Ten Things I Hate About the Efficient Markets Hypothesis

Well maybe not ten, but Scott Sumner hits a bunch of my pet peeves in this post:

Commenters often present me with market anomalies, which supposedly “prove” the efficient markets hypothesis is wrong. I always respond that they’re just engaging in data mining. They retort that no theory that can’t be disproved is worth anything. But the EMH can be disproved. The tests have been done, and it passes. Sort of.

OK, that “Sort of” is a little odd, but clearly at this point, Scott is saying the EMH is a falsifiable theory. Let’s continue:

Finance professors have done many different tests of the EMH, and I’d guess 90% of the published tests (but only 5% of the actual tests) show that the EMH is wrong. (Yes, I’m pulling these numbers out of thin air, but you get the point.) They’ve found January effects, small stock effects and value stock effects. They’ve found the market does better when P/E ratios are low. They found the market does worse on rainy days (a study published in the AER!).

Boom, that’s it, right? These are all things that, prima facie, shouldn’t be true if the EMH is right. In fact, Scott himself agrees that these tests “show that the EMH is wrong”; don’t take my word for it. So case closed, right? Nope:

Of course you’d expect to find 5 anomalies for every 100 tests you do, and for the most part you only get published if you find an anomaly, and finance professors have a lot of computer power, so . . .

Here’s my analogy. Suppose Stephen Wynn was concerned that some mysterious gamblers were getting away with cheating at one of his casinos. He’d heard rumors, but had no proof, or even suspects. You are statistician brought in to investigate. You study 600 slot machines, and find 30 of them produced three cherries more often than you’d expect from mere chance. You suggest that the anomalous slot machines be destroyed. How should the casino owner react to that “investigation?” I’m guessing Wynn wouldn’t be impressed.

I’m not sure that’s a good analogy. But doesn’t matter, suppose it is. Let’s move on to what really bugs me:

To find out whether cheating is occurring you need to look at whether the winnings of gamblers are serially correlated. Are those who win once, more likely to win next time. That’s the proper test, indeed the only practical test, of whether people are cheating the casino. And it’s also the only test of the EMH. Don’t look for “the system,” the secret way to beat the stock market. Look for whether other people have found it. Look to see whether people who did better than average one year, tended to do better than average the next year. Don’t look for market anomalies—look for evidence that other people have found market anomalies.

Of course the study has been done. I recall that Fama and French found that mutual returns were approximately serially uncorrelated, but not exactly. There appears to be a slight serial correlation among the very best funds (top 3%), but not enough to give the average investor any advantage.

And that’s what I would have expected. The EMH is approximately true; indeed it’s almost impossible for me to imagine any other model of financial markets. But it’s not precisely true, again, just as you’d expect. After all, if the EMH were perfectly true then no one would have any incentive to estimate fundamental values.

Huh? This is the same trick that the evolutionary biologists pull–“Our theory is so right, that even when the data don’t support it, it just proves how right it is.”

Note that I’m not saying, “The EMH is wrong,” or even that, “Evolutionary biology doesn’t fit the data.” What I have said over and over is that the EMH is a way of viewing the world. No matter what happens, Scott Sumner would say, “See? Just what I would have expected.”

Don’t believe me? Look at this:

A smart person like Eugene Fama should have been able to come up with both the EMH, and its limits, by just sitting in a room and thinking. Much as David Hume got the QTM by imagining what would happen if everyone in England woke up one morning with twice as much gold in their purses. Or Fisher’s theory of inflation and nominal interest rates. Or Cassel’s purchasing power parity. Or Friedman/Phelps’ natural rate hypothesis. Or Muth and rational expectations. Certain ideas are simply logical, and that’s why I have no doubt that despite all those economists on the left arguing the EMH has been discredited, it will still be taught in every top econ/finance grad program 100 years from now, whereas fiscal stimulus will be long gone from macro textbooks.

See? If you can derive a theory by sitting in a room and thinking, then it is not an empirical theory. So let’s drop the charade and stop pointing to all of Fama et al.’s “tests” of it. Just admit it is a very useful way of viewing the world, like supply and demand. Have the courage, as Ludwig von Mises did, to say that it is an a priori approach that could not possibly be falsified.

But instead, just about every EMH supporter I have read thinks it is an empirical claim, open to falsification. They just don’t realize that they can explain everything. If sophisticated hedge funds are making a bunch of money, that just proves how hard it is to “beat the market”; you need to spend a bunch of quants and computers.

And if the hedge funds all blow up, while guys like Mark Thornton called the housing bubble in 2004? Nope, just shows Thornton got lucky, and how hard it is to beat the market. (I’m not exaggerating; that’s exactly what Jeremy Siegel said in the WSJ, defending the EMH, as I explain at the bottom of this article.)

