Slope of Yield Curve at Record High

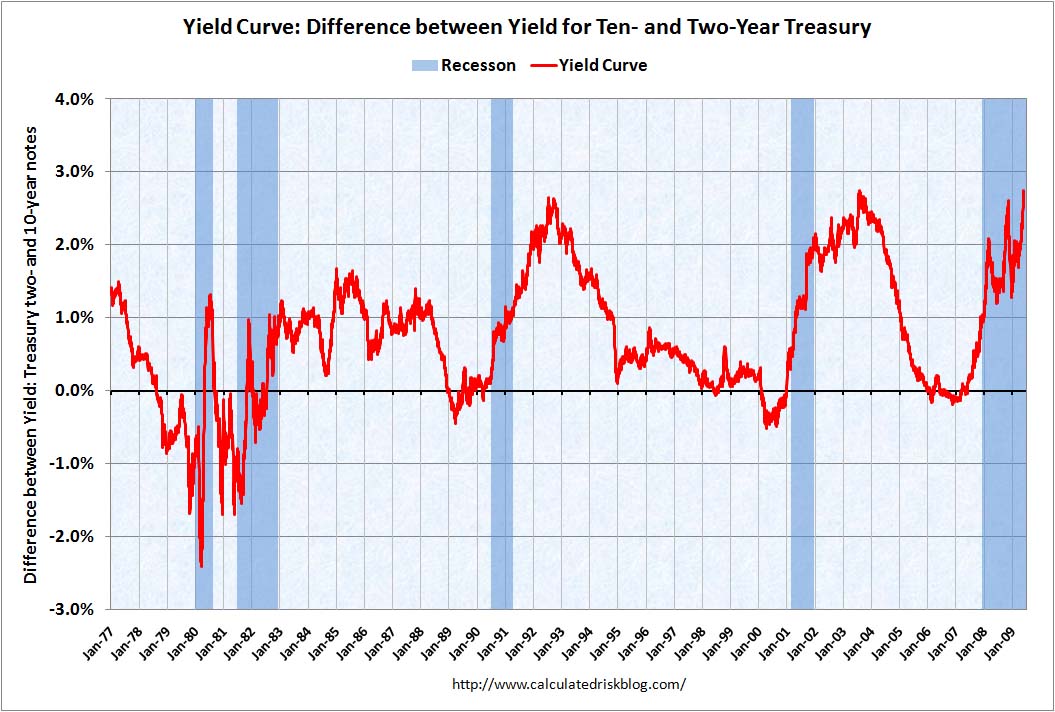

The econogeek blogosphere is abuzz because the slope of the yield curve is at a record high. Here’s the chart from Calculated Risk (HT2 Greg Mankiw):

Whenever I see a chart of a spread, especially when it’s over a long time frame, I like to see its constituents:

The yield curve holds a revered place in the hearts of many, because it is surprisingly good in forecasting recessions (when it “inverts,” meaning when interest rates of shorter maturity rise above interest rates of longer maturity). Notice in the first graph above, that the spread goes negative before each recession. And contrary to an old joke about predicting 8 of the last 3 recessions (or whatever), I’m pretty sure the inverted yield curve is never, or at least rarely, wrong, going back to the 1960s.

When I worked in the financial sector my firm did a research paper on this, and I remember thinking that the academic literature didn’t really have a good explanation for this amazing phenomenon. I think the Austrian theory of the business cycle can explain it: The Fed pushes down short rates by inflating the credit markets, and so you get a few years of a boom. But then the Fed gets scared and hikes short rates back up, and you get a recession.

(And it’s not really that hiking up short rates “causes a recession.” More precisely, when the Fed stumps pumping in funny money, short rates rise and the economy is allowed to cleanse itself of the malinvestments made during the unsustainable boom, a cleansing process that is unfortunately painful and requires workers to change jobs.)

This was actually the topic of Paul Cwik’s dissertation [.pdf]. It’s been years since I read it, and I honestly can’t remember whether I thought he hit it out of the park; he criticized me in a few footnotes and I think I sulked over that instead of his main points.

In our present environment, of course, I think the reason short rates are staying low, while ten-year yields are rising, is that the Fed is still very loose while long-term deficits are making investors worried.