So Was Oil in a Speculative Bubble or Not?!

Over the last year, I pretty definitively painted myself into a corner regarding speculators and oil prices. I said in many places (here and here, for example) that speculators weren’t driving the record run-up in oil prices, and that the default explanation–changes in the fundamentals of supply and demand–were responsible. Specifically, I testified to the committee of my good friend Barney Frank (though he actually was never in the room when I was speaking) that record oil prices were the result of a weak dollar and explosive growth in demand in places like China and India.

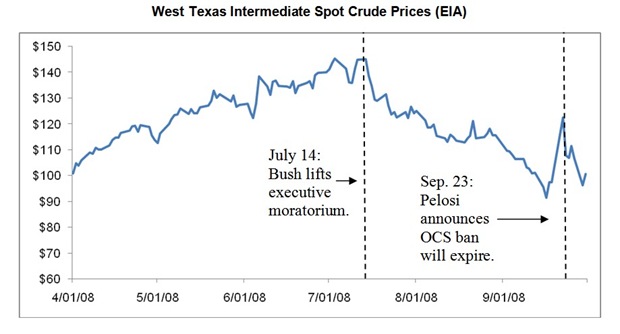

Well, here’s a chart of oil prices:

I think we can all agree, that looks pretty bubblicious.

So what gives? Well, the thing is, I still don’t see any obvious mistakes in the chain of reasoning I used in the two articles linked above. And for the record, I didn’t come to the analysis thinking, “OK, for political reasons it can’t be the fault of hedge funds, so I have to work some Murphy Magic here and spin a story.”

On the contrary, I initially thought it was speculators in the futures market driving up oil prices, especially since the take-off in commodities really kicked in when the Fed started cutting rates in September 07. (For example, the yr/yr change in monthly oil prices was actually negative until then, but afterward of course oil prices started exploding.) So I was coming to the analysis thinking speculators were holding prices up above the equilibrium price as determined by the “short-run fundamentals” (if you will), and I was prepared to explain why that was a good thing. E.g. if the US started bombing Iran, then at that point a build-up in oil inventories would be a blessing.

So I was very surprised when the initial tests weren’t showing any tell-tale signs of a speculative bubble. If you want to talk about ideological bias, you could say that it was apparent since I was prepared to argue “trust the market” whether or not speculators were pushing up the price of oil. But my views on whether the speculators were responsible weren’t driven by a preordained conclusion.

But back to the question at hand: Reader Joe Potts emailed me and asked if the apparent bursting of the oil bubble has made me revisit my arguments about speculators. I would definitely need to study the matter more carefully before giving a definitive answer, but here are my quick reactions:

(1) The big swing in prices certainly looks like it has nothing to do with fundamentals, but keep in mind (a) the dollar fell sharply and then rebounded very sharply from September 07 – October 08; the graph of oil prices measured in euros or pounds wouldn’t look nearly as bubblicious, (b) the prospects for future economic growth have completely collapsed during the period in question, and (c) the US removed the moratoria on billions of barrels of domestic reserves (see the surprising graph below). So when smart alecks say, “Oh, you told us it was supply and demand. Did those curves for oil really shift that much in 4 months?!” the answer is, “Maybe.” When you throw in the fact that oil is famously price inelastic, then it is just possible that much of the apparent bubble is really due to changes in the fundamentals.

(2) Even if it were true that hedge funds and other institutional investors were pushing up oil prices during 2007 and the first half of 2008, nonetheless 95% of the people who “called” it were still spouting nonsense. In particular, they were acting as if the hedge funds could push the price up automatically and make guaranteed money–that’s why the CFTC needed to step in and lay down the law to protect hapless motorists. The sudden collapse in oil prices shows that their worldview was rather flimsy.

(3) I would need to first run some back-of-the-envelope calculations to see how much wiggle room the factors I discussed in point (1) give me. If it still looks like I need to do some serious ‘splainin, it occurs to me that there is a theoretical possibility that the typical “It’s those greedy speculators!!” people would have missed, but also that I would have missed with my (somewhat) methodical process of elimination. What if the demand by end users (such as refiners) is fairly malleable, based on expectations of future prices? Something like, the refiners will buy 5 million bbl/day when the price is $90 per barrel, and they expect prices to remain at $90+ for at least the next 12 months. But if they consider $90 to be a ridiculously unsustainable price, then they only buy 4.5 mbd at that price.

