Inside Job a Scathing Indictment of Professional Economics

I don’t know what the deal is, but I can’t find the NPR story on the documentary Inside Job that I heard just this week. Instead, I can find this earlier interview with the film maker that aired in October:

Now I want to caution free-market economists against focusing on incidentals. Sure, the guy making this film (I’m guessing) wants much more stringent government regulation of the financial industry, and he wants people to go to jail for things that you and I might think were not crimes.

But please don’t dismiss the level of corruption he has uncovered in academia, and also the revolving door between academia, investment banks, and government regulatory positions (including Treasury Secretary and the New York Fed). The interview above shows Glenn Hubbard in the hot seat, but the one I heard earlier this week also featured the famous “gotcha” with Mishkin, and it discussed the Goldman Sachs connection.

What I really don’t want to to see happen, is what occurred in the wake of Naomi Klein’s book The Shock Doctrine. When I read that, I was stunned by the horrific things that the U.S. government had done to psychiatric patients, and the odious foreign regimes that were openly advised by Chicago-trained economists.

But most libertarians didn’t care about any of that; they merely bristled at Klein calling all of that “capitalism.”

Gold: The Market’s Global Currency

Here is my Mises Daily about Robert Zoellick’s halfhearted call for a return to gold.

Also, the Hillsdale Collegian ran a story on the Krugman debate, though I actually stopped teaching there in 2006 (not 2008 as the article states). Since there are one or more Hillsdale economics professors who read this blog, I want to highlight this part of the article:

Joe Petrides, who graduated from Hillsdale in 2006 with a degree in economics, found out about the campaign through Murphy’s YouTube videos.

“I thought he was the smartest economics professor, as far as depth of knowledge goes,” Petrides said, recalling classes he took with Murphy. “He knows the minute details of the arguments. He won’t be scared by Krugman’s celebrity status.”

Frank Zappa versus Bryan Caplan

Whatever the post title suggested to you, I promise the actual post will fail to live up to your hopes…

Recently Bryan wrote a post with the implausible title, “Why T.V. is Great for the Family,” which I reproduce in full:

Yesterday my baby acquired a valuable life skill: He learned how to watch television. I’m thrilled for at least three reasons:

1. Television is fun. I don’t want my son to miss out on one of life’s great pleasures.

2. Television is a cheap electronic baby-sitter that allows parents of young kids to get a much-needed break.

3. When my son is older, the threat to deprive him of television will become one of our most convenient and effective tools of discipline. The naughty corner’s usually enough, but when bad behavior persists, it’s time for a night without t.v.

Won’t t.v. stunt my baby’s cognitive development? Hardly. Twin and adoption studies find zero long-run effect on IQ of all family environment combined. Television’s isn’t just a drop in the bucket; it’s a drop in a bucket that doesn’t hold water.

Now I was going to let this go, I really was. But then I read Stephan Kinsella praising Bryan, and it pushed me over the edge. Particularly when Stephan wrote: “One reason I like it is I’m sick of “Oh, I don’t have a television” snobs. Also of hand-wringing one-size-fits-all humorless drones.”

Well call me a “Oh, I don’t have a television” snob. I also drink tea and pee sitting down (at least in the middle of the night). Wassup, Stephan?

First of all, note that you could use Bryan’s arguments to explain, “Why Cigarettes are Great for the Family.”

Second of all, the objection to TV watching isn’t that it reduces your IQ, but that it fills your mind with garbage. Someone can be very intelligent but also quite ignorant and full of fallacies.

Third, I really really really don’t agree with Caplan’s conclusions from the twin/adoption studies. I confess I haven’t delved into the literature first-hand. But I know when I read the first Freakonomics book, the presentation horrified me. Assuming Levitt and Dubner summarized the research correctly, I believe they were arguing (to paraphrase): ‘If a parent orders his kid to turn off the TV and read a book, that won’t make the kid do any better on standardized tests. What the kid actually responds to, though, is being raised in a household where the parents value reading.’

