Krugman Can’t Stand People Who Switched Their Fiscal Policy Views From the Bush Years

[UPDATE below.]

I’m sure most people wouldn’t have caught this, but that’s why you kids have me on the job. In trying to show everyone how intellectually dishonest Republicans are, Krugman stretches so far that he throws his back out. Follow me:

In discussing a Pew poll on evolution, Krugman argued that Republicans moved their views during the Obama years purely as a signaling device, to show their support for their “tribe.” (Note: We’ll come back to this on Sunday; let’s not discuss evolution right now, because the point here is Krugman.) Then he likened this to how Republicans have also (allegedly) changed their views on countercyclical policy, too. He wrote:

As recently as 2004, the Economic Report of the President (pdf) of a Republican administration could espouse a strongly Keynesian view, declaring the virtues of “aggressive monetary policy” to fight recessions, and making the case for discretionary fiscal policy too. (Naturally, the only form of discretionary fiscal policy considered was tax cuts, but the logic was straight Keynesian, and could have been used to justify public works programs equally well.)

Oh, and the report — presumably written by Greg Mankiw — used the “s-word”, calling for “short-term stimulus”.

Given that intellectual framework, the reemergence of a 30s-type economic situation, with prolonged shortfalls in aggregate demand, low inflation, and zero interest rates should have made many Republicans more Keynesian than before. Instead, at just the moment that demand-side economics became obviously critical, we saw Republicans — the rank and file, of course, but economists as well — declare their fealty to various forms of supply-side economics, whether Austrian or Lafferian or both. Compare that ERP chapter with the currency-debasement letter and you see a remarkable case of intellectual retrogression.

I don’t want to spend too much time on this, but it is quite remarkable just how wrong and hypocritical the above commentary is. For example:

(1) Krugman thinks he is documenting a shift in Republican views on economic policy, presumably because of the change in Administrations (from Bush to Obama). But Mankiw didn’t sign the currency debasement letter, and I don’t ever remember him saying since 2008 that he thought Bernanke had no role to play in the recovery. Furthermore, the rank-and-file Republicans who oppose aggressive monetary policy today, certainly were not parsing the “Economic Report of the President” back in 2004. That’s not something Rush Limbaugh read on the air. And if, for some crazy reason, you had asked the average Fox News fan back in 2004, “Do you think it would be a good idea for the Fed to create more than $2.5 trillion so it can buy assets from the feds and Wall Street bankers?” the answer would have been a resounding, “No! That would wreck the dollar!” So even on Krugman’s own terms, there is zero shifting going on here.

(2) Krugman is completely full of it when he says that the 2004 case for fiscal stimulus is Keynesian. From the summary provided at the report: “Tax cuts can boost economic activity by raising after-tax income and

enhancing incentives to work, save, and invest.” So what is so inexplicable about going from that position in 2004, to a Laffer position today? That’s the same position. I realize Krugman is incapable of thinking that tax cuts can do anything except give taxpayers more money to spend, but that’s not the actual reason conservatives/libertarians favor tax rate reductions as a way to boost economic growth. (Perhaps Krugman should start reading people with whom he disagrees? Then he wouldn’t have to get his notion of conservative tax policy from a guy in a bar.)

(3) Mankiw didn’t sign the currency debasement letter, but even if he had, there is nothing in it that contradicts the 2004 report. The letter isn’t making blanket statements like, “Monetary policy can never provide countercyclical relief.” Rather, it is very specifically saying that as of November 2010, the people signing the letter thought the Fed had already done what it could, and that further QE would risk doing more harm than good. Maybe that’s right, maybe that’s wrong, but that doesn’t explicitly contradict someone arguing in 2004 that Greenspan’s lowering of interest rates cushioned the blow from the dot-com bust.

(4) I believe I have demonstrated that Krugman is on very shaky ground when trying to document a major (and politically convenient) shift in the opinion of Republicans on the effects of monetary/fiscal policy. In contrast to Krugman’s examples, I can think of a much better case of an economist who has done a complete 180 in his views since the Bush years, and moreover in a way that very conveniently lines up with his partisan stance. But in this particular economist’s view, this isn’t evidence of his perfidy; rather, he is to be congratulated for changing his position, because he has a better moral character than his foes. If anyone tries to bring up his previous writings, this economist dismisses the move as an unfair ad hominem attack, irrelevant to the correctness of his current view. Do I need to tell you who this mystery economist is? Hint: It’s not Greg Mankiw.

