Scott Sumner Slips

Long-time readers know that I am not a fan of Scott Sumner’s signature idea, namely that the Great Recession was caused by Ben Bernanke’s tight monetary policy. However, if you’re really an expert on my writings, you’ll know that I’ve said Sumner would be a very formidable debating opponent–much more than Krugman. Indeed, when I said Sumner was “insane,” I meant it as a (backhanded) compliment: Sumner can back up his “outlandish” (to me) views with all sorts of internally-consistent facts and arguments. It’s like you run into a guy who claims to be Napoleon, and you realize five minutes into the conversation that you can’t prove he’s wrong.

In that context, then, it’s refreshing to see Sumner slip. (This is just a re-hash of Sumner’s same slip back in 2011. I don’t know if he saw my response at the time.) It reassures me that he’s a man, and can be beaten…

Anyway, in a recent post, Scott is kinda-sorta taunting the people who warned of the housing bubble, last time around. Since a popular US housing price index is above its peak (in nominal terms) from the prior boom, Sumner wants to know if they think another crash is coming? (My answer is “yes,” and Scott at least concedes I am being consistent–he probably thinks I’m insane!)

Then to drive home just how goofy these bubble-theorists were, Scott asks them a bunch of provocative questions:

Is it possible that the housing boom was not a bubble? Is it possible that fundamentals (such as building restrictions and lower real interest rates) support much higher real housing prices during the 21st century than during the 20th century? Is it possible that the real problem was nominal, a fall in NGDP engineered by a monetary policy that (during 2008) held the Fed’s target interest rate far above the equilibrium interest rates? Is that why unemployment stayed low as housing construction fell in half between January 2006 and April 2008, and then soared when tight money pushed NGDP down in late 2008? [Bold added.]

Scott thinks he’s got a real zinger here. In fact, superficially it’s so good that Arnold Kling admitted defeat back in 2011 when Sumner made the same point. But as I pointed out at the time, Kling threw in the towel unnecessarily. Scott’s point blows up in his face once we pick better data. As with two of Krugman’s examples (here and here), the attempt to destroy a coordination-of-resources story (and replace it with a shortfall-in-demand story) actually turns against them. And since it was Sumner who picked this example, that gives it extra significance when it actually supports the Austrian (and Klingian) view.

First, let’s make sure we get what Sumner is doing. He’s saying that the casual association of the financial crisis of 2008, and more generally the Great Recession of 2007-2009, with the collapse of the housing boom, doesn’t actually work when you look carefully at the numbers. Specifically, between early 2006 and mid-2008, new home starts fell in half, while the national unemployment rate didn’t move up very much. See for yourself:

So, Sumner is arguing that *clearly* the slowdown in house construction has little to do with the onset of the Great Recession or the financial crisis that struck in September 2008.

Yet as I pointed out back in 2011, “new housing starts” isn’t the right metric. Clearly a much better test of the Kling/Austrian story–about workers needed to move out of construction and into other sectors, and this reallocation (or “recalculation” in Kling’s terminology) takes time–would be to look at *employment* in construction, and relate that the to the national unemployment rate. If you doubt me, here’s what Sumner himself said when he thought he blew up Kling back in 2011: “So housing starts fall by 1.3 million over 27 months, and unemployment hardly changes. Looks like those construction workers found other jobs, which is what is supposed to happen if the Fed keeps NGDP growing at a slow but steady rate.” So clearly, Sumner thought that the collapse in housing starts was a good proxy for construction employment.

But we don’t need to use a proxy for construction employment. We can use total construction employment itself. And when you compare *that* to the national unemployment rate…

…the fit is gorgeous. That’s exactly what Kling (or Murphy) require for their story. Not only does the story work for the crash, but the prior boom works too: The national unemployment rate falls, as more and more workers are sucked by the real estate bubble into construction.

If you’re trying to put your finger on the problem, it’s this: Sumner just assumed that a large drop in new housing starts went hand-in-hand with a large fall in construction employment. But as the data show, that’s not what happened. So no, there weren’t a bunch of “construction workers [who] found other jobs” because the Fed kept NGDP growth up.

