Responding to Steve Landsburg on Government Debt

Steve graciously commented on my recent talk from Mises U, in which I rehashed the Great Debt Debate of 2012. (Steve left a comment here and here.) Below, I will respond to Steve’s points individually. But before doing that, let me give an analogy.

==================

A HYPOTHETICAL DEBATE ON GUNS

PAUL: It’s impossible for handguns to hurt our grandkids, so long as they are wearing bulletproof vests.

BOB: What the heck are you talking about? I could shoot the grandkid in the head. Dead.

STEVE: Well no, actually it would be the bullet that would cause the actual pain there; the handgun is incidental. Indeed, I could kill someone with a rifle or indeed any device that accelerated a bullet. Furthermore, a handgun without bullets can’t hurt our grandkids. So Bob, you are actually wrong on this, and Paul is right.

==================

AN ACTUAL DEBATE ON GOVERNMENT DEBT

PAUL: It’s impossible for debt to hurt our grandkids, so long as they hold the Treasuries.

BOB: What the heck are you talking about? We could have overlapping generations like this. Utility up for earlier generations and down for later ones.

STEVE: Well no, actually it would be the taxes that would cause the actual pain there; the debt is incidental. Indeed, I could cause utility movements with simple transfer payments. If the government ran up big debts today but never taxed anybody to pay the interest or principal, clearly our grandkids would not be harmed in the way you think. So Bob, you are actually wrong on this, and Paul is right.

=================

Now on to Steve’s specifics, with his words in italics and mine in normal text:

Your chart and your presentation are very clear and engaging (as one expects from Bob Murphy). Also, a big thumbs-up on the beard.

I always liked Steve.

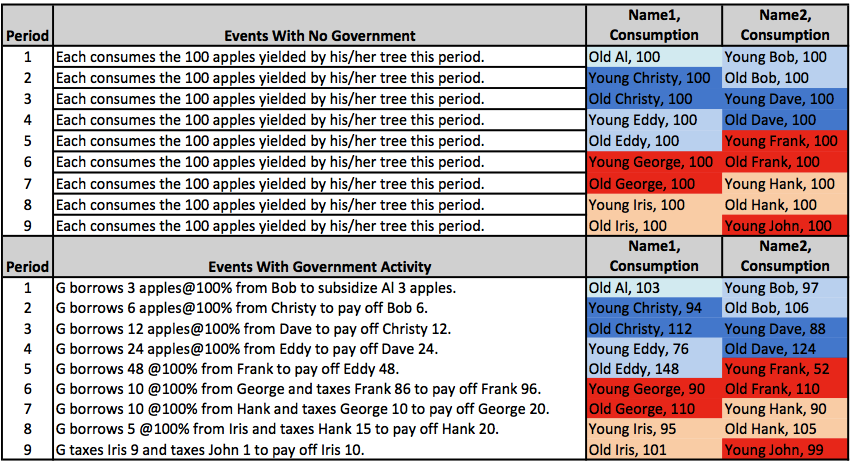

1) Your chart does not display the effect of govt borrowing; it displays the effect of a Social Security system (with old people receiving transfers of various amounts in various generations). If you financed exactly the same system through taxation, you’d get exactly the same results. In year 1, we tax Young Bob 3 apples and give them to Old Al. In year 2, we tax Young Christy 6 apples and give them to Old Bob. Et cetera.

All of the effects you’re illustrating would have been exactly the same if you’d financed all the transfers by taxation instead of borrowing. It’s the transfers that are having all the real effects.

Your particular assumptions lead to different sized transfers in different years. But any pattern of transfers you care to specify can be achieved equally well by appropriate timed borrowing or similarly timed taxation.

See my analogy above.

There is no doubt that Krugman thought it was our grandkids owning the bonds that made all the difference. This is why I was so frustrated with Steve at the time of the debate. Steve was making a series of correct statements showing how government financing was a red herring, but in that framework, “we owe it to ourselves” is still a non sequitur. And yet that was literally the mantra of Abba Lerner, and it was explicitly adopted by Krugman and Dean Baker.