So yes, I don’t deny that regressions on my kid would fail to pick up a statistically significant impact from the lack of a television. What I predict will be his above-average scores on standardized tests could be explained by my PhD, the amount of books we have around the house, the IQs of my wife and me, etc. I grant that there isn’t a big enough sample size to distinguish the Caplan household from the Murphy household. (I.e. Caplan has a PhD in economics too, presumably has a lot of books, blah blah blah. But the relative performance of our kids isn’t a smoking gun as to the effects of TV watching.)

But do Bryan and Stephan really want to say that it’s better for a kid to watch TV, say, two hours a day, rather than playing sports or reading a book?

I think I have noticed just how ridiculous TV has gotten lately, because I only see it infrequently (when I go to a hotel, visit relatives or friends, etc.). Just about every prime-time show has to have a very attractive female lead, preferably showing cleavage. I was watching a show on a channel like A&E (it may not have literally been A&E) called, “The 10 Most Ridiculous Ways to Die” or something like that. And the #3 or so ranked way was a lesbian woman choked to death on her partner’s edible underwear. Naturally, they did a re-enactment of the scene that would have been rated R 20 years ago.

I realize now I sound like the religious prude. Well no libertarian can possibly say that about Mr. Zappa:

Slate Yesterday, Daily Show Tomorrow?

[UPDATE inserted below.]

A few people today have sent me this Slate article that links to one of my old Mises Daily articles. Just when I’m about to give up economics and go full-time into male modeling, they pull me back in…

On a more serious note, what’s the story with this guy J.D. Foster from the Heritage Foundation? It sounds like he’s trying to hang out with the cool kids at Slate and UC Berkeley, who go behind the house and roll joints out of fiat currency. Check out this final quote:

If a gold standard is so problematic, why do so many people—including Ron Paul and various libertarian economists [That’s me.–RPM]—want to peg the dollar to it? Part of the reason is distrust of the Federal Reserve. The gold standard takes the power to manipulate currency out of the Fed’s hands, which economic libertarians consider a good thing. Another reason is that gyrating exchange rates make international trade difficult, since prices are always changing—better to have every economy pegged to the same index.

But economists say you can’t force currency to be stable—at least not for long. Economic uncertainty is a fact of life, says Foster. Advocates of the gold standard want to “legislate certainty,” he says. “It’s like you have a town of declining morals, so you legislate churches. It’s not going to work.”

Well, I’m not sure that’s a very good analogy. It’s not like the government is imposing a gold standard on hooligan gang members who try to issue their own currency. No, the Federal Reserve does that, right now–i.e. the very thing that Foster says doesn’t work.

What the gold standard does, is impose a restraint on the government. So rather than “legislating morality,” it’s more like guaranteeing free speech, or the right to a jury trial.

A final point: Does anybody know if Foster has publicly endorsed complete drug legalization? I hope so. [UPDATE: I’m saying, in terms of logical consistency, if Foster says it wouldn’t work to force the government to not print a bunch of money, then surely he doesn’t think we can force people to not use cocaine.] It’s odd, because the gold standard is very old-school and conservative. On that score, one could have expected the economist from the Heritage Foundation to be all for it.

I Am a Tool of the Government

The Chinese government, I should clarify. A new Chinese rating agency had this to say about US government debt:

Dagong has downgraded the local and foreign currency long term sovereign credit rating of the United States of America (hereinafter referred to as “United States” ) from “AA” to “A+“, which reflects its deteriorating debt repayment capability and drastic decline of the government’s intention of debt repayment.

The serious defects in the United States economic development and management model will lead to the long-term recession of its national economy, fundamentally lowering the national solvency. The new round of quantitative easing monetary policy adopted by the Federal Reserve has brought about an obvious trend of depreciation of the U.S. dollar, and the continuation and deepening of credit crisis in the U.S. Such a move entirely encroaches on the interests of the creditors, indicating the decline of the U.S. government’s intention of debt repayment. Analysis shows that the crisis confronting the U.S. cannot be ultimately resolved through currency depreciation. On the contrary, it is likely that an overall crisis might be triggered by the U.S. government’s policy to continuously depreciate the U.S. dollar against the will of creditors.