If you want to offer various theories about why that should be, go ahead. It’s an interesting puzzle, presumably having to do with rates of growth, the fact that you build shopping centers etc. around new housing developments, that there is a lag for add-on work to newly constructed houses, etc. But, it’s not my job to explain *why* the collapse in new housing starts didn’t translate into a collapse in construction employment. Once we realize that, apparently, the one didn’t cause the other, then Sumner’s whole point falls apart. We are back to the original “common sense” view that it’s not a coincidence that the housing bubble collapsed, and then the financial crisis / Great Recession happened.

If you’re curious, the following sheds some light on it:

An Ironic Slip of the Tongue for Jordan Peterson

You guys think you’ve got me allll figured out. I’ve been pumping up Jordan Peterson, saying how great he is, and then his interview with Cathy Newman goes viral. You would expect me to share it with enthusiasm, yet I actually was underwhelmed by it (as I think I’ve said before on the blog).

Anyway, David R. Henderson and I were discussing it over email. (BTW, David has a nice post about JP at EconLog.) I said that even though Newman was obviously being combative, there were a few key parts where I thought JP was not trying to get his point across to someone who disagreed with him. Even though it was perhaps hopeless to try to persuade Newman herself, there could be sincere feminists watching who honestly would not have gotten his points.

David encouraged me to re-watch the video, and every time Newman said something, I should stop the video, and then jot down what I wished JP had said in response. Then, play the video to see how he did.

It was an instructive exercise, and David was right, JP did better than I remembered. It was actually only in two or three exchanges where I thought he missed an opportunity, and there were other places where he was amazing. So overall, he did fine. (And of course the “ha–gotcha” near the end will go down in Hostile Interview history.)

But, the one major goof I noticed: Start at 5:40 and JP clearly says, “…multivariate analysis of the pay gap indicate that it doesn’t exist.”

OK, we all know what he means by that. He takes “pay gap” to mean “a disparity in pay that can only be explained by irrational sexism.”

Yet later on, starting at 8:07, Newman says, “OK so rather than denying that the pay gap exists, which is what you did at the beginning of this conversation, shouldn’t you say to women…” and then she followed up on his nuanced position about being assertive.

At this point JP goofs. He says at 8:20–while he literally points his finger at her–“But I also didn’t deny that the pay gap existed. I denied that it existed because of gender.”

No, that’s not correct. He literally said the multivariate analysis indicated that it didn’t exist.

And then, to compound the problem, he then went on to lecture her about how he’s “very very very” careful with his words.

Anyway, we all get what he meant, and he had a very defensible, correct position on the substance. But this is a good example of what I mean, when I say that I actually don’t think he demolished her as much as some of his fans believe. And if someone went into this interview thinking he was slippery, they would see “confirmation” of that (incorrectly, in my mind, to be sure).

As I’ve said before, I think JP’s Biblical lectures are absolutely amazing; I can’t believe a thinker like him exists. I personally know people who have benefited from his work, as in, it’s helped them in their personal lives. So I’m mostly just posting this because it’s ironic.

God Saves Us; We Don’t Save Ourselves

This is a famous blessing that comes out of Numbers 6:

22 The Lord spoke to Moses, saying, 23 “Speak to Aaron and his sons, saying, Thus you shall bless the people of Israel: you shall say to them,

24 The Lord bless you and keep you;

25 the Lord make his face to shine upon you and be gracious to you;

26 the Lord lift up his countenance upon you and give you peace.

27 “So shall they put my name upon the people of Israel, and I will bless them.”

Regarding the part I put in bold, here is what commentator David Guzik says: “To be kept by the Lord is blessing indeed. Some are kept by their own sin and desire, some are kept by idolatry and greed, and others are kept by their own bitterness and anger. But to be kept by the Lord insures life, peace, and success.”