That’s all Nick Rowe and I were doing with our simplistic thought experiments. We were trying to show as simply as possible that Lerner and Krugman were simply mistaken when they argued that “we owe it to ourselves” therefore meant government debt (and yes the taxation to service it) couldn’t hurt our grandkids to our benefit.

I myself believed this at first. Then I realized Nick was right. (Don Boudreaux was right too, but it was Nick’s specific numerical examples that made me realize I was wrong.) Dean Baker himself later admitted that theoretically his original position was wrong, and switched to an empirical defense. To my knowledge, Krugman never realized the problem.

2) You’ve assumed a 100% interest rate. This means that in each year, people adjust their bond purchases until, at the margin, they consider two apples in old age a perfect substitute for one apple in their youth.

Therefore:

Al is a winner.

Bob is neither a winner nor a loser. (He gains 6 “old age” apples, which exactly compensates him for his loss of 3 “youth” apples.)

Christy is neither a winner nor a loser.

Dave is neither a winner nor a loser.

Eddy is neither a winner nor a loser.

Frank, George, and the rest are losers — because they get taxed. The bottom line is that you hurt people by taxing them. Again, this would be true with or without the borrowing program.

I didn’t go back to check this, but I *think* you said Bob, Christy, Dave and Eddy were winners. If so, I think that’s a mistake.

No, in the very simple example I sketched out, there is no private borrowing. I specified actual utility functions and so the Excel sheet told me who had more or less utility, relative to the consume-your-endowment baseline.

In a more general framework, yes we have to allow for private credit markets, but even there the government can improve the utility to lenders by offering a higher interest rate (relative to default risk) than the market. I will do more work on this once I see how far things have been taken in the literature.

(Steve anticipates a bunch of these subtleties in the following, but I don’t see how it overturns my position:)

3) Your simplifying assumptions mask the most interesting (to me) issues. Namely: Because the govt is essentially doing people’s saving for them, they face a reduced incentive to save on their own. This isn’t an issue in your model because they can’t save without the govt anyway. But in the real world, this means people will engage in less private saving, so there will be less investment (and in fact suboptimal investment) which hurts

all generations going forward above and beyond what your chart shows.

(This is the essence of Martin Feldstein’s calculations of the social cost

of Social Security.) But once again, this effect will be exactly the

same whether you finance your program through taxes or through borrowing.I should add, though it’s a second-order effect, that some borrowing is inframarginal, so the govt, by making borrowing possible, can make some people better off. For example, we know that the last apple Bob borrows is, for him, a perfect substitute for 1/2 a present apple (otherwise he’d borrow more). But his first and second borrowed apples might be worth more to him than 1/2 a present apple apiece. So Bob can be a winner here, though I think this is a relatively minor point in the context of the issues you’re trying to get at. (Or maybe it’s a major point, if I haven’t fully understood your purpose.)

{kind=link}

Keeps saying it is a duplicate – adding this to avoid that

‘We were trying to show as simply as possible that Lerner and Krugman were simply mistaken when they argued that “we owe it to ourselves” therefore meant government debt (and yes the taxation to service it) couldn’t hurt our grandkids to our benefit.’

So I think the thing that does the burdening is the ‘the taxation to service it’ , right ? And Steve’s point I take to be that if the govt just taxed this generation the same amount but used it for something else other than paying off the debt (that also didn’t benefit them) they would be just as equally burdened.

Is that a correct understanding?

In both cases (tax to pay off debt v tax for some other purpose) it is the tax that is the ‘bullet’

But in the case of taxes used to payoff debt the obligation was created by a past generation’s government , while in the case of taxes used for some other random purpose the burden was created by a discretionary act of the present government.

So I think I would call it for Bob that debt does create a burden for future generations in as much as the debt is binding and must be paid when due.