So whether hedge funds make a killing or blow up, it just shows how rational markets are. The EMH–a scientific theory, subject to falsification–passes its test with flying colors.

Ferguson: A Crash Is Coming

I am not kidding when I tell people the economy is like Wile E. Coyote before he looks down. (And of course I didn’t invent that great metaphor.) I truly check the financial news every morning, wondering if the dollar had crashed earlier that hour.

I was flipping through my radio yesterday and hit upon Fred Thompson reading from an op ed that summed up my views better than anything I’ve heard in a while. It turns out the author was Harvard historian Niall Ferguson. Check this out:

In imperial crises, it is not the material underpinnings of power that really matter but expectations about future power. The fiscal numbers cited above cannot erode U.S. strength on their own, but they can work to weaken a long-assumed faith in the United States’ ability to weather any crisis.

One day, a seemingly random piece of bad news — perhaps a negative report by a rating agency — will make the headlines during an otherwise quiet news cycle. Suddenly, it will be not just a few policy wonks who worry about the sustainability of U.S. fiscal policy but the public at large, not to mention investors abroad. It is this shift that is crucial: A complex adaptive system is in big trouble when its component parts lose faith in its viability.

Over the last three years, the complex system of the global economy flipped from boom to bust — all because a bunch of Americans started to default on their subprime mortgages, thereby blowing huge holes in the business models of thousands of highly leveraged financial institutions. The next phase of the current crisis may begin when the public begins to reassess the credibility of the radical monetary and fiscal steps that were taken in response.

Neither interest rates at zero nor fiscal stimulus can achieve a sustainable recovery if people in the United States and abroad collectively decide, overnight, that such measures will ultimately lead to much higher inflation rates or outright default. Bond yields can shoot up if expectations change about future government solvency, intensifying an already bad fiscal crisis by driving up the cost of interest payments on new debt. Just ask Greece.

Ask Russia, too. Fighting a losing battle in the mountains of the Hindu Kush has long been a harbinger of imperial fall. What happened 20 years ago is a reminder that empires do not in fact appear, rise, reign, decline and fall according to some recurrent and predictable life cycle. It is historians who retrospectively portray the process of imperial dissolution as slow-acting. Rather, empires behave like all complex adaptive systems. They function in apparent equilibrium for some unknowable period. And then, quite abruptly, they collapse.

Washington, you have been warned.

For those of you who are inclined to “big player” worldviews, note that the op ed is adapted from a paper Ferguson wrote in Foreign Affairs, the publication put out by the Council on Foreign Relations.

As I blogged just last night: deep doodoo.

Caplan’s Anti-Religious Non Sequitur

Because of my son’s last cross country meet on Sunday, I missed my regularly scheduled religious pontificating. So I will make up for it by a quick reaction to something Bryan Caplan posted over at EconLog.

First, Caplan quotes from a Pew Forum poll which shows some pretty abysmal performances from self-identified religious Americans. (The example that bothered me the most, was that 53% of Protestants couldn’t identify Martin Luther as the person who inspired the Reformation.) OK that’s embarrassing, but I also would be embarrassed by what self-described “believers in the free market” had to say about economic theory.

Then Caplan goes in for the kill:

Now consider: If people sincerely believed that their eternal fates hinged on their knowledge of religion, their ignorance wouldn’t be rational. If you could save your soul with 40 hours of your time, you’d be mad to watch t.v. instead. Unfortunately for religious believers, this leaves them with two unpalatable options:

1. Option #1: Deep-down, most religious believers believe that death is the end. (This is consistent with the fact that even the pious mourn their loved ones at funerals, instead of celebrating the good fortune of the deceased). Even if this covert atheism is mistaken, the idea that most of the people in church aren’t true believers seems threatening.

2. Option #2: Most religious believers are so stupid and/or impulsive that they’ll knowingly give up eternal bliss for trivial mortal pleasures. But why then do so many believers show intelligence and self-control in other areas of life?

My question for Bryan: Has there ever been a major religion in the history of the world that taught “you could save your soul with 40 hours of your time”, in the way Bryan means in the quote above? I can’t think of any (but that might just be my rational ignorance).

If not, then isn’t it a rather poor premise, upon which Bryan leaps to the alternative that religious people are either liars or stupid?

Last point: I have said this before, I think when dealing with Steve Landsburg’s recent book. For some reason, really intelligent atheists who are extremely open-minded–people who would bend over backwards to be fair to Keynesians and Marxists when evaluating their arguments–don’t seem to think it’s necessary to be careful when evaluating what is obviously the single most important question of human existence. I’m not saying they’re stupid, just incredibly overconfident.