UPDATE: OK, in response to a comment I went and looked more carefully at the exact defense given in the Economic Report from 2004 for the earlier Bush tax cuts. And it’s true, on pages 43-44, that the author of the report (Mankiw?) gives a “Keynesian” justification in that they increase after-tax income and hence boost aggregate demand. The report then goes into supply-side considerations, but Krugman is correct if he says that there exists a Keynesian justification for tax cuts in the 2004 report. Even so, that doesn’t really document a shift in any individual Republican’s position; Mankiw (the author?) hasn’t changed since then, as far as I know, and the average Republican wasn’t running around in 2004 saying, “I just love pages 43-44 of Bush’s report!”

Note that I’m not saying Krugman has a monopoly on switching his opinions with the party in the White House. I’m just saying he really hasn’t documented his claims of massive Republican shifting on matters of economic policy in this post.

Is Market Monetarism Pining for the Fjords?

Scott Sumner has a new post at EconLog saying that Keynesianism isn’t just resting (in reference to the famous Monty Python “Dead Parrot” sketch). Scott does a great job busting Mike Konczal, who earlier in 2013 had said the year would be a great test for market monetarism vs. Keynesianism. Since the Keynesian warnings about the horrible effects of the sequestration (and government shutdown) totally blew up in their faces (I will document this in a separate post at Mises Canada), Scott is perfectly justified in raising his eyebrow at Konczal’s victory dance now that 2013 has closed.

But being the paragon of mercy and understanding that I am, I wanted to understand how it was possible that Konczal and Sumner could look at the same data, yet each walk away with an opposite verdict. And you know what? The answer is that Konczal wasn’t looking at Keynesianism per se. Rather, he was looking at NGDP growth, and concluded that the story didn’t match what Sumner needs. Specifically, Konczal wrote: “2013 brought us a fiscal deficit that closed far too fast, NGDP growth and inflation falling compared to previous years…”

And here’s the NGDP graph that Konczal linked:

Does that surprise anybody else? From reading Scott’s blog all these years, I sort of expected “the tightest monetary policy since Herbert Hoover” to show really low annual NGDP growth during our abysmal recovery, but that it started picking up in 2013, the year that Scott tells us has been vindicating market monetarism. (Remember, Scott’s original ideal target rate for a healthy economy was 5% NGDP growth.)

Now I know, I know, Scott advocates level targeting, meaning that we have to catch up to where NGDP would have been right now, had we never hit the catastrophe of falling / slowly rising NGDP in 2008-10. But my point is, of course Scott can reconcile the data to his story; anybody can do that. (It’s why Krugman, Scott, and I all think the past 5 years have totally vindicated our basic stories.) But be honest: Did you expect the NGDP graph to look like the above?

Let me give an even better test that puts more pressure on Scott: If his theory is correct, then we should have seen price inflation and real GDP growth moving cyclically, since 2008. (I’m not just speculating; I’ve seen Scott say this explicitly, for example when a QE announcement increases inflation expectations and Scott says it’s proof that QE is “working.” Please give me a link if you can find one.) That’s because in Scott’s view, extra demand (from looser monetary policy) will mostly get sopped up by an increase in real output, but it will also show up in accelerating price inflation.

