I Stand Athwart the Blogosphere, Yelling Stop

I waited several days to write about this, because it may sound like I’m calling for someone to be fired when that’s not my intention. All I want to do is point out that it’s weird that on one of the leading classical liberal / free-market economics blogs, the resident monetary excerpt applauds the Russian central bank for letting consumer price inflation break 16 percent.

Furthermore, when explaining how the Russian central bank maintained a good labor market despite a collapse in oil prices, the resident free-market monetary expert quotes the following with no criticism:

To maintain reserves when the oil price began to fall, Ms Nabiullina [head of the Russian central bank–RPM] accelerated a plan to allow the rouble to float. It fell by 40% against the dollar in 2015 alone. Propping up the rouble would have been popular, since it would have preserved ordinary Russians’ purchasing power, but it would have meant burning through the country’s reserves again. Instead the CBR channelled dollars to sanction-hit banks and energy companies, to help them repay external debt. Reserves have also been used to finance the budget deficit. As oil prices recover, so the CBR is again accumulating reserves, with a view to hitting the $500 billion mark once again.

Now to be sure, I have been following Scott Sumner’s writings since 2008, so I understand exactly what led him to write his post. He’s not “for” price inflation, rather he’s “for” doing whatever it takes to keep NGDP rising, even if that means double-digit consumer price inflation.

And regarding the block quote above, it’s certainly not that Scott is in favor of the Russian central bank channeling dollars to banks and energy companies, but rather that he was so busy praising them for having the courage to let price inflation break 16 percent, that he didn’t want to distract EconLog readers by criticizing the bailouts of major players.

While I’m complaining, let me bring up two other points:

==> As David R. Henderson noted in the comments, Scott was taking credit for NGDP targeting even though he (initially, at the time he first posted) had exactly zero data on Russian NGDP. It would be as if I heard that some foreign country had a big drop in its unemployment rate and I said, “Although I haven’t been able to find any news accounts of policy changes, the drop in the UR is evidence that they must have improved their score on the Economic Freedom Index.” I am pretty sure I wouldn’t write something like that.

(For what it’s worth, Scott later found out that “NGDP growth slowed from 9.6% in 2014 to 3.2% in 2015, to a predicted 5.8% in 2016.” Is that really NGDP targeting? I think if the unemployment rate had skyrocketed in 2015, Scott could quite plausibly have claimed, “Well what the heck did they THINK was going to happen, letting NGDP growth plummet two-thirds in a year?!”)

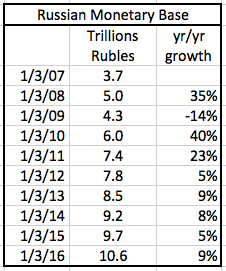

==> Scott’s preferred metric is of course NGDP growth, but sometimes “when in Rome” he’ll switch to talking about policy rate hikes or cuts as a proxy for central bank tightness or looseness. Yet the one thing he NEVER talks about is the quantity of money. For example, in this post about the Russians being much better central bankers than the Americans because the former were willing to let their currency fall and CPI to hit double digits, nowhere does Scott compare what happened with the monetary base in the open-minded Russians versus the tightwad Americans.

And yet, if this link is accurate, it turns out that we have the following stats for Russian monetary base:

If you go back and look at Scott’s second chart, when he was praising the Russians for letting inflation increase sharply, the big jump occurred in the end of 2014 and throughout 2015. But glancing at the table above, we see that this is actually a period when the Russian central bank was relatively tight, compared to its normal policy (save for the big plunge over 2008).

Yet again, had the Russian unemployment skyrocketed in 2015, Scott could quite plausibly have complained, “Well what did they THINK was going to happen?! Monetary base growth was far lower than it had been just a few years earlier. How are people supposed to sign long-term contracts when the Russian bank is inflating at a rate of 23% through 2010 but 5% through 2014?”