OK kids, back to secular matters. We will return to our economic discussions, until Sunday.

The Dollar’s Demise?

Robert Wenzel has recently started the EPJ Daily Alerts. I try to check it out everyday; it reassures me to know Wenzel is out there, scouring the internet for new developments. (He’s not paying me to say that, but he’s also not charging me for the subscription.)

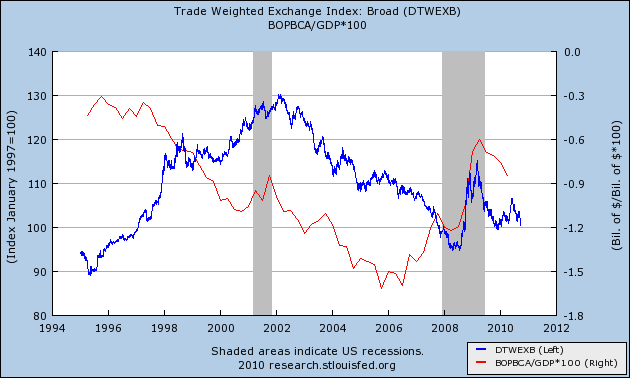

In today’s Alert, Wenzel mentioned that the dollar is at a 5-month low. So I decided to check things out with the trusty graphing tools at the St. Louis Fed (which, incidentally, are a lot more powerful than they used to be):

The eclectic von Pepe and I have a running joke where I tell him, “I had to stop looking at these charts before I turned into Nash.” (I.e., if you stare hard enough at something, you will “see” a pattern.)

Even so, my Spidey sense is tingling. In July 2007 I did a forecast for a bank (which later inspired this somewhat-prescient article) in which I realized people like Peter Schiff were totally right in their doomsaying.

Part of what pushed me over the edge was that the current account deficit’s increase (i.e. getting more negative) went hand in hand with a falling dollar. That told me that the people who were saying, “Don’t worry, trade deficits are fine, people love U.S. assets and a current account deficit is just the flip side of a capital account surplus” were fooling themselves.

That type of story made sense in the late 1990s, when the dollar was gaining strength against other currencies even as the current account deficit grew. But from 2002 onward (in the midst of Greenspan’s rate cuts) the dollar started tanking even as the current account deficit grew. So that told me all was not well.

But now flip things around and look at what’s happened in the last few years. To hear Krugman and DeLong tell it, the reason the dollar has gone up so much, is that everyone’s rushing to buy Treasurys.

But if that’s the case, then wouldn’t the dollar’s rise be sharper than the “improvement” in the current account deficit?

Yet the chart shows the opposite. In other words, it looks like the dollar was pulled up by Americans’ spending habits, not because foreigners all of a sudden really wanted to get more US financial assets.

Standard disclaimer: It’s almost bedtime and we probably need to decompose these variables to truly test these hypotheses. But from staring at this graph (and also the plunge in the dollar during the last few months), I think we have yet more evidence that we’re in big doodoo.

Now It All Makes Sense…

Has anyone ever seen Tyler Cowen and Paul Krugman in the same room at the same time?

Reuters Readers Ruv Me

At least according to the first two commenters. Here’s an excerpt of my op ed on fiscal austerity–and I had to rely on your guys’ help with digging up the European statistics:

The ECB documented several episodes when a government implemented aggressive policies to reduce its budget deficit, and the result was a stronger economy. Specifically, they reviewed the experiences of Belgium, Ireland, Spain, the Netherlands, and Finland in successfully reducing their budget deficits. Three of the countries—Ireland, the Netherlands, and Finland—saw immediate improvements in economic growth, but all benefited from tightening government finances.

Consider the case of Finland. From 1993-1997, its government budget deficit averaged -5.2 percent of GDP. But starting in 1998, the string of deficits turned into a string of surpluses, which averaged +3.8 percent of GDP from 1998-2002.

Finland embarked on this austerity program in the midst of high unemployment, which was 12.7 percent in 1997 (the last year of a budget deficit). In the first year of surplus, the unemployment rate had fallen to 11.4 percent, and it continued to fall in the subsequent years. It’s true, Finland’s unemployment had been falling steadily since its peak, at 16.6 percent, in 1994, but the crucial point is that the austerity program didn’t reverse the trend.

Turning from the labor market to total economic output, we find that in 1997, GDP growth was 2.0 percent, while in 1998 — the first year of a budget surplus — GDP growth rose to 3.4 percent. Also, average GDP growth was slightly higher in the first three years of budget surpluses, than in the preceding three years of budget deficits.