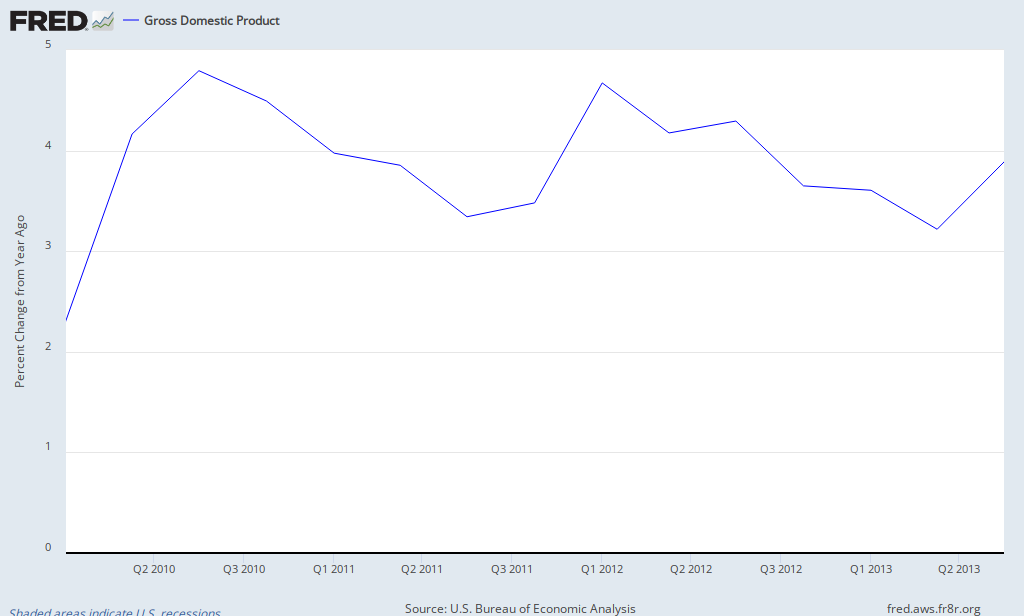

And yet, I think we arguably see the opposite:

In the above graph, we see that from 2010 onward, there are three distinct periods where the movements in price inflation and real GDP growth are mirror images. To repeat, that’s the opposite of what Scott’s story requires. They should be moving together, at least while we remain below “potential GDP” (or full employment or whatever term Scott prefers).

Don’t get me wrong, I have no problem with Scott dismissing the above chart as irrelevant, or even somehow (heroically) arguing that it just proves how right he is. That’s because in macroeconomics, there are 57 moving parts, and all of us (Austrians, Keynesians, and Market Monetarists) can always tell a story after the fact.

Rather, my purpose in this post is to get Scott and his followers to see that if you just entertain the premise for one moment that our economic woes aren’t because of “tight money,” there are lots of data to comfort you.

When it comes to macroeconomic theory and the data, believing is seeing.

New NYC Mayor Not Horsing Around

I saw someone mention this on Facebook, and thought it was satire: New York City Mayor-Elect Bill de Blasio wants to completely ban horse-drawn carriages from the Big Apple, saying it’s cruel to animals. From the CNN story:

Horse-drawn carriages could soon be a thing of the past in New York City’s Central Park after Mayor-elect Bill de Blasio announced plans to outlaw the popular tourist attraction once in office.

“We are going to get rid of horse carriages, period,” de Blasio said at a news conference Monday, saying that the practice is inhumane.

Beyond the specific pros and cons on this issue–such as the fact that horse-drawn carriage rides around Central Park are a staple of the imagery–is the audacious presumption that this is the type of thing a new mayor has the power to do. (Technically de Blasio needs City Council to approve his proposal.) I would be curious at this point to see a poll of Americans asking, “Do you think there is any sphere of human life whatsoever that isn’t in principle under the jurisdiction of some level of government?” Except for religious beliefs, I think a majority would say, “No.”

Potpourri

==> I had briefly toyed with the idea of ignoring Krugman in 2014, but then I realized: You guys want me on that wall, you need me on that wall. For now: A while ago someone exclaimed with horror in the comments here that Krugman was referring to his opponents as cockroaches, and that this was the type of dehumanizing move in which Nazis engaged etc. I rushed to Krugman’s defense and clarified that no, strictly speaking, Krugman was referring to cockroach ideas; he wasn’t calling his actual opponents cockroaches. Well, Krugman just put up a post titled, “Jean Baptise Say, Cockroach.” (But maybe that’s just because nobody can remember that famous idea with which Say is associated, so Krugman had to make it about the man, not the idea?)

==> I’ve karaoked with one of these people.

==> I see that I have been focusing too much on Krugman, and not enough on Scott Sumner. Now the latter has a platform at EconLog. But guys, I can prove that Scott’s analysis is wrong: After all, we still have a horrible economy. So clearly Scott’s blog output has been suboptimal, by definition, regardless of whatever nice things David has to say about him.

==> This Walter Oi sounds like an absolute riot. David R. Henderson provides a tribute, and so does Steve Landsburg. From Steve’s post:

He must have cultivated these traits for a very long time, because the Economics Department at the University of Chicago has a long (but sometimes broken) tradition of awarding, at the end of each academic year, the “Walter Y. Oi Award” to the graduate student who has asked the most irrelevant question — presumably in commemoration of something Walter asked in his own student days at Chicago over half a century ago. I’m not sure anybody knows what that question was, but according to one rumor, it came in the midst of a fairly technical lecture in Milton Friedman‘s Price Theory class, where Walter suddenly raised his hand and asked “Do you just make this stuff up as you go along, or what?”.

Yet More on Tyler Cowen on Bitcoin

Say what you will about him, Tyler is a sport and retweeted this guy, who has a “Tyler vs. Tyler” post up. The money excerpt:

…Tyler is able to derive the following theorem: “the value of WitCoin should, in equilibrium, be equal to the marketing costs of its potential competitors.” To put this in simpler terms, Bitcoin’s network externalities should drive the value of Bitcoin. Tyler says in theory you could argue that Bitcoin’s price reflects these fundamentals, but he doesn’t buy it. Therefore, Bitcoin is due for a crash.

