Bernie Jones Interviews Murphy About Bailout

Details and audio link available here. This is actually a pretty neat interview, because he is not a right-wing fundamentalist like a lot of the hosts who interview me, and so I get to break it down for a “normal” person. Another benefit is this guy’s voice is awesome; I wonder if his brother is James Earl.

Fed Uses New Power to Engineer a "Stealth Cut" in Interest Rates

Amongst its weaponry, the government just got fear, surprise, ruthless efficiency, and an almost fanatical devotion to low interest rates–namely, the ability to pay interest on reserves kept at the Fed.

I have been puzzling over this ever since it was announced. It seems innocuous enough; at worst, I thought it just gave the Fed one fewer restraint in pumping in excess “liquidity.” (Without being able to pay interest, if the Fed pumped in too much extra reserves, then the federal funds rate might drop below the target. This is because the banks would have an incentive to lend out any excess reserves and earn something on them, rather than parking them on deposit with the Fed and earn 0%.)

Well, no sooner had the Fed gotten its wish than it engineered a “stealth” (the press’ word, not mine) rate cut. By paying an interest rate on balances kept at the Fed, the central bank can set a floor below which no bank would ever lend out to another bank. But, by setting this floor 75 basis points beneath the current, official target of 2%, the Fed can “cut rates” without actually announcing this to the world. (HT2 Bill Barnett.)

Now, at first this seems like something the Fed could have done all along. I.e., the Fed could have decided its “real” target was 1.25%, and then just pumped in enough extra reserves to cause the market-determined federal funds rate to sink to that level. However, I think the added twist here, is that there is something fairly objective that the banks can see. In other words, the Fed can objectively set the interest rate that it pays on bank balances, and all insiders can see and verify this fact. In contrast, before this new power, if the Fed did a stealth rate cut, the banks would have to just play mind games and try to guess what the true rate was, since all they would have to go on would be the official target rate and then the Fed’s handling of reserves.

The United Socialist States of America

Dear readers, I grant you that my title is partly motivated by the urge for ratings (not that I want you to click on the nearby ads–of course not). But I really think that when future Rothbardians are throwing back drinks and speculate as to precisely when the United States crossed the line, and became not a heavily regulated capitalist country, but instead a very liberal socialist country, they will point to October 2008.

First let’s get our working definitions. Murray Rothbard once asked Ludwig von Mises how to draw that line, since after all in the modern world, there is no such thing as a laissez-faire economy, nor is there pure central planning with no money. (To my knowledge, Lenin gave it the best try ever for a few years and then stopped, realizing absolute power was no fun if all you had were corpses to bark orders at.)

To Rothbard’s surprise, Mises had a crisp answer. He said that if a country has a stock market, where private individuals trade ownership claims to the country’s great engines of industry, then it is a capitalist country. On the contrary, if the State owns the large companies, then that is socialism, end of story.

Now, over the last year the government’s control over the financial sector has steadily increased. People think things got serious by this summer, but the big Wall Street firms were already doomed by, say, Christmas of 2007. By that point, they were all addicted to the massive injections of “liquidity” (oh what a harmless sounding word–they might as well call it soma dollars) being constantly pumped in by the Fed. By Christmas, the banks who were on the Fed’s lifeline were completely at the government’s mercy. Even though they were still nominally owned by private individuals, they could be cut off overnight (or in 28 days if you are a purist) if they didn’t do something the government asked of them.

In early September, the government took the gloves off and literally seized control (again, it is the press using the verb “seize,” which terrifies/fascinates me) of Freddie and Fannie. But hey, even this didn’t seem so crazy, because after all they were government-sponsored enterprises.

But then a mere week went by before the government seized AIG. Now we’re cooking! Not only was this a true blue private company, but it wasn’t even a bank. The justification for its seizure was purely pragmatic. Just as the Bush Administration claims it can imprison anyone on the planet with no legal recourse if one man (whose first name rhymes with gorge) declares the person to be an enemy combatant, so too it showed with AIG that it can seize any (American) company if its collapse threatens the financial system.

And now with the recent bailout… Oh my gosh, I am telling you, this thing is truly awful. It is so much worse than it first seems. The negative economic consequences, like moral hazard, are child’s play.