Technically though I think Steve is right. Any present government could use a combination of taxes on bond holders and defaults on bond payments to stop any present generation from actually being burdened.

1) You are absolutely right that “We owe it to ourselves” is a red herring. Holding govt spending fixed (as I think we’ve agreed to do here), the decision to issue debt *is* a decision to lower current taxes, which in turn means that people can leave larger inheritances. It doesn’t matter whether those inheritances are in the form of govt bonds or in some other form, hence it doesn’t matter whether the bonds were bought by domestic citizens or by foreigners.

2) It is not the taxes that cause the pain any more than it is the debt that causes the pain. It is the govt spending that causes the pain.

3) The problem with your analogy is this: It is standard and reasonable in discussions like this to hold the level of govt spending fixed. The corresponding assumption in your analogy would be to hold the number of bullets piercing your body as fixed, as we vary the use of handguns. It is absolutely correct that if we hold that number of bullets fixed, then a change in the number of handguns (or a switch from handguns to rifles) can’t hurt you. But it is also absolutely crazy, in this context, to have a discussion that holds fixed the number of bullets.

4) I think you must have somehow misunderstood me in your response to point 2. I never said or assumed anything about private borrowing. What I said was that your model has specific people buying specific quantities of govt bonds, and from those decisions we can infer something about their utility functions. This inference tells me that the marginal apple that anyone lends to the govt makes him/her neither better nor worse off, and since all of the apples are at least nearly marginal (when you are lending 3 out of an endowment of 100), the opportunity to lend to the govt cannot be making anybody very much better off. (Yes, you could specify a weird utility function where the MVs of the 99th and 100th apples are vastly different, and then I’d be wrong.)

(This line added because your software keeps claiming this is a duplicate post; maybe the extra line will fool it.)

‘It is not the taxes that cause the pain any more than it is the debt that causes the pain. It is the govt spending that causes the pain.’

I’m not following this. If I am taxed and the money is spent on something I wouldn’t have bought myself then this is a ‘pain’ to me. However if I don’t pay taxes and government spending buys something that benefits me then this is not a ‘pain’.

I think it would even be impossible to say if the pain of those taxed exceeds the benefits of those who get the spending.

‘But it is also absolutely crazy, in this context, to have a discussion that holds fixed the number of bullets.’

Is bullets = taxes in Bob’s analogy?

If so then even holding govt spending fixed (3 apples in Bob’s model), taxes (bullets) do increase to pay the interest on the debt. don’t they.

Holy cow! Steve I actually think we are now disagreeing about the underlying economic analysis, whereas in the original debate I agreed with everything you were saying except your unwillingness to say, “Good job Bob, you showed Krugman was messing everybody up on this.”

Let me just focus on that point for now, Steve, because your other points are more substantive.

You agree, now, that “we owe it to ourselves” is a complete red herring, right?

Now then, that was THE ENTIRE POINT of Dean Baker and Paul Krugman when they started this debate. It was literally in the title of Krugman’s initial volley, so you can’t say I’m exaggerating. They couldn’t believe any idiot could possibly believe that gov’t debt could burden our grandkids SO LONG AS THE TREASURIES WERE OWNED BY OUR GRANDKIDS, but Baker and Krugman *did* say that to the extent that the Treasuries were owned by future Asians (for example), then indeed today’s debt mongers had a point.

So I take it, Steve, you are now agreeing with me that this point was utterly wrong.

And yet, back when you jumped into the debate, the very first thing you said was: “Paul Krugman has a very good column on government debt and why it doesn’t matter nearly as much as many people believe. There’s just one spot in the column where I think Krugman misses the point, and therefore makes a weaker case than he could have made.”

Again, in my gun analogy, that would be like saying, “Krugman has a very good argument when he says handguns can’t hurt our grandchildren, I just have one little quibble where he says it’s because he thinks empirically most of our grandkids will be wearing bulletproof jackets…”

(Yes, in your post you weren’t linking to Krugman’s blog post, but rather to his column, but even there, the column fundamentally rests on the “we owe it to ourselves” fallacy. That is the basis of the column; the rest is window-dressing.)