As my cousin and I were studying this, it reminded me of Jesus’ prayer to His Father, from John 17:

1When Jesus had spoken these words, he lifted up his eyes to heaven, and said, “Father, the hour has come; glorify your Son that the Son may glorify you…

6“I have manifested your name to the people whom you gave me out of the world. Yours they were, and you gave them to me, and they have kept your word. 7Now they know that everything that you have given me is from you. 8For I have given them the words that you gave me, and they have received them and have come to know in truth that I came from you; and they have believed that you sent me. 9I am praying for them. I am not praying for the world but for those whom you have given me, for they are yours. 10All mine are yours, and yours are mine, and I am glorified in them. 11And I am no longer in the world, but they are in the world, and I am coming to you. Holy Father, keep them in your name, which you have given me, that they may be one, even as we are one. 12While I was with them, I kept them in your name, which you have given me. I have guarded them, and not one of them has been lost except the son of destruction, that the Scripture might be fulfilled. 13But now I am coming to you, and these things I speak in the world, that they may have my joy fulfilled in themselves. 14I have given them your word, and the world has hated them because they are not of the world, just as I am not of the world. 15I do not ask that you take them out of the world, but that you keep them from the evil one.a 16They are not of the world, just as I am not of the world. 17Sanctify them in the truth; your word is truth. 18As you sent me into the world, so I have sent them into the world. 19And for their sake I consecrate myself, that they also may be sanctified in truth.

20“I do not ask for these only, but also for those who will believe in me through their word, 21that they may all be one, just as you, Father, are in me, and I in you, that they also may be in us, so that the world may believe that you have sent me.

As you can see quite clearly from the parts I put in bold, Jesus is NOT saying, “Father, thank you for letting me set a bar of minimum goodness, and granting me fellowship with those whose sin fell below the veto mark.”

Even Judas is lost NOT because he is a “worse person” than Peter or the other apostles, but rather because he is the “son of destruction” (or “son of perdition” in some translations), i.e. he is of the devil, and his betrayal of Jesus and loss is necessary to fulfill the prophecies of the Old Testament. Even here, it’s not that Jesus was saying, “Well let’s see how this Judas guy turns out…YIKES he’s a bad one, he needs to go.”

Scott Sumner, Trade Deficits, and Dark Matter

Scott Sumner at EconLog pounced at the red meat I waved in front of him. (I had sent him Trump’s ludicrous tweet on trade wars.) One of Scott’s points was very interesting, and I want to make sure readers understand the claim.

Specifically, Scott wrote, “4. Most people assume that the US runs a persistent trade deficit. But if the trade deficit really were persistently negative, properly measured, then this time series should also be negative and falling. Instead, the US surplus on investment income is strongly positive and rapidly increasing. If this is what it means to be a “debtor nation”, then lets have lots more debt!”

He then presented a chart, but I’ll give a more comprehensive one below:

(So what Scott showed was more-or-less the green line in my chart above, although it’s not exact–perhaps his wasn’t seasonally adjusted?)

Another clarification: I think technically Scott should’ve been talking about the current account deficit, not the trade deficit.

Anyway, the basic idea is this: Over time, the flow of annual income that Americans earn from their foreign assets held abroad, keeps growing more than the flow of annual payments that Americans must make to foreigners on their U.S.-based (but foreign-owned) assets. This is not what you might have expected, since the U.S. has been running large and persistent current account deficits for decades. A current account deficit means that the amount Americans earn on their foreign assets PLUS their sales of goods and services to foreigners (i.e. exports), is less than the amount Americans spend on imports and on making payments to foreigners for their US-held assets.

So what Scott is saying is that there must be something screwy with how we measure current account (sic) deficits.

This is the “dark matter” thesis of Hausmann and Sturzenegger, from 2005. They argued that superior US know-how explains why American investors can earn higher returns on Foreign Direct Investment abroad, than foreigners can earn abroad. So effectively the foreign savers invest in the US at a low yield, and Americans then invest abroad at a higher yield, earning the spread. That seems fine when hedge funds or commercial banks do it, but in terms of the conventional trade accounting it looks “unsustainable.” Here’s an analogy I made back in 2007 (in an essay in which I made some unfortunate and snarky predictions at the end):

Suppose a stock speculator spies a company that is undervalued. He invests $100,000 in the company, waits one week, then sells the shares for $105,000. Then he uses the profit to buy his wife a necklace.

His wife…is quite furious. “How much did you earn selling your labor or merchandise last week?!” she demands. He thinks for a moment and realizes the answer is “None.”

The speculator’s wife continues with the interrogation: “And how much did you spend on assets this week?” The husband replies that he spent $100,000 on stock shares.