Let’s get something straight: When the government seizes a company, it is truly a hostile takeover. Here’s a great illustration. Australian money manager John Hempton explains how the Washington Mutual takeover wiped out senior debtholders who would probably have gotten something in normal bankruptcy proceedings. OK folks, are you starting to see? When the government comes in and seizes a company, it is stealing property. (Robert Wenzel has a great post explaining how Citigroup and Wells Fargo are battling to see who gets to eat the carcass of Wachovia, after the FDIC slew it.)

Don’t get me wrong, the government has been picking off vulnerable targets. Neither the FDIC nor any other agency could have declared Exxon insolvent and then given its assets to politically connected firms. (Of course, the route the feds are taking there is to impose a windfall profits tax. Not every problem is a nail requiring a hammer. Some companies you kidnap via the FDIC, and some you merely rob via the IRS. Leave it to the professionals, please.)

What is truly sickening with the Paulson bailout is how many “liberal” commentators are gleeful that the forces of truth and justice prevailed, and got some “protections” for the taxpayer by inserting language giving the Treasury Secretary discretionary (!!) power to acquire equity in companies that s/he assists. (In contrast, the original Paulson Plan merely asked for $700 billion with which to buy assets from the financial sector, rather than buying ownership stakes in the participating companies.) I would be hard-pressed to think of a deadlier weapon to place at the disposal of the Treasury, than to give it the ability to grab equity shares in any company it classifies as “troubled.” With our fractional reserve banking system, and all of the complicated interconnectedness of markets in general, any major financial institution can be plausibly labeled in danger.

This is why the wiping out of so many of Goldman Sachs’ competitors is crucial. The fewer firms there are, the easier it is for the government to lean on any one of them. With the $700 billion pot of goodies at its disposal, the government can easily bribe a a few firms to stop dealing with Target Firm X. Then Target Firm X finds itself unable to roll over its short-term debt, and especially with the short-sale ban and all the other nonsense, no outside private group in its right mind will come in to help. So then Target Firm X has no choice but to ask for government help, with all the attendant strings.

To return to the title of this blog post, I admit that strictly speaking, the government has not yet fully nationalized all of the industries. There is still nominal private ownership of the means of production. But because Americans are very proud of their (imagined) liberties, there will probably never be outright, formal socialism. And yet, I suspect that within, say, 20 years, libertarians will have no hesitation in declaring the United States a socialist country.

And when they trace back the gradual evolution, and try to pinpoint the dividing line, the quantum leap in the march towards socialism, I believe they will settle on October 2008 as the obvious moment.

Great WSJ Article on Effects of Short-Sale Ban

Back on September 29, Arturo Bris had a great piece in the Wall Street Journal on the counterproductive effects of the SEC’s ban on short-selling financial stocks. As readers of this blog know full well, I have been pounding on the fact that the ban will actually make prices more volatile (here’s an example from back in August).

The benefit of Bris’ analysis is that he actually looked at statistical tests and found that volatility went up, etc. after the ban. This is just textbook stuff. Thanks Paulson for proving that freedom works! Maybe you and Bush are really doing all this as a lesson to glorify the Invisible Hand. An excerpt:

What follows is a snapshot of the landscape before the SEC took action, and then the subsequent findings from my study of the 799 stocks initially covered in the ban. First, the “before” trends:

– Short selling activity was not excessively high for the 799 stocks from January to the ban’s start. While the percentage of short sales to total shares outstanding hit 19.1% in March, that percentage fell to 14.8% in July, when the sector’s stock prices experienced the greatest drops since March 2007. From Sept. 1 to Sept. 12, short sales in the 799 stocks amounted to a low 6% of shares outstanding. Short sales in relation to trading volume display the same pattern.

– Short-selling activity typically picked up after a stock fell in price, not generally before. Increases in short selling of individual stocks more often occurred the day after a sharp price drop, not before. This is consistent with research conducted by Karl Diether and Ingrid Werner of Ohio State University, and Kuan-Hui Lee of Rutgers, showing that short sellers trade in response to past negative news, and that they reveal information about forthcoming price drops. They may also want to protect their long positions from further declines by locking in prices through short sales.

…

After the ban took effect last week, we saw a dramatic shift for the worse (market quality and stock liquidity declined) as investors found it increasingly difficult to hedge market risks.– Liquidity dried up. With lenders halting their stock loans, volume down and regulatory uncertainty high, less capital flowed into trading of the 799 stocks. Bid-ask spreads increased more for the 799 stocks than for the market overall.