In closing, let me just say that besides the weirdness (to me at least) of a classical liberal blogger praising double-digit price inflation, it also seems weird to me that today’s market monetarists never even bother talking about the quantity of money. I’m always having to go look it up and see how the quantity of money relates to the market monetarist interpretation of an event, since that’s the last thing market monetarists care about.

Let me vainly try to forestall an obvious retort from Scott’s fans: Yes, I KNOW that Scott thinks interest rates and the growth in monetary base can be misleading policy indicators. But as we saw in this very episode, Scott will cite NGDP growth as doing the trick, without even knowing what the numbers are, and even though the numbers (once we find them) are just as (or even more?) consistent with a story about the bank deviating from Scott’s recommended policy and slamming on the brakes to try to arrest the ruble’s plunge.

What are you getting out of this chicanery, Murphy? Had there been no plunge in NGDP growth, unemployment in Russia would now be below its all-time low, which was in August 2014.

Yes, Sumner was wrong not to look up NGDP data first.

Sumner was shooting from the hip and he turned out to be wrong. The end.

BTW, Murphy, what the heck is happening to manufacturing productivity:

https://research.stlouisfed.org/fred2/graph/?g=Vzx

What you’re looking at here is (Mostly) a phenomenon in non-durable goods, if that helps elucidate it.

Dang it I messed up the link

But even the durable goods productivity has experienced stagnation over the past couple years.

Hm, the capacity index for manufacturing is also pretty stagnant. Took a big hit during the recession, still hasn’t recovered. Overall it’s not much higher than in 2000. It’s a conundrum.

Sumner:

“Ultimately living standards depend on production, which depends on employment. It does no good to preserve real hourly wages, if there are no jobs”

That right there is Sumner’s problem. Keynesian Konfirmed.

Sumner once talked about the money supply. Remember the post about inflation of the money supply in the US during the 1920s? That because the Fed was not LOOKING at M2 or M3 during that time, that this meant there was no significant increase in the money supply and could not have been a factor that explained the subsequent market correction in 1929?

——————-

From econlog:

“If the Fed had allowed inflation to rise slightly as RGDP slowed during the housing bust, then NGDP growth would have been more stable. Workers would have seen a reduction in real wages, but total employment would have been higher. With more people working, RGDP would have been higher, and since RGDP equals real income, Americans would have (paradoxically) had higher total real incomes, despite having lower hourly real wages.”

Sumner’s problem is that he is unable to distinguish between individuals and aggregates. Notice in this passage above we are to ignore the individul workers who experience a reduction in real wages, and focus instead on any increases in RGDP. In other words, we are to ignore the fact that “Paul” is less able to purchase goods, and instead focus on the fact that “Peter and Paul” is more able to purchase goods. “Paul” is worse off, and “Peter and Paul” is better off.

This is just collectivism. Sacrificing individuals for the sake of “society”.

And then we are to ignore the malinvestment generated by this as well.

Fair comment, not a problem unique to Sumner though. It probably would be the standard paradigm right now, although perhaps if you keep pointing it our more people might start wondering why.

I’ll give Sumner the benefit of the doubt and say that he thought “Paul” was going to be worse off anyhow, so might as well save “society” which is better than nothing. At least Sumner is willing to point out there is a problem with employment in the USA right now, the mainstream seems to be cheering the Obama recovery.

I think Sumner’s policy prescription has a different issue with it. He says, “If the Fed had allowed inflation to rise slightly” but it wasn’t for lack of trying. Interest rates were virtually at zero, there was a huge Obama fiscal stimulus, biggest deficits in the history of the USA, the Fed created *A LOT* of extra money. What Sumner is saying here is same as Krugman — if only they did more!

There’s got to be some logical point where you scratch your head and say, “Did this work at all?”