I agree with Tyler’s theorem, or at least my simpler paraphrase. Nevertheless, I am not so convinced by Tyler’s conclusion. As a wise man once said (in an addendum to the same post), “expected price changes usually get compressed into the present and [] an overall expected rate of return equality must hold.” So the network externalities that matter in determining Bitcoin’s equilibrium price are mostly expected future ones, not present ones. Is it so unreasonable to expect that future Bitcoin network externalities would equal $20 billion or more?

Well, that depends on whether network externalities in currencies in general tend to be strong or weak. To answer that question we might turn to an expert such as Tyler Cowen, who in 2011 argued (1, 2) that currency network externalities are so strong that Bitcoin couldn’t possibly succeed. Now Tyler is arguing that currency network externalities are so weak that Bitcoin can’t possibly succeed. Who are we to believe?

Beautiful. I wouldn’t change a word, except I’d put in “Whom” for “Who” at the end there…

Since I see that others are linking to my wisealeck previous post about Tyler’s commentary, let me clarify something: I was perhaps a bit too flippant, when I argued that Tyler’s whole argument rested on people being willing to sell something for $400 when they were sure it would quickly appreciate to $500.

In context, Tyler was talking about issuers of competing cryptocurrencies. So yes, maybe a new issuer would be willing to sell “undervalued” money, in order to get people to hold it. For an analogy, if you had a foolproof USD printing press in your basement, you would have no problem selling $100 counterfeit bills for only $90 in genuine USD on some type of black currency market, to account for the risk or whatever. By the same token, if the only way I could get the public to accept BobCoin were to issue it “below par,” then it would still make sense for me to do that, rather than hold all the BobCoin myself, forever.

Yet even though this type of reasoning is what Tyler had in mind, you still get the odd result that nobody else would be willing to spend the cryptocurrency, at least until all of its units had been issued and it no longer appreciated in price faster than the market rate of interest. But then that means there would be no liquidity in these alternate currencies, until they had been fully issued, at which point we would have to see what their market would be, for the first time, in order to get a sense of their purchasing power. This outcome clearly doesn’t make much sense.

All in all, I think the discussion surrounding Bitcoin shows that economists really don’t have a firm grasp on how to think through these issues. This shouldn’t be too surprising, since we all spent a few weeks arguing about whether QE would cause prices to rise or fall–something Nick Rowe cleverly likened to an econ equivalent to the Sokal hoax, except it wasn’t a hoax!

Krugman Once Again (Unwittingly) Confirms What the Critics Warned of ObamaCare

Unfortunately I can’t find it now, but at some point in 2013 Krugman was making the argument that deep down, Republicans knew ObamaCare would actually be a good thing, and that’s why they were fighting it tooth-and-nail before implementation. For if ObamaCare actually were a disaster, Krugman continued, then it would be plain as day and Republicans would score a major political victory repealing it.

Well, we can all see how silly that particular argument is. What’s interesting is that Krugman himself knows it doesn’t work. I’ve linked to him letting the cat out of the bag before, but look at his latest, where he’s even more blunt:

Perceptions about health reform are in an interesting place. Just about everyone on the right is still living in October…and is waiting to move in for the kill after the whole thing collapses. Meanwhile, a funny thing has been happening: enrollments surged this month, to such an extent that the original expectation of 7 million people signed up via the exchanges by the end of March no longer looks crazy.

OK, the usual caveats: we don’t know how many of the people signing up via the exchanges are replacing existing policies, and we don’t know how much trouble there will be when people start trying to use their new insurance. On the other hand, we know that there are a substantial number of people buying ACA-compliant policies directly from insurers, who don’t show up in the numbers yet.

And while 7 million has become the number to match or beat, the truth is that it doesn’t matter too much if “only” 6 million sign up via the exchanges, plus millions more who are signed up under expanded Medicaid. Even a slightly disappointing first year will still offer enough people benefits to make reform politically irreversible.

At this point, we have more than 2 million signed up via the exchanges and more than 4 million added to Medicaid. Both numbers will grow a lot over the next three months. This is pretty close to the end game. [Bold added.]