Now a Keynesian cynic might argue that Finland’s economy, for whatever reason, naturally recovered in 1998, and that this lightened the load on government social programs while bringing in more revenues. So perhaps the switch from massive budget deficits to sizable surpluses was a consequence, not a cause, of the improving economy.

It’s true that we can’t run a controlled experiment in macroeconomics. But in 1998, when the Finnish government went from a string of deficits to a string of surpluses, government expenditures fell sharply as a share of GDP — from 56.5 percent down to 52.9 percent in a single year. Yet the fall wasn’t merely relative: the Finnish government actually cut the absolute size of its budget by some 50 million euros. This cut was not large — less than 1 percent of the budget — but still impressive at a time when the unemployment rate had averaged almost 13 percent the prior year.

BTW for a purist, let me admit my wording was less than desirable in the above. What I was trying to say is that they achieved their deficit reductions by holding absolute spending in check, so that the economy’s growth lowered expenditures/GDP.

That is practically unheard-of in conventional fiscal punditry. It’s just assumed that spending in absolute dollars will rise, and that tax hikes (on “the rich”) are needed to boost revenue/GDP.

Groupon: Another Market Success

Details here. Incidentally, the most important part of this article–the news you can use–isn’t about Groupon, but about its parent site:

As I was investigating the website for Groupon, I discovered that it was a specific application of the more general website, The Point. As the short video at the link explains, The Point exists to solve collective-action problems. Whether it’s something trivial like raising money from coworkers to buy a ping-pong table for the break room, or something grand like raising a million dollars to fund a long-shot political candidate, The Point offers a convenient way for people to conditionally pledge to give money (or perform some other action) if enough other people sign on.

What’s especially intriguing is that The Point offers members the option of joining a cause anonymously, with their identity being revealed only if the “tipping point” (hence the name) has been reached.

Conclusion

Groupon is an extremely clever idea with an equally catchy name. It is just one example of the solutions that free entrepreneurs can dream up to solve social problems. Libertarian dreamers should familiarize themselves with the campaigns at The Point to see if there are applications to achieving their ends, such as adopting alternate currencies or developing a Friedrich Hayek Super Bowl commercial.

Wall Street 1: Murphy Never Sleeps

In preparation for Sunday’s viewing of Wall Street 2: Money Never Sleeps, I decided to watch the original. (Fortunately you can watch it instantly on Netflix.) This postponed by a day my usual catch-up on sleep, but it was worth it.

I’m ashamed to say that I don’t think I ever gave the movie a chance when I was much younger. Back then, I let the conservative op ed writers convince me that Oliver Stone was a nutjob who hated America and capitalism.

Well, I didn’t get that sense from the movie. (Maybe Stone has said some crazy things in interviews; I don’t know.) It’s true, Gordon Gekko is not portrayed as a hero, or even a flawed hero, but I don’t think Stone did a hatchet job on him. I mean, you don’t cast Michael Douglas as a character unless you sort of respect him.

By the same token, Stone didn’t do a hatchet job on George Bush in W. I think Stone set out to give an accurate account of how the heck somebody ends up making the decisions (in the White House) that horrified Stone.

(To see the contrast, Danny DeVito’s character in Other People’s Money wasn’t a patch on the shoulder blade of Gordon Gekko. Besides more obvious differences, their speeches to the shareholders were different. Gekko’s famous “greed is good” speech is actually mostly correct, and he rightly castigates the incompetent management. In contrast, I don’t remember DeVito even giving a semblance of an argument as to why the shareholders should sell to him, except “You’ll make a lot of money.”)

But enough of the praise. I have huge problems with a central part of the plot in the original Wall Street.

(1) First of all, why could Gordon Gekko lay off the union workers and gut the company? The union representatives specifically ask him if he will put all of his promises in writing, when they meet at Charlie Sheen’s place. This isn’t terrible–we could assume Gekko had his attorneys draft up something with a loophole that the salt-of-the-earth union people didn’t see coming. But then…

(2) If Gekko is planning to break up the company and raid the pension fund, why does he care when the union people come in and threaten to not concede to his requested wage cuts? He only needs their wage concessions if he’s planning on operating the airline, right? So if he’s really going to eliminate everybody’s job–as Charlie Sheen begs him not to do–then it doesn’t matter if the unions don’t go along with the original agreement. So why does their threat convince him to dump the stock?

Maybe I’m missing something, and there was supposed to be a transition period when Gekko winds down the company. But the investment bankers were making it sound as if the whole strategy was to sell off the assets and allow Gekko to retain the overfunded pension.

{kind=link}

Recent Comments