I haven’t worked this through yet, but it’s something that neither side really considered. The people blaming “speculators” had in mind hedge funds or, for the more sophisticated analysts, they blamed the oil producers who cut production and “stockpiled” oil underground. But as I explained in the articles linked in the beginning of this post, the data just don’t support either of those claims.

However, what if the “speculation” was being done by the actual end users? That would be indistinguishable (with the approach I was using) from saying, “Nah, physical oil demand is way up. There are no inventories accumulating.” And yet, this case was clearly not what I had in mind when talking about the “fundamentals.” (We are already getting into this gray area if we say that the lifting of the executive and then congressional bans on offshore drilling moved prices. Because obviously, if those policy changes have an immediate impact, it must be working through expectations. All along–even before it happened, mind you!–I expected the effect would come from producers increasing output, since they expected more competition from the US in ten years or whatever. But maybe that same mechanism was at play on the “fundamental” demand side too.)

In conclusion, I am not yet throwing in the towel and saying, “Yep, it was a speculative bubble.” But if I do end up deciding that, I think it would be along the lines of point (3), since the logic in the earlier articles still seems solid to me.

Who Were the Worst Economists During the Housing Boom?

John Carney is starting a list of economists who botched the housing/financial crisis, and his first victim is Cato’s Alan Reynolds. I feel bad for Reynolds, because when you read the “shocking” quotes that Carney reproduces, I totally understand why a free market guy would say those things at the time. (Incidentally, this is why libertarian economists almost have no choice* but to embrace Austrian business cycle theory: If you don’t think the Fed caused an unsustainable boom, then it really is inexplicable why everything blew up like it did. It’s not like the government raised taxes or imposed price controls in early 2007.) I just hope nobody points Carney to the second-last paragraph of this piece. *whistling*

It’s not great, but the below video has some embarrassing predictions by Bush Administration people, as well as Dubya himself. “Diablo” at Carney’s blog posted the link.

* Incidentally, I recognize that a critic of unregulated markets would find my statement to be hilarious, and serve as proof that free market economists are ideologues. So, for the record, I will admit that economists who were completely stunned by how bad the credit markets screwed up, should first consider the possibility that decentralized markets don’t work very well. If you still think there is way too much evidence against that position, then you need to find some other way to explain what happened, and I submit the best explanation is the Fed.

Thinking Green: It’s All About Tradeoffs

This Wall Street Journal article (HT2 Rob Bradley) explains that some of the money you save in fuel from switching to a high-mpg vehicle is offset by higher insurance premiums:

Small cars generally cost more to insure than larger ones because they’re involved in more accidents and incur bigger claims, especially for injuries. That’s true regardless of the driver profile, though younger and less-experienced drivers tend to buy smaller, cheaper cars.

A 40-year-old male driver would pay an average of $1,704 to insure a 2009 Mini Cooper that gets 37 miles per gallon on the highway, according to a study by Insure.com, an online insurance broker. That same driver would pay only $1,266 — a difference of $438 — to insure a Toyota Sienna Minivan, which gets 23 mpg.

Similarly, a Honda Civic compact that gets 36 mpg on the highway costs $412 more a year to insure than a Honda CR-V, a small sport-utility vehicle that gets 27 mpg.

Three Thoughts on the Bailout Switcheroo and Bogus Credit Crunch

(1) Isn’t this hilarious that the $700 billion “Troubled Asset Relief Program” contains all sorts of money for various companies–here’s a partial list–but not one thin dime for troubled asset relief?

(2) So how do all those fools who were running around saying how much money the taxpayers were going to make on these purchases of mortgage-backed securities feel now? I admit, in this article I just cautioned that the government would fleece the taxpayers on both ends of the deal, by buying the “toxic” assets at overvalued prices, and then dumping them down the road at below-market prices to their cronies. It didn’t occur to me that Paulson might blow through the whole $700 billion on other Super Important Things before getting around to spending a cent on what (he told us) was necessary to avert a worldwide financial collapse.