I wholeheartedly agree with everything in the above analysis. Alas, here is what Paul Krugman has to say about their assessment: “Way to build credibility, guys — just in case anyone wondered whether Dagong would be truly independent, or just a tool for Chinese policy ….”

It’s funny how so many people around the world are tools of their governments. Only a fool could possibly disagree with quantitative easing.

Potpourri

My Firefox browser is littered with tabs, so it’s time to clean house…

* For those in the area, note that I will be back in Oregon later this week, in a multi-pronged educational effort with Richard Ebeling. Details here.

* In preparation for my debate with Krugman, I have been accumulating mainstream critiques of his worldview, the better to smell him with. Tyler Cowen and Scott Sumner have some good thoughts. I have also switched out of pizza and into low-fat cottage cheese. Mmmmm, cottage cheese.

* The econ profs at Hillsdale College have started a blog.

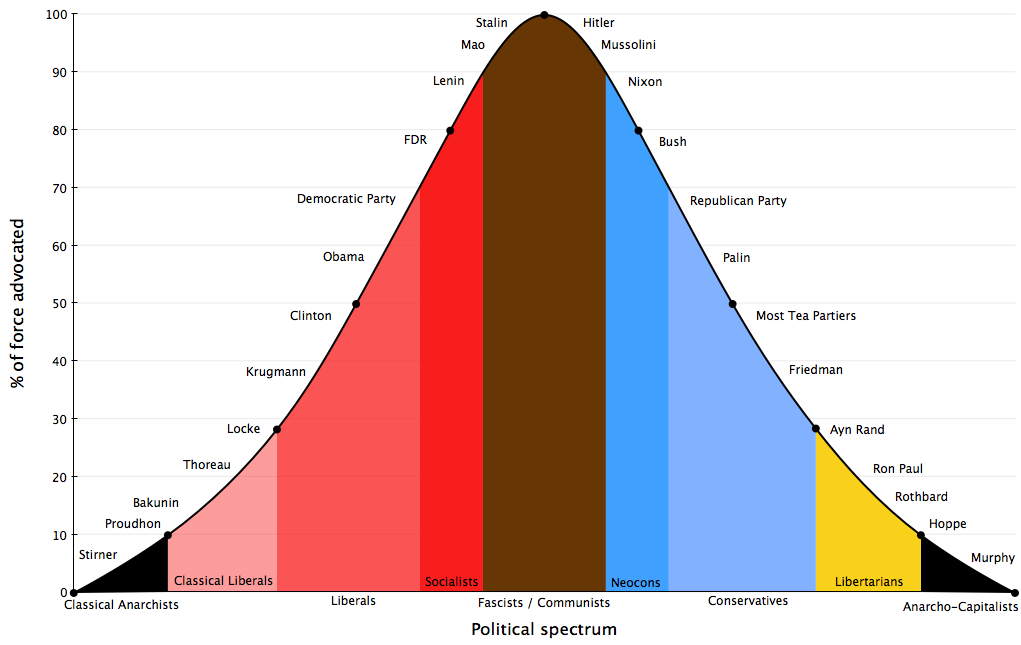

* I am to the right, not only of Hitler, but Hoppe. Who knew? (If you want the context of that graph, here.)

* Once you go Neo-Confederate, you never hear the end of it.

* David R. Henderson is doing some great work on austerity and the U.S. experience in World War II. I will definitely have to bone up on this material before the Krugman standoff. This is truly very important, because World War II is the one example that Krugman and the other Keynesians have pointed to, as an example of an economy allegedly taking off because of massive deficits. (They have also pointed to cases in the 1930s, but c’mon, is the U.S. in the years 1934-1936 really a “success story”?)

* Bryan Caplan has found a good discussion of paternalism and slippery slopes. He’s totally right. I am old enough to remember–back when they were banning cigarettes in restaurants–that right-wingers would say, “What next? Banning fatty foods? A Twinkie tax?” And I clearly remember that the response was, “Stop being absurd! Cigarettes can kill you. Get real, nobody is talking about banning Big Macs.”