This is one of the first things I really ever heard about Keynesianism (since all the hipster leftists of the early 70s were members of the Khmer Rouge and Keynesianism was “capitalism”). We have always conceded that bursts of funny money injections can and do “stimulate” the economy:

Hayek 1975: The present difficulty is not due to a deficiency of aggregate demand. It is due to the fact that without continued inflation, you cannot maintain the people in the new employments in which they have been drawn by the inflation of the past.

https://mises.org/library/hayek-meet-press

I never see the statists acknowledge this about positions. That’s probably because they refuse to comprehend economic calculation and miscalculation which is the cause of unsustainable prices and capital structures. .

The crypto-Keynesians of all schools have the burden of proof to show that the market left to itself fails and requires an external source of “momentum”. They cannot and will not do this. If the market does not fail, it does not need a shot of “momentum” which will only cause a theft of purchasing power and unsustainable price distortions.

Ask an interventionist: Why the violence? Watch what happens.

http://www.themoneyillusion.com/?p=17692&cpage=1#comment-205619

It seems as though we’re all expected to be cold, strict utilitarians. I never understood the critics of “economic imperialism” until I started thinking about this reality.

I’m looking forward to reading an article recently published in the Journal of Organizational and Institutional Economics entitled “Externalities as a basis for regulation: a philosophical view” by Rutger Claassen.

FWIW:

On the “cold, strict utilitarians” point, Tom Woods spoke to that:

Critics Say, “You Libertarians Are Soulless Materialists”

[www]https://www.youtube.com/watch?v=eZGtcNcyyTI

On the point about externalities, Murray Rothbard covered this:

Man, Economy, and State, with Power and Market

12. The Economics of Violent Intervention in the Market

Appendix B: “Collective Goods” and “External Benefits”: Two Arguments for Government Activity

https://mises.org/library/man-economy-and-state-power-and-market/html/p/1159

Bob I just want to throw this out for you to think about. This goes back to the inflation bet ( you have won 9X).

The stock market now trades at 24X earnings. Just a few years ago 15X was the max sanity.(9X)

GreenSpan can be found on video saying he Knew, they all know, Fed policy of inflation will result higher in higher earnings ratio. Higher and higher.

To them, this is the result, no biggy.

I am telling you though, 24x is where all the inflation has landed.

Just stop an think about what I am saying. Do the math.

Soon it will be 50X, no biggy.

Poor David Stockman and his long puts…

Socialism stinks.

Until rates are allowed to float up and down, we are inflating and moving towards more and more socialism.

In summary, the stock market will grow 2% for ever. They have put this thing on autopilot. Buy and hold S&P index, you cant lose ,lol.

Your inflation is sitting in equity’s, period.

Having just finished reviewing Sumner’s book, I think he would say there has been a dialectical process:

(Classic liberalism Socialism) –> Keynesian, new deal liberalism

(Keynesian, new deal liberalism libertarianism) –> neoliberalism

He’s a neoliberal, not a classical liberal, and one of the things he thinks was learned was the need for aggregate demand management.

So basically he and Samuelson are both Left-Hegelians.

Personally I think that Keynesian style “Aggregate Demand” management is more dangerous than some of the traditional policies associated with Socialism such as wealth transfer for example.

If you take resources from some and transfer to others, there is no trickery or confusion about what has happened. Some are better off, others are worse off. Of course, there are many variations in the techniques used to achieve this, but regardless of those details the outcome is clear. Economists might argue about the morality of wealth transfer; they do argue about how it might benefit or harm a nation as a whole (which is a very tricky thing to define), but none of them argue about how wealth transfer actually operates.

However, certain policies seem able to confuse otherwise highly intelligent people. One of these is the question of whether a minimum wage discourages employment, and another is the idea of “Aggregate Demand” being some sort of entity that can meaningfully be controlled. There’s a kind of internal blindness imposed when people start talking about the evil of savings but the benefits of investment. Apparantly low interest rates can create more investment while simultaneously discouraging “hoarding” … personally I think that’s ridiculous, but lots of people believe it.

BTW, I’m not defending Sumner’s policy profile, just explaining what it is.