Steve, let me make sure I understand you. Are you saying in an overlapping generations framework, if we fix the timing of government spending (which includes transfer payments as well as interest/principal on outstanding government debt) then the timing of taxation can’t affect the utility of specific individuals?

If so, are you saying this is due to pure accounting, or are you saying it also requires Ricardian equivalence-type assumptions about how people will change their bequests?

Because notice, Baker and Krugman weren’t talking about Ricardian equivalence stuff. They were saying as a matter of physics, that old people today can’t benefit from GDP in the year 2100 because of time.

1) I have also believed that “We owe it to ourselves” is a complete red herring, and have said so many many times in print over the past few decades. I haven’t reviewed our past discussions on this matter, so I don’t know whether I said something that you might have interpreted as agreement with Krugman on this, but I am 100% sure my position on this has never changed.

2) To repeat: If the govt borrows from me today, then my daughter inherits both the debt and the bond. If the govt borrows from an Asian today, then my daughter inherits both the debt and the extra money I’ve got in the bank because I didn’t get taxed, EITHER WAY, she comes out even. To the best of my memory, Krugman had the first part of this right and the second part wrong, he spent most of the column on the first part, and therefore I thought it was a pretty good column. I have not gone back and reread to make sure my memory is correct, though.

3) The big exception: It is nonetheless perfectly *possible* for govt borrowing (either from me or from Asians) to transfer utility across generations. It does so if it affects either my consumption or leisure choices, which affect the size of her inheritance. This is true with or without overlapping generations.

4) However: That big exception does not apply in your model, since there is no leisure and people always consume their entire incomes. Therefore, in your model, the govt borrowing is having absolutely no effects beyond those that could be achieved by an equivalent pattern of taxes and transfers. Those taxes and transfers, can, of course, affect individual utility.

5) Summary: Govt borrowing has exactly the same effects as taxes and transfers, unless the borrowing affects consumption or leisure choices in ways that taxes and transfers can’t. That exception applies in some reasonable models, but it does not apply in yours.

[“If the govt borrows from me today, then my daughter inherits both the debt and the bond. If the govt borrows from an Asian today, then my daughter inherits both the debt and the extra money I’ve got in the bank because I didn’t get taxed, EITHER WAY, she comes out even.”]

Are these scenarios consistent with the overlapping generations assumption?

Steve, I hope you can answer my main point in this discussion.

Yes you can do the same thing with taxes and transfers THEORETICALLY, BUT in the real world a politician proposing the same spending scheeme with direct taxes won’t be elected and this spending doesn’t ever happen in the first place, because people taxed could not be sure to get their money back because noone is bound to.

Only if a politician proposes the same thing via Bonds, that give people of today a piece of paper that guarantees them they personally do not loose any money, can this thing be started at all.

And that is because young Bob doesn’t want to be taxed to make old Pauls life better. Only if he knows future gens are obliged to pay him off when he is old and the burden is for sure transfered to young XY will he agree.

Skylien:

I live in the United States of America, where my government taxes me in order to make transfer payments to older people. This is called the Social Security System. I don’t like paying those taxes, but I am partially placated by the expectation that I might receive similar payments myself when I am older, though there is absolutely no legal guarantee of that. I hold no bonds, and if the Social Security system is eventually eliminated or curtailed, I might say, informally, that the government has “defaulted” on a promise, but in fact there was never a legally binding promise in the first place.

In fact, I fully expect that some generation — maybe mine, maybe a later one — will in fact receive less than it pays in.

I am also taxed to fund a whole lot of *other* transfer payments which I have *no* realistic expectation of ever recouping through similar payments from others to me.

So if your theory is that people simply will not tolerate being taxed to fund transfers, then your theory flies in the face of empirical reality.