…

The intra-day trading range has almost doubled for the 799 stocks over the past week. This means that liquidity deteriorated. Less liquidity makes it more difficult for investors to trade without a severe market impact, and prices are less transparent.

…

– Stocks reacted sluggishly to news. The 799 shares reacted more slowly to news than stocks outside the ban’s umbrella — a key sign of market inefficiency. In an efficient market, individual stocks should be affected primarily by company-specific news rather than overall market activity.Taken in full, the preliminary findings run counter to the SEC’s stated rational for imposing the ban.

A Man, a Plan, and a Short-Selling Ban

Yes, I invented the title but no, it is not a palindrome.

As usual, I wrote on a topic for different outlets, stressing different themes depending on the audience. EconLib is for super econ geeks, so I get fairly technical (at least by Internet standards) in this piece on the recent financial coup. For example:

Continuing the above logic, there are other firms that might use shorting as a hedge, rather than as a speculative move. In the extreme, suppose that an analyst is dead certain that Medium Bank XYZ behaved beautifully throughout the housing bubble, that there is not a single “toxic” mortgage-backed security on its balance sheet, and, moreover, that XYZ has been very careful to become intertwined only with other financial institutions that have played it safe. The analyst is convinced that Medium Bank XYZ is one of the safest banks out there.

Even so, it does not follow that the analyst will recommend buying large numbers of shares in XYZ. After all, it is a minor player, and if bad news about a regulatory change or some other event sweeps the market, then XYZ’s stock might go down with the herd. A much safer bet, therefore, would be the spread between XYZ and comparable financial stocks. For example, the analyst might recommend that clients take out a large long position on XYZ, while taking out much smaller short positions on the largest five banks. The SEC’s ban has now made this hedge illegal, and thus our hypothetical analyst may now recommend less aggressive buying of XYZ.

"October 1, 2008: The Coup in America Took Place"

So argues Naomi Wolf (not to be confused with Naomi Klein, author of The Shock Doctrine). Now folks, Robert Wenzel sent me this 27 minute YouTube, and I wrote back, “What part should I listen to? I don’t have time for this whole thing.” And he just said, “The whole thing, man.”

He was right.

You’re busy, I know. Fair enough. Just start running it and then go check your Bloglines, your fantasy football team, whatever. Wolf sounds very credible and what she is saying is very scary. She ties together a bunch of things that I have been harping on here at Free Advice, but she connects them in a way that I hadn’t done. By about the 15:00 mark, I think you will agree with her that a coup has taken place.

Incidentally, below is the clip she alludes to, where Brad Sherman (the same guy I gave a wise aleck answer to when I testified before the Financial Services Committee) says that representatives in Congress were told the president would impose martial law if they didn’t vote for the bailout.

Despite "Rescue," Markets Continue to Get Pummelled

I really don’t take pleasure in pointing this out, not the least reason being that I have a (very modest) retirement account in global equities. But we were told we needed to fork over $700 billion to reduce volatility and shore up confidence in the financial system. Well, as of this writing, the Dow is below 10,000, and the S&P is down 4.75% on the day.

Is it too late to have a Do Over?

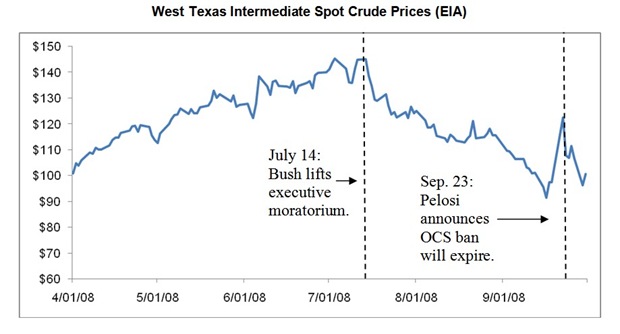

Lifting the Offshore Ban [Apparently] Gave Immediate Price Relief

Here’s a link to a fairly impressive demonstration that might surprise those who thought the offshore ban had nothing to do with current prices. The money chart:

NOTE: In the interests of complete academic honesty, I should note that after I wrote the above article, someone asked me if the price for natural gas looked the same. (After all, offshore drilling will tap into natural gas deposits as well.) The 2nd inflection point is beautiful, but for the first one, the natural gas price peaks more than a week before Bush lifts the executive ban.

Recent Comments