(3) In late summer I formally incorporated my consulting business. As part of the process, I opened up a business checking account, and just for kicks–since Tyler Cowen and Alex Tabarrok were arguing about it at MR–I applied for a business credit card. Keep in mind, I am a relatively new business owner; I didn’t show any history of revenues to the bank. All they could do was run my credit history; I only had a half year of consulting income on my last tax filing (if they even checked that). Nonetheless, they approved me for a $7500 credit line (with purchase APR right now of 12.99%) and I had the card in about two weeks from the time of application. I asked the lady at the bank (when I was applying) if she anticipated any problems, what with the “credit crunch.” And she said something like, “Well we’re a smaller bank, you know, and we didn’t get into all that stuff that the bigger banks did. We’re being a little more cautious in our review process because of all that’s happening, but no, if there’s a ‘crunch’ we certainly haven’t felt it.”

Paulson on His Bailout: The Ol’ Switcheroo

So you know how it was a little weird that Paulson initially asked for $700 billion to buy dubious mortgage-backed securities and other assets, and then very quickly changed course and said they needed to use some of the money to “recapitalize” troubled banks? And then remember that the first $125 billion got injected into the biggest 9 banks, most of which were healthy and some of which didn’t even want the money? And then the automakers and (for all I know) Orange Julius producers started asking Paulson for their piece of the action?

Well now the transformation is complete. According to the headlines on CNBC (but for which no story is yet available*), Paulson is right this moment explaining that not one penny of the $700 billion will actually be used to buy “toxic” assets. That’s right, about 5 or 6 weeks after asking Congress for $700 BILLION for Unbelievably Important Task A, Paulson is now admitting that he has decided in the interim that actually, that money is better spent on Super Unbelievably Important Tasks B, C, D, …

In the beginning I thought Paulson was an evil genius. Now I’m wondering if maybe that is only half right.

* UPDATE: Here is a brief story with this juicy quote:

Paulson, in an update on the Treasury’s financial rescue efforts, said his staff has continued to examine the benefits of purchasing illiquid mortgage assets under the so-called Troubled Asset Relief Program.

“Our assessment at this time is that this is not the most effective way to use TARP funds, but we will continue to examine whether targeted forms of asset purchase can play a useful role, relative to other potential uses of TARP resources,” Paulson told a news conference.

So, umm, what exactly changed in the last 5 weeks? Many economists were saying from the get-go that his plan made no sense. Was it that Paulson’s staffers actually read some of the informed critiques of the plan, after they literally begged Congress for the money and warned that the world will end if they didn’t get it for their Unbelievably Important Plan? Actually, that probably wasn’t it. It was probably more like, Paulson and his staff discovered for themselves that their plan made no sense, without having read any of the outside commentary on it.

Consumers Don’t Cause Recessions

Ah, I have outdone myself in this one. You know how you’ve wanted someone to rip apart the “circular flow diagram” for years? Well, enjoy. Learn it. Live it. Love it. Here’s an excerpt for those readers who are “busy” and need a hint before clicking a link:

In his discussion of the “paradox of thrift,” Paul Krugman proves that he is not an economist—or at least, not a very good one. His policy recommendations are based on a Keynesian model bereft of time and the capital structure of production. Recessions are rooted in misalignments in this unbelievably complex structure, and there needs to be a period of below-normal output as these pipelines are fixed. Most important, consumers are doing the right thing when they increase their saving during a downturn. If solving a recession really were as simple as getting people to spend, then we wouldn’t keep experiencing them.

A Reader Shares Her Airline Tax Story

Reader Lisa M. emailed to tell of her ordeal with the FAA / American Airlines. I’m not sure how much good it will do to publicize this, but I was stunned by the story (which seems real, e.g. the electronic receipt looked authentic) and so I am passing it along. The following is her letter to an American Airlines representative.

==========

Good Morning Mr. Smith,

I have left you a voice mail earlier this week during your absence but I thought it may be beneficial to send you a copy of the complaint I sent to the FAA regarding over charge of tax by American Airlines and possible gas gouging.

