The LEGO Movie Is AWESOME

From my gushing review at Mises Canada:

Let me tackle the other stumbling block for free-market libertarians: The name of the villain is “President Business.” Thus, some viewers complained to me that the movie had an anti-market message.

…

Remember, the underlying theme of the LEGO movie is that America is turning fascist. Now what is fascism? It is the unholy alliance of Big Government and Big Business. So if you are making a kids’ movie and want to drive home the point, what do you do? You make your villain simultaneously the head of the democratic government and the head of a major corporation that provides security cameras, controls the media, and even publishes the history books (yes they explicitly say all that in the LEGO movie).

Remember, the villain is President Business; don’t focus on just the second half of his title. His chief enforcer isn’t a private mercenary, but instead is the head of the police (voiced by Liam Neeson), with the name “Bad Cop.” His robotic enforcers are called “Micro Managers.” If you watched this movie and came away sulking that it was bashing markets, then congratulations you have the same sophistication as the analysts on FOX news who are fans of Mitt Romney.

Potpourri

==> The Economist magazine gets on the Bitcoin bandwagon. (HT2 Tyler Cowen)

==> The haughty von Pepe sends this Cochrane post in which he (Cochrane) points out that Yellen has thrown policy rules completely out the window.

==> David R. Henderson describes his flawless victory on ObamaCare.

==> Is China going to back its currency with gold? My latest Mises Canada post. (HT2 Frank C. for the tip.)

Potpourri

==> Salim Furth does a good job showing something pretty screwy with one of Krugman’s favorite scatter plots.

==> David Stockman has a new blog, I just learned.

==> At first I thought Pete Boettke was wrong in this analysis, but then I realize he’s right (in terms of his particular point): Even though there are an unfathomable number of “possible states” in which the chess board can (legally) be, there are way more possible states of the soccer field or basketball court, perhaps even rendering the concept nonsensical. On the other hand, there is an obvious sense in which computers (embedded in robots) will one day in the not too distant future obviously be able to beat human athletes in these standard sports.

==> In this new analysis for the Fraser Institute, some colleagues and I show that Ontario has a much larger government debt than the state of California.

==> More atheist bashing from Gene Callahan.

==> In a moment of weakness, I clicked on a BuzzFeed link in my Facebook feed, but this is actually pretty cool.

Let’s Be Careful With “Spreading Out” Damages

Lately at his blog, David Friedman has been doing a great job challenging the “the science is settled, we need a big carbon tax NOW” dogmatism. However, in a recent critique of an older piece by William Nordhaus (which I myself criticized at IER when it came out), Friedman makes a move that seems rather dubious. It doesn’t necessarily flip Friedman’s overall point, but I just want to point it out since I see people on both sides of the debate using this technique. So here’s Friedman talking about Nordhaus’s study of the climate change issue:

[Nordhaus] finds that the net cost of waiting fifty years instead of taking the optimal actions now is $4.1 trillion dollars. Spread out over the rest of the century, that comes to about $48 billion/year, or about .06% of current world GNP. Which position is that closer to, that there is a need to panic and take drastic action or that there is not?

I claim that Friedman’s move here is really fishy, and I am pretty sure I complained when Krugman used a similar trick to show why cap-and-trade was also really “cheap.” (I’m not going to bother looking it up.)

What Nordhaus looked at was the present discounted value of the flows of costs and benefits from various strategies regarding climate change. If governments around the world imposed the “optimal” (in a Pigovian sense) carbon tax immediately, it would reduce conventional economic growth but it would mitigate climate change damages. Humanity would be richer by $X trillion, where X>4.1. Instead, if humanity did nothing for 50 years and then implemented the optimal carbon tax worldwide, from today’s vantage point this would still be better than the status quo of no controls on emissions, but the gains would be smaller; humanity would only be richer by $(X – 4.1) trillion.

Now to say a policy decision has a cost of $4.1 trillion in today’s terms (actually back in 2012 when the piece came out, since Nordhaus at that point was updating his 2008 numbers), is a pretty big deal. As Nordhaus himself points out, that’s how much major wars can cost. If somebody tried to say the Iraq and Afghan invasions and occupations weren’t a big deal because they only reduced world GNP by 0.06% through 2100, that would be a bit weird wouldn’t it?

It’s not clear why Friedman picked the end of the century, either. If we’re not going to use a single number today for the cost, then the only non-arbitrary “spreading out” period would be the 50 years where we’re delaying. To put the point differently, why not spread the cost of “doing nothing for 50 years” out until the year 2400? Then it would be virtually zero percent of world output per year.

But there’s another problem. Friedman isn’t doing the conversion properly. He apparently came up with his number by taking $4.1 trillion and dividing by 85 years, since we’re already into 2014 and so “through the rest of the century” means another 85 years. (Note that $4.1 trillion / 85 = $48.2 billion.)

But that’s just plain wrong. You can’t ignore interest on an 85-year amortization schedule. At a 3% interest rate (which might be what Nordhaus used himself, when discounting the flows of costs and benefits from various policies–I can’t remember off the top of my head), you would have to make 85 annual payments of about $134 billion in order to knock out an initial debt of $4.1 trillion (assuming no midnight Excel mistakes on my part). That’s almost triple the number Friedman came up with; you really can’t ignore discounting if you’re going to “spread the costs out” over 85 years.