* In this post, Krugman uses his FRED jujitsu to explain away surging commodity prices. He concludes, “There’s really nothing here to shake my view that deflation, not inflation, is the threat.”

Well two can play that game. Check out this FRED graph, showing year-over-year changes in the PPI versus the CPI. Look at how closely they follow each other over the decades. And now that the PPI is surging up, Krugman thinks the CPI is going to fall?

* Speaking of price inflation, Robert Wenzel explains that your toilet paper is shrinking. Wenzel–who for some reason likes to post pictures of pretty girls whenever possible on his blog–missed an obvious chance to link to a photo of Sheryl Crow.

Forgive Him, Mises, For Gonzo Knows Not What He Writes

A lot of people are flipping out over Gonzalo Lira’s latest tirade. His object this time is not the banksters, the government, or Paul Krugman. No, his target is the Austrian School of economics, and specifically its predilection for mathematical prediction, GDP maximization, and tax increases. (Yes.)

When I was reading Lira’s piece, at first I was annoyed. After all, I’m an Austro-libertarian; we are genetically predisposed to take offense at 95% of anything on the internet.

But after some of the following passages, it was apparent that Lira truly had no idea what he was even talking about. It would be like someone accusing Billy Graham of popery.

Anyway here’s Lira, lashing out against the Austrian School:

Well, economics claims it is a science—yet for all its “scientific” models, economics found itself in 2007 with its hands up against the wall and its collective pants down around its ankles, when it utterly failed to predict the Global Financial Crisis, and the subsequent Global Depression.

Actually, there were a number of non-economists whose predictions were far more accurate than any paid economists’. But all those eccy Ph.D.’s with all the academic trimmings? They got the big ol’ raspberry, when the Global Financial Crisis hit.

…

Why be coy: Economics isn’t a science—it never has been. It can’t be—because its subject matter is people: And people aren’t predictable.

…

Yet economics—ridiculously—claims it has models which can predict the future—but what’s even more ridiculous, there are many who believe them.

…

What did economists and the other clergy of economics claim, in the Fall of 2008? “If we don’t save the banks, we are all doomed!!!”That was of course not true: If the banks had not been bailed out, they would have gone into bankruptcy, the stock holders would have been wiped out, the bond holders would have gotten a haircut (or a buzzcut, rather)—but life would have gone on.

…

But not one economist in any position of influence advocated the bankruptcy and restructuring of the Too Big To Fail banks. Some actually advocated a “hold your nose and get it over with” approach to the TBTF banks—

…

Austrians argue that the government should cut spending and raise taxes, so as to balance the budget—and magically, the economy will improve, with no loss of GDP.Austrians are smoking something—and whatever it is, it’s powerful. So I want some.

Lira then says: “See, I’m not an Austrian. Not only that, I do not commune at the church of economics. Call me a son-of-a-bitch if you must, but don’t ever call me an economist.”

OK, Mr. Lira, it’s a deal.

P.S. If newcomers to this blog don’t understand why the above quotes are so funny, try reading this and this. Also, check out Robert Wenzel and Robert Blumen’s reactions to Lira.

Thinking Clearly About Capital, Interest, and Income

A few weeks ago I promised to “eviscerate” Scott Sumner’s blog post, in which he claimed that income was a “meaningless, misleading and pernicious” concept. It is now ready for your inspection. Flowers and condolences can be sent to Scott Sumner’s widow, c/o Bentley University.

Joking aside, this is actually related to my dissertation. Was it worth five years of my life, to be able to now dismantle Sumner? I believe so.

The intro:

Nowadays, Austrian economists are most famous for their theory of the business cycle, as developed by Ludwig von Mises and Friedrich Hayek. However, they also made many contributions to the pure theory of capital and interest, most notably in the seminal work of Eugen von Böhm-Bawerk and later in that of Hayek. In the present article we’ll see that these insights are relevant today, as mainstream economist Scott Sumner lashes out justifiably against absurd tax policies but, in the process, throws economic theory out the window too.

{kind=link}

{kind=link}

Recent Comments