If you eliminate all government bonds, and all government debt, from Bob’s overlapping generations model,, you can duplicate exactly the resource transfers via the tax system. And it seems to me that people are exactly as likely to stand for it. After all, under Social Security, I risk a change in the program. If instead I am issued bonds, I risk a default. (And the more bonds the govt issues, the greater that risk is.) Eventually, there are a fixed number of resources to go around, so the risk of getting a raw deal under social security has to be pretty much the same as the risk of getting a raw deal when I buy bonds.

That, I think, is the reply you were asking for. Though it’s slightly off-topic, I will reiterate this: Govt debt *can* have real effects, if and only if it changes the quantity of physical resources that one generation leaves behind for the next. It can do that if it changes the incentives to work (so that we produce more or fewer resources) or the incentives to consume (so that we leave more or fewer resources behind). In Bob’s model, none of that can happen, because his model holds fixed the quantity of physical resources at 200 per generation. In a more realistic model, debt has consequences, but the reasons for those consequences are 100% absent from Bob’s story.

In Bob’s model when the government borrows apples in period 1 it creates a 100% certainty of either future taxation or a future default that will cause utility loss to someone in a later period.

Govt debt has “harmed” future generations.

If the government simulated everything in Bob’s model via taxation then it could replicate the utility outcomes – but all the harm is done to people in the current period never a future period. Taxation is not harming future generations.

If you change Bob’s utility function and/or allow government borrowing to affect output in the present or the future then you could make government borrowing have any effect you wanted it to have on future generations just by tweaking your assumptions.

Thanks very much for the answer.

But why does the government then go this way to give people pieces of paper that tell them they will get the money + some more returned when the bond is due or they are old enough to get SS?

If you theory were true and it would not make any difference of how people would react. Why do we have those promises and bonds in the first place? In effect you are saying that politicians can do what ever they want and people would go along with it anyway.

I live in Austria, and since 2014 we can no go online to see our current status of our claim on pension payments when we are old. Pension payments are a hot topic in Austrian politics basically all the time. It wouldn’t if people would just stoically accepted whatever politicians wanted to do..

The proof is in the pudding. We have bonds, and promises of SS “insurance” for a reason. People need to be convinced. Direct taxes with no promise of repayment (with different degrees of legal obligations) would not be accapted for many things the government wants to fund. It could simply not “tax” and spend as much as it can without those tools.

I agree with you last part.

“It could simply not “tax” and spend as much as it can *with* those tools.”

sorry..

“I live in Austria, and since 2014 we can *now* go…”

omg, I shouldn’t write an answer on a sunday morning.. Sorry for all the mistakes, at least the remaining ones should not interfere with the intended meaining of my answer.

>So if your theory is that people simply will not tolerate being taxed to fund transfers, then your theory flies in the face of empirical reality.

The relevant comparison is to *how much more* tax and spending they could get political support for, if they *couldn’t* just pass off the problem to a future generation via debt. And on that question, yes, a higher spending level is indeed facilitated by (the capability of) issuing bonds.

>If you eliminate all government bonds, and all government debt, from Bob’s overlapping generations model,, you can duplicate exactly the resource transfers via the tax system.

Logically possible, yes. Politically possible, no. Though (as above) you could get some (lower) level of transfer payments funded.

> The problem with your analogy is this: It is standard and reasonable in discussions like this to hold the level of govt spending fixed

it is not. The *entire reason* that Joe Sixpack raises concerns about debt is *because* of the spending it thereby facilitates, — the concern being that the government *shouldn’t* be spending the money that it needs the debt for, as that hurts our kids.

At best, your point translates into, “hey Joe, you should more explicitly frame the argument about the spending itself, and since the borrowing aspect cancels out. You’re also implicitly making an argument about the relative social returns of the government spending vs the conception you’d enjoy without the taxes or the spending.”