Anyway, you can either view my post here as a wonderful display of intellectual honesty, in criticizing someone who’s on “my side” of an issue. Or, you can think I’m still sulking about my debate with Friedman last Porcfest (which now has more than 21,000 views!). Either way, kids, be careful about turning lump sums into annual amounts.

UPDATE: After posting I realized I should clarify two things, especially for the casual reader:

(1) I am a HUGE CRITIC of Nordhaus’ entire approach. Indeed, I have an article at The Independent Review going methodically through Nordhaus’ DICE model and his case for a carbon tax. All I’m saying in this post is that Friedman was trying to use Nordhaus’ own calculations against him, and I think Friedman didn’t make a good move on this minor rhetorical point.

(2) If we’re going to pick discount rates for this type of thing, I think 3 percent is too low. But I wanted to be generous with Friedman (since the bigger the discount rate we use, the worse his estimate of $48 billion would look compared to the “true” number). Also, perhaps more relevant, Nordhaus himself was using a discount rate to turn the flows of costs and benefits into a PDV of $4.1 trillion. So to turn that lump sum back into annual flows, it seemed to me more reasonable to pick a discount rate like 3 percent, since a lot of the economists in this field use lower discount rates than I personally think are appropriate. But like I said in the original post, I can’t remember which discount rate Nordhaus used; for all I know he picked 5 percent in these model runs.

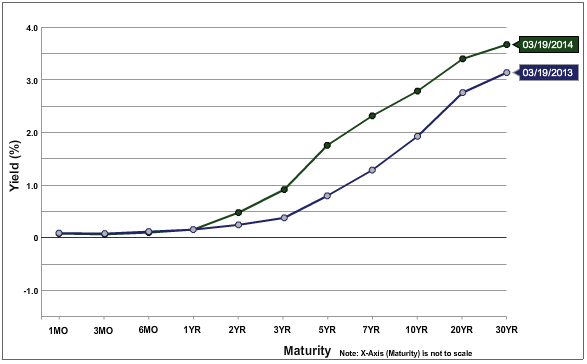

Medium-Term Treasury Yields Rising Quickly

On a conference call today with some people in the financial sector I made sure everyone was aware of this:

I think a lot of casual observes (i.e. not the bond traders obviously) just think about the fed funds rate, and maybe the really short maturity Treasuries. But as the chart above shows (from here), the yields on 7-year and 10-year Treasuries have risen dramatically in just the last twelve months. In particular, the nominal 7-year yield has risen from 1.23% to 2.31%.

There are lots of ways to explain what’s happened, but be careful–if you go to the link and fiddle around with the settings, you’ll see that back in March 2011 (i.e. three years ago), the yield curve was uniformly above where it is right now.

I realize some of us have been raising alarm bells since the winter of 2008, and that other analysts have accused us of crying wolf, but I really don’t see how this ends well. The Keynesians have lectured guys like me saying, “When nominal interest rates are near zero, bonds and cash are interchangeable, so open market operations don’t have the usual impact on spending and prices.” OK, so what happens if the yield curve keeps shifting up, especially if the increase filters down to the shorter maturities? At some point, the commercial banks are going to resume normal lending, and the Fed will have to either raise the interest rate it pays on excess reserves, or it will have to rapidly reduce its balance sheet. Either way spells trouble.

Michael Goldstein on the Anarchist Roots of Bitcoin

Before any Rothbardian offers further commentary on Bitcoin, I highly encourage him or her to watch this short presentation. This is one of the things that really made me get off the fence regarding Bitcoin. (Note: I’m not saying Bitcoin will ever be the global money; it’s possible that governments keep it underground. I will write more on this, soon. But I’m saying I don’t think Bitcoin is a faddish bubble like tulips; Bitcoin–or a variation of it–is here to stay.)

For more, go to the Satoshi Nakamoto Institute.

The Continuing Importance of Capital Theory

My new post at Mises Canada, which on Facebook I summarize as “Friedrich Hayek >> Scott Sumner.” An excerpt:

Now if Sumner’s explanation were the main thing going on, there would be two immediate implications: (1) Booms are good things. And (2) Booms should naturally slide back into normal growth as wages and prices adjust; there is no reason we should ever see a massive slump following a boom. Austrian economists sometimes chide their Keynesian foes for wanting “a perpetual boom,” but here Sumner is explicitly endorsing such a position too (whether or not he realizes it).

In the Austrian approach, on the other hand, there is no mystery here. The layperson’s intuition is right: A boom feels good because it really is a period with an above-normal standard of living, but it is genuinely unsustainable and it is bad. People come to realize at some point that the boom is illusory, and this realization leads not just to a return to normalcy, but a slump. How can we explain these facts? Because during the boom period,people unwittingly consume capital.

If a businessperson who owned a fleet of trucks suddenly stopped spending money on oil changes and didn’t get new brakes even for the vehicles that “needed” them, these decisions would boost (apparent) profitability in the short run. Not only would monetary expenses be reduced, but revenue would be higher, since the entire fleet could be out delivering cargo, rather than having some of the vehicles (at any given time) tied up in maintenance. Yet obviously this temporary boost in profitability would be a sham, with a disaster looming on the horizon.

Recent Comments