysis. For one thing, it sounds like he’s saying that everything was chugging along nicely, until Indonesia cut its government spending. Obviously I don’t endorse that.

However, it wouldn’t surprise me in the least if the IMF “austerity” measures messed up the region. When compassionate leftists complain that the cold-hearted IMF foists “market reforms” on beleaguered countries, my eyebrow shoots up. For one thing, I went to school with people who were going to work for the IMF, and believe me, they did not have dog-eared copies of Free to Choose lying around.

As I explained in the PIG to Capitalism (link is on the left margin if you’re curious), the IMF and World Bank austerity measures would–yes–involve things like lowering tariffs, but that sometimes include tax hikes to close budget deficits. Remember that the financial press described the Bush years as extreme deregulation, the next time you read that the IMF foists capitalism on socialist dictators.

Anyway, even though I came out strongly against the “global savings glut” explanation for the housing boom, in some conversations with Bill Barnett and Tom Woods, I came around to the position that the Bank of China’s actions could have exacerbated Greenspan’s ridiculous interest rates in the early to mid-2000s.

Think of it like this: Greenspan flooded the market with a bunch of new credit after the dot-com crash and 9/11 attacks. Now if the US were just a regular old country, the result would have been a decline in the foreign exchange value of the dollar, and hence a rise in the price of imports into the US. In other words, Greenspan’s money pumping would have led to domestic price inflation, and he would have had to back off.

But because the Chinese central bank had pegged the yuan (or renminbi) to the dollar, this in effect meant the Chinese were committed to sopping up as many US assets (mostly Treasury debt) as they had to, to prevent Greenspan’s inflation from causing the dollar to depreciate against the yuan. So I’m not sure if that would be reflected in the figures of “global savings rate,” but surely it didn’t help things.

Jon Stewart Goes Off on CNBC

I think he is a bit unfair to Rick Santelli, but Jon Stewart–and his research staff–are awesome. This is a bit long but it’s really good. I watched it twice. (HT2EPJ)

This interview isn’t as good, but it’s still pretty good. Jon Stewart asks a great question about double-paying for the toxic assets, and then he makes a hilarious analogy about CNBC and the Weather Channel.

OK I Will Ignore DeLong, Starting…Now

I misspoke in the previous post when I said I was done nitpicking Brad DeLong’s posts. For how could I know that he would then devote an entire post to me?! (What timing.) Regular readers here will see right away the true hilarity in DeLong’s response. PLEASE be nice, guys. Let’s be the classiest commenters in the blogosphere. We already know we’re right (or at least we think we do). The point is to get innocent readers at DeLong’s site to question his preaching.

UPDATE: For DeLong readers who are coming here to see the original controversy, this is the post you want. It’s fine for DeLong to argue that Hoover followed Mellon’s advice in practice, but surely he should have mentioned the fact that his quotes from Hoover were written by Hoover to discredit Mellon.

Note to Self: Don’t Ever Let Brad DeLong Paraphrase My Views On An Issue

All right kids, I promise I will leave Krugman and DeLong alone for a while after I get this one out of my system. But I couldn’t help from posting a snarky comment at DeLong’s blog in response to his ridicule of an NRO post warning of hiking taxes on the nation’s most productive people. If you’re curious, just go read the DeLong post and then you can see my comment which I reproduce below:

I am not defending the NRO stuff, but I did find it odd that Prof. DeLong changed what they said. Here’s DeLong’s intro:

“The most deserving and valuable people in America, according to National Review, aren’t our firefighters, police officers, nurses, soldiers, and teachers. Instead, they are our lawyers, bankers, executives, and top salespeople.”

But then if you read the actual quotation he gives–you don’t even need to click through, it’s right there a few lines below in the quote he pasted in–the actual NRO person wrote:

“The doctors, lawyers, engineers, executives, serious small-business owners, top salespeople, and other professionals and entrepreneurs who make this country run…”

Look carefully at how DeLong changed the list of professions that the NRO writer was praising. He took out doctors, engineers, and small-business owners, retained lawyers and top salespeople, and then inserted bankers.

In other words, DeLong took out all the professions in the original list that most Americans think are good, he left in all the professions that most Americans despise, and then for good measure DeLong added a profession that right now people can’t stand.

An interesting pattern.

UPDATE: Concerned that I am being too harsh on poor DeLong, I reviewed the post again and then made this follow-up comment:

Whoops in fairness to DeLong I concede that Schiffren mentioned people putting in long hours at banks, so she therefore is praising hard-working bankers. But even so, DeLong still took out all of the “noble” professions from the list that Schiffren originally gave.

Recent Comments