Joe’s *substantive* concern is valid — the borrow+spend action leaves his kids worse off. No amount of “lol just buy government debt” addresses that.

Steve would agree I think. The point under dispute is, does debt financing vs tax financing have deleterious effects? If you want to make the distinct point that debt financing is an easier sell politically, so more of a worry, I would agree. But that’s not the bone of contention this time.

He pretty clearly disagrees about whether “lol just buy government debt” is responsive.

Steve is trying to have it both ways. The whole point of this discussion is that certain financing schemes create the opportunity for earlier generations to benefit at the expense of later generations. In a democracy, this creates huge moral hazard because the people making decisions need not pay any price for the decisions they make. It’s about choices, and how the scheme alters people’s decision making process.

* Government will spend more if they recognize that debt financing will not require them to put the hard word on taxpayers. Most governments think short term (4 years till next election) so they don’t care about any problems that might be a generation away.

* Citizens will choose to buy the government bonds if they feel this is a secure purchase with guaranteed interest payments. Each individual is expecting some other person to pay the tax… on the margin this is correct thinking because the tax imposition is dilute while the interest payments are right here in my hand (until the payments stop coming, but that’s another story).

Steve is trying to argue that these are really arbitrary transfers of funds and in principle any fund transfer would be possible… but that would be ignoring the economic and political process.

Exactly this! Thank you!

So you say Landsburg doesn’t get that the problem is the spending. In proof you link a column where Landsburg says the problem is the spending.

That’s blurring the very distinction that I and his critics are making: debt allows them to defer the taxation to another generation and is thus more politically popular. But they wouldn’t be so willing to levy a tax if they themselves had to pay it. That’s exactly why it’s important to fight such debt issuance!

Re 2. The government makes a decision to allocate resources in a way the market would not. This has two sides, the spending and the paying for. The paying for can be effected by a transfer method known as taxes or a transfer method known as borrowing. In either case we have an reallocation of resources which is less productive of utility that it would have been without this reallocation. But it is the reallocation in toto not just the spending side of the coin which is the problem.

Note that I am agreeing with Steve here.

I don’t think that’s quite right and you too seem to be talking past each other. Yes, the type of spending “matters” in terms of the amount of assets that may or may not be bequeathed to future generations, but the liabilities bequeathed are strictly a function of whether current taxes or borrowing are used for that spending.

First, a quick statement of the problem and an example. The problem arises when the assets are sold down overlapping generations (buying and selling bonds) while the liability (promise to pay) is bequeathed, i.e. inherited. This is the fundamental asymmetry that causes all the problems in Bob’s model, and in our overall government borrowing situation. With current taxation, no such problem exists.

The example is as follows: imagine an indolent, drunken father who borrows from his son (even formally signing a note to pay), who then gets drunk with the money for years and then dies. The son inherits the note, but is without any compensating benefits, either inherited wealth, or the ability to recover the debt (he now “owes it to himself”). This is where the moral outrage of “stealing from our grandchildren” comes from, and it is legitimate as far as it goes.

However, you are spot-on in a different sense to focus on the nature of the spending. If the father in the above example had instead invested in generating productive assets (building a house, or a company) and had bequeathed those as well, then the son would actually be better off overall. So the type of spending matters in this very important sense, but so too does the method of financing.

To sum that last point up, with spending from current taxation, there is no method for imposing a burden on future generations, no matter the nature of the spending (either the future generation inherits assets and no liabilities, or no assets and no liabilities). With spending from government borrowing, the future generation’s status is indeterminate depending on the quality of the spending, that is whether valuable assets were in fact created to be bequeathed along with the liabilities, or whether only liabilities were inherited.

Yes, the primary debate should always be on whether government spending will generate better assets for future generations to inherit, or whether private economic activity will do the trick better. But there is still a real secondary debate on whether that government spending should be financed currently through taxes, or from future generations through Treasury borrowing. It seems to me, therefore, that you are both raising salient points, but not quite getting each other’s emphasis, Steve on the former and Bob on the latter.