—————————————————————————————

I have tried to rectify a TAX issue with American Airlines. My base fare is

$701.80 with Taxes of $398.60 for a Total of $1100.40. Every other flight that date on AA to the same routes had taxes of $97.50 or less. As of yesterday, the tax was $84.50.

When I spoke with the airlines, I was told my tax is $429. Yet on my ticket it clearly states $398.60.

I asked two different people on two different dates for an explanation of why I was charged an additional tax of $301.10. The first person told me it was a luxury tax and the next told me it was a fuel surcharge tax.

I have the following questions:

Why was only this flight on that day charged $301.10 additional fuel tax charge

Moreover, no other flights that day were charged this tax?

If it is a fuel charge tax that has since been reduced due to falling fuel

prices, why am I not being refunded the tax as I have not flown yet

nor has the airlines incurred the fuel charges.

This amounts to gas gouging.

The same flight today cost base $867 tax $83.90 Total $950.90.

I was also told since my base fare is less then the current base fare

I would have to pay a penalty to get a less expensive fare.

I am asking for the additional tax of $301.10 be returned to me.

Record Locator/AA Confirmation:ELV***

Itinerary

Date: 20Dec – Saturday

Flight: AMERICAN AIRLINES

OPERATED BY AMERICAN EAGLE 4474 Embraer RJ145(ER4) Booking Code: S

Departure: JAX Jacksonville 12:50 PM 2HR 50MIN

Arrival: ORD Chicago 02:40 PM

M., LISA

SEAT 8C Economy FF# :AA 4H4****

Date: 20Dec – Saturday

Flight: AMERICAN AIRLINES 92 Boeing 767-300 Passenger(763) Booking Code: S

Departure: ORD Chicago 07:20 PM 7HR 10MIN

Arrival: DUB Dublin 08:30 AM

M., LISA

SEAT 25J Economy FF# :AA 4H4****

Date: 06Jan – Tuesday

Flight: AMERICAN AIRLINES 93 Boeing 767-300 Passenger(763) Booking Code: V

Departure: DUB Dublin 10:30 AM 8HR 25MIN

Arrival: ORD Chicago 12:55 PM

M., LISA

SEAT 24J Economy FF# :AA 4H4****

Date: 06Jan – Tuesday

Flight: AMERICAN AIRLINES

OPERATED BY AMERICAN EAGLE 4503 Embraer RJ145(ER4) Booking Code: V

Departure: ORD Chicago 06:05 PM 2HR 30MIN

Arrival: JAX Jacksonville 09:35 PM

M., LISA

SEAT 13A Economy FF# :AA 4H4****

Receipt

PASSENGER TICKET NUMBER FARE TAXES TICKET TOTAL

M.,LISA 0012116****** 701.80 USD 398.60 1100.40

Payment Type:

AMERICAN AIRLINES *********7809

Total

1100.40

Kind Regards,

Lisa M.

Peter Klein Stands Up for the Small Businessman[woman]

Peter Klein wants consumers to stop gouging gas station owners. (HT2 Steve Horwitz)

Please join me in support for poor, beleaguered gas station owners, the victims of unconscionable price gouging by ruthless consumers who are taking advantage of market conditions to reduce their demand for gasoline, driving down the price by nearly $2 per gallon over the last four months. Fortunately, governments are swinging into action. Georgia governor Sonny Perdue issued this statement: “The financial crisis has disrupted the consumption of gasoline, which will have an effect on prices. However, we expect the prices that Georgian gasoline station owners receive at the pump to be in line with changes in consumers’ incomes and the prices of substitutes and complements. We will not tolerate consumers taking advantage of Georgian business owners during a time of emergency.”

I should point out that the fall in gasoline prices really isn’t because of a drop in consumer demand; I think it’s almost entirely due to falling crude prices. So technically that would be an increase in the supply curve of gasoline at the retail level (since producers’ input prices have fallen). In other words, it’s not that motorists have decided they don’t want to drive as much at each hypothetical price of gas, just like the huge run-up in gasoline prices wasn’t because they all of a sudden enjoyed driving more. Klein obviously knows all of this, but it’s not clear if he was purposely botching the analysis in the above to make the joke.

Recent Comments