Notice what Krugman needs for “end game”: Just several million people to start getting benefits from the government. Yep, that’s exactly what (most) of the critics of ObamaCare said: Once you start giving federal subsidies to millions of people, that will create a politically unstoppable interest group who will prevent repeal. It’s like with Social Security or (for that matter) Medicare: It doesn’t matter how much damage the programs do to the country as a whole, once they are up and running, it’s impossible politically to get rid of them.

In case you think I’m exaggerating, look closely at Krugman’s caveats: The only things he mentions are that maybe we’re miscounting the number of people who are getting insurance who didn’t have it before (since some of the gross numbers are just replacements of old policies), or that there could be a logistical snag in actually using a new policy. (For example, maybe you need surgery but the hospital and the government computers can’t agree on who you are.)

But nowhere does Krugman mention:

(A) “Supposing that the ACA doesn’t drive up premiums so much that people are outraged…”

(B) “Supposing that the institution of death panels doesn’t horrify too many Americans…”

(C) “Supposing that the increase in wait times for MRIs doesn’t annoy enough voters…”

etc. In other words, Krugman doesn’t mention any of the things that might actually show how awful ObamaCare is, for the country as a whole. On the contrary, Krugman says–and I agree with him–that the only real consideration is to get millions of new people dependent on the government for their health insurance. Then it’s game over.

Ironically, the healthcare.gov debacle was arguably good for ObamaCare, though awful for Obama. It reduced the bar so low that critics were hoping, “Hey, the feds are so freaking incompetent, maybe they won’t even be able to technically implement this thing!” while proponents were saying, “Let’s just hope we can sign people up, let’s just hope we can sign people up, let’s just hope we can sign people up.” At this point, if one guy gets stitches in 2014 under ObamaCare, Krugman’s going to do a dance in the endzone.

Potpourri

==> I am going to be at the First Annual “Save Long Island” Forum in mid-January. If you buy your tickets in 2013, they are 50% off. I will be debating “Money Masters”‘ Bill Still Friday night, and there are lots of interesting speakers/performers.

==> Tucker talks teetotalling in a tux.

==> The NSA really is doing its best to ensure that no terrorist ever again attacks us for our freedom.

==> On Facebook all the h8ers picked apart various entries in this compilation, but hopefully at least some of these moments of compassion trumping violence are real.

==> John Carney has some Christmas fun at my expense (as well as other econ bloggers).

==> And you guys wonder why I associate with Gene Callahan? Because sometimes he attacks Brad DeLong, not just Rothbard.

==> A great point by David R. Henderson on how redistributionists never want to go beyond US borders.

==> Don’t get me wrong, this lady’s tweet was stupid as well as racist, but oh man–can you imagine your whole career collapsing, with the world watching, while you were blissfully unaware on a flight? As one who often engages in deadpan jokes, these cases (like the Duck Dynasty guy) always make me uneasy.

==> I have no inside info on this entrepreneurship program in Africa, but I told the guy I’d pass along the info.

==> I realize I’m biased, but I thought this was a pretty good zinger I had against Scott Sumner.

==> Glenn Jacobs (“Kane”) has reservations about Bitcoin. You have no idea how much the cool-kid libertarians want to convince him. (I know because they hang out with me, sort of like when the cool kids in high school couldn’t buy beer yet so they’d let a nerdy 21-year-old go to their parties and such.)

==> Speaking of Bitcoin skeptics, I thought this guy had a good response to one of my recent posts.

But the Progressives Told Us Abenomics Would Be Good for Japan

Chris S. gave me the idea for my latest post at Mises Canada, by pointing out that Japan’s Cabinet just approved another “stimulus” package to help its faltering economic recovery. Chris reminded me that earlier in the year Krugman had held up Japan’s “Abenomics” as a model for US deficit hawks to follow.

As I point out in the post, despite strong growth early in the year, 3rd quarter real GDP in Japan grew at 1.1 percent. In contrast, in the US it grew at 4.1 percent. Do you remember how many people warned us of the awful impact the budget sequestration, and the shutdown, would have on our tepid recovery?

Look, we can fiddle with these numbers all we want, and I’m not saying the US economy is great right now, by any stretch. What I am saying is that you shouldn’t believe the Keynesian progressives who act like they’ve got a monopoly on empirical evidence. As I document in the Mises Canada post, Krugman, Yglesias, and Dean Baker were really happy when the numbers seemed to be going Abe’s way, and said it showed the success of his deficits and inflation. So are they going to admit they were wrong now? Of course not. This will just prove that Abe didn’t go far enough, and that the US economy was–thank heavens!–on more solid footing than any Keynesian forecaster realized, back when they warned how awful sequestration would be.

{kind=link}

Recent Comments