Is it this that Mises talks about on page 843 of Human Action?

Steve say ‘Summary: Govt borrowing has exactly the same effects as taxes and transfers’.

Isn’t the issue not whether they have the same affect but when they have those effects ?

In Bob’s model it is indeed always taxes that cause utility loss. but its ts the fact that borrowing in one period creates a tax obligation in a later period that leads him to conclude that borrowing can be a burden to a later generation in an OLG model.

Dr. Murphy, Here is my story.

Imagine a simple world in 1914 where the “Good News of the Kingdom” has come to pass and the “Other Sheep (John 10:16)” live in an Anarcho-capitalistic society of peace, plenty, and prosperity. One of the apostles (not Judas or Paul, one of the other ones) comes to talk to me and says, “Bitter, we have a minor problem. Some people suffer from anxiety (lack of faith) and when they have an attack they pull all their money from their bank and others see them do it and it starts a “run”. What we are going to do is create a new currency called ‘Bitter Clingers’ and when we have a “run” will give it to the bank to cover the money the depositors withdraw. This is going to be good money because we are going to print the faces of the apostles on it.”

I point out that we cannot give money to the banks for free that are having the “run”; that we must charge at least the rate of interest the banks are paying their depositors. The Apostle agrees. I purposely don’t mention the idea that these “runs” may not be caused by anxiety but by the observation that the particular bank is badly managed and insolvent. I do point out another opportunity.

“Since there is a belief here in Paradise (Luke 23:43) that prices are set by the size of the basket of money chasing the basket of goods and services available, I think we should also grow the money supply by the amount the economy grows so that prices remain stable.”

The Apostle is interested. I say that we cannot give that money out for free either so we will charge interest on it. The Apostle then thinks for a minute and says but what about this interest? I assure him that any interest I collect, less my expenses of course, I would give to him for his good works. (Gal 2:1-10) He then pointed out that if you create money to lend, in a sense creating a “flexible currency”, then the amount the flock deposits will no longer be equal to the amount of money the sheeple at the bank lends out. People will owe more than what other people will be saving. I smile and assure him that not only will no one notice, any who do notice will believe that it is “God’s Will”.

Let’s say there are $100 of currencies, greenbacks and silver certificates among others, in circulation 1914. I grow the money supply by 5% ($5) by setting my interests rates competitive to what depositors want and let us say that is 10% interest (to keep the math easy). At the end of year one there is $105 in circulation but the sheeple (member banks) now owe me $5.50. Prices stay stable so the second year I again grow the money supply by 5% ($5.25) and charge the same interest which brings the money supply up to $110.25. Now at the end of year two the sheeple owe me principal and interest of $11.825. The question is; how many years does it take before the sheeple (and the people they lend money) owe me more money than money in existence? How much money is owed in year 104 vs. the amount in circulation? The Apostle Paul, of course, yells and screams for audits and accounting….oh no, that is another Paul I am thinking about, sorry.

My two questions. First based upon the scenario above, who should “own” the debt? Should the apostles and their 144,000 ruling from heaven or should the “Other Flock” living on the Paradise Earth? How about a 50 word justification for your answer. Second Dr. Murphy you asked me to remind you when you weren’t so busy to figure out who we owe the $150 TRILLION debt to and why it is not an asset. See: https://en.wikipedia.org/wiki/Financial_position_of_the_United_States#Foreign_debt.2C_assets.2C_and_liabilities

“The financial position of the United States includes assets of at least $269.6 trillion (1576% of GDP) and debts of $145.8 trillion (852% of GDP) to produce a net worth of at least $123.8 trillion (723% of GDP)[a] as of Q1 2014.” This is the reminder.

The answer would be to lend freely, at a penalty rate, against good collateral.

Ahhh but now you are lending money even when there is no “run” which rather defeats your original concept that this was all about anxiety (lack of faith).