She then demands, “And how much did outsiders spend on assets that you owned during this same time frame?” After a pause—for he’s not used to thinking in these terms—the husband informs her that outsiders invested a total of $105,000 in assets that he owned.

The wife starts to tremble with rage. “Do you mean to tell me that you financed this $5,000 bauble purely by increasing your liabilities to people outside of this household??”

So to be clear, I’m not now saying, “Sumner is right, it’s dark matter, everything is fine.” I’m just clarifying the argument.

For example, I could flip things by imagining a guy telling his wife, “I’m a smart investor, babe. I borrowed $10,000 from credit cards at an introductory APR of 1.99%, and I invested $9,000 of it into 30-year bonds yielding 3%. Then I spent the remaining $1,000 getting you some new shoes and myself a new sport coat. Some people call this ‘living beyond my means’ but I call it leveraging dark matter. I mean, I’m only paying $199 in finance charges, while I’m earning $270 in interest on my Treasuries. It’s all under control.”

Podcasts Are Here

==> Episode 48 of the Lara-Murphy Show covers Chapter 1 of our new book (with Nelson Nash).

==> Not sure if I already posted, but: Episode 127 of Contra Krugman involves Krugman calling Republicans liars. But, tune in for the banter between Tom and me.

Murphy Triple Play

==> In the Washington Examiner I argue that Pope Francis “has it wrong on global poverty and its cure” (their title).

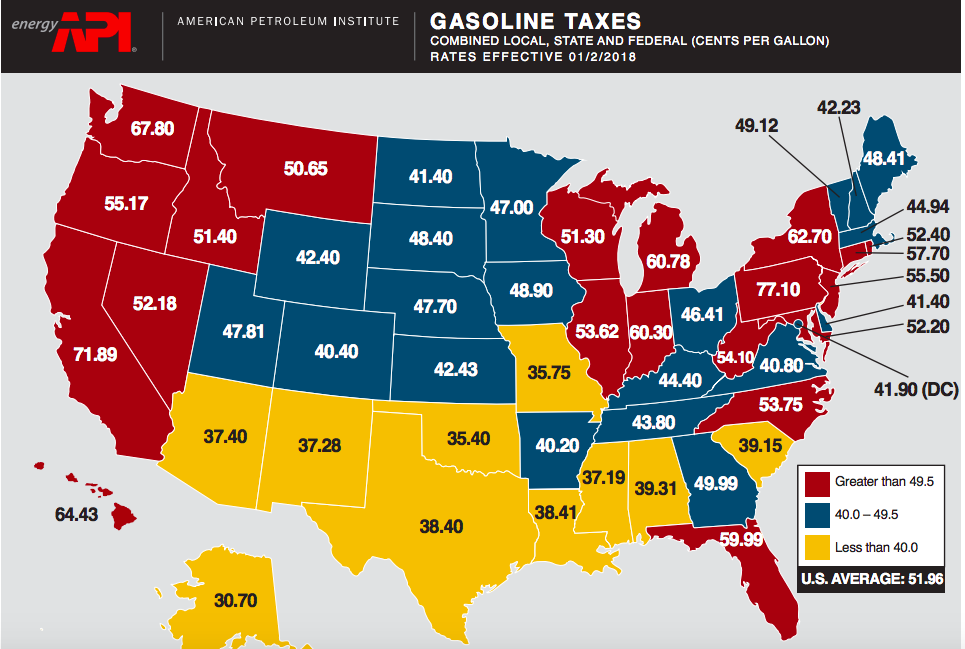

==> At IER, I argue for road privatization, rather than a gas tax.

==> In a follow-up piece, I explain that the gas tax is already quite high, when we factor in taxes at all levels. Here’s a graph from API:

Murphy at Ramapo College and then Yale

Tonight (Monday Feb. 26, 2018) I’ll be presenting at Ramapo College on the economics of climate change. Here’s the info, and my understanding is that there will be a link to the live presentation once it starts.

Then tomorrow (Tuesday Feb. 27, 2018) I’ll be debating at the Yale Political Union on “The Free Market Can Provide an Effective Solution to Climate Change.” Here’s their page, even though my event seems not to be formally listed (!). It’s not going to be recorded but I think anybody can attend